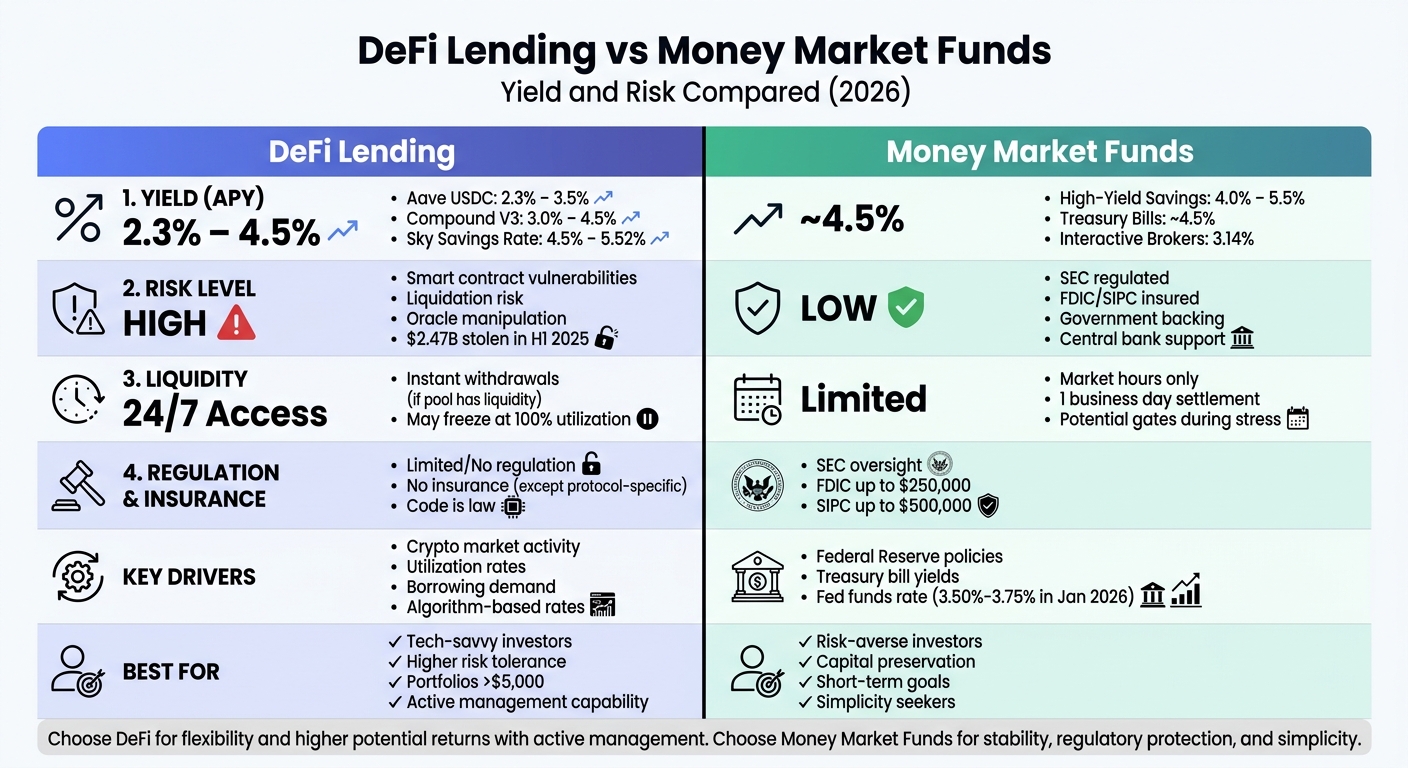

DeFi lending and money market funds offer distinct ways to earn yields, but their risks and returns vary significantly. Here’s what you need to know:

- DeFi Lending: Platforms like Aave and Compound provide yields by lending crypto assets through smart contracts. These yields are dynamic, often tied to market activity, but come with risks like smart contract vulnerabilities, liquidation risks, and potential hacks. Current yields (as of April 2026) range from 2.3% to 4.5% APY for stablecoins, often aligning with or falling below risk-free rates.

- Money Market Funds: These funds invest in short-term debt like U.S. Treasury bills and are regulated by the SEC. They offer predictable returns (around 4.5% APY in March 2026) and are less risky, with protections like SIPC or FDIC insurance. However, yields drop quickly when the Federal Reserve reduces interest rates.

Key takeaway: DeFi lending offers flexibility and higher potential returns but requires active management and tolerance for technical risks. Money market funds provide stability and regulatory safeguards but may lack the higher yields that some DeFi platforms can offer.

Quick Comparison

| Feature | DeFi Lending | Money Market Funds |

|---|---|---|

| Yield (APY) | 2.3%–4.5% | ~4.5% |

| Risk | High (smart contracts, hacks) | Low (regulated, insured) |

| Liquidity | 24/7 access | Limited to market hours |

| Regulation | Limited | SEC oversight |

| Insurance | None | FDIC/SIPC (up to limits) |

| Key Drivers | Crypto market activity | Federal Reserve policies |

DeFi lending suits tech-savvy investors seeking higher returns and willing to manage risks. Money market funds are better for those prioritizing safety and simplicity. Choose based on your risk tolerance and financial goals.

DeFi Lending vs Money Market Funds: Yield, Risk, and Features Comparison

How DeFi Lending Works

Core Features of DeFi Lending Platforms

DeFi lending platforms rely on smart contracts to manage loans, collateral, and liquidations automatically. To protect lenders, these platforms enforce over-collateralization, meaning borrowers must deposit assets worth more than the amount they borrow. This structure is key to balancing both yield potential and risk management.

Interest rates on these platforms are determined algorithmically. They adjust based on the utilization ratio – the percentage of the lending pool currently being borrowed.

"The protocol adjusts borrowing and lending rates automatically based on capital utilization – an approach driven solely by code." – Michael Hemingway, Blockchain Analyst

When you lend assets on platforms like Compound, you receive tokens such as cTokens (e.g., cUSDC), which reflect your share of the lending pool and automatically accrue interest. Aave, on the other hand, increases your balance over time. Both platforms offer instant withdrawals, provided there’s enough liquidity in the pool.

These automated systems form the backbone of DeFi lending, driving the performance seen in major platforms like Aave and Compound.

Case Studies: Aave and Compound

Looking at Aave and Compound highlights how their distinct approaches influence their performance.

As of February 2025, Aave managed around $41.1 billion in total value locked (TVL), dwarfing Compound’s $3.6 billion TVL. Aave operates across more than 14 blockchains, while Compound remains focused on Ethereum and major EVM-compatible chains like Polygon and Arbitrum.

Aave’s standout features include modular contracts and flash loans – uncollateralized loans that must be repaid within the same transaction block. In contrast, Compound uses a simpler structure centered around its Comptroller and cToken models.

Both platforms use a kinked interest rate model. Interest rates rise steadily as utilization increases but spike sharply once a target utilization point is reached, typically 80% for stablecoins. This discourages full utilization, ensuring lenders can still withdraw funds. Aave sets its optimal utilization at 80% for stablecoins and 95% for assets like ETH, with borrowing rates potentially jumping from single-digit percentages to over 50% APR when these thresholds are exceeded.

Collateral management is automated using a health factor, calculated as:

(Collateral Value × Liquidation Threshold) ÷ Total Debt.

If the health factor falls below 1.0, liquidators can step in to repay the debt and claim the collateral at a discount. To maintain accuracy, platforms like Aave and Compound rely on price oracles such as Chainlink to provide real-time asset valuations.

sbb-itb-7e716c2

DeFi Lending Explained: Aave vs Compound for Beginners

How Money Market Funds Work

Money market funds operate differently from algorithm-driven DeFi lending platforms. They rely on pooled investor capital and follow strict regulatory guidelines.

These funds gather money from investors to buy short-term debt instruments. They aim to keep a stable $1.00 net asset value (NAV) while offering yields that outperform typical bank savings accounts. By the end of January 2026, money market funds in the U.S. managed over $7 trillion in assets.

The investment approach focuses on high-credit-quality assets. This cautious strategy helps reduce interest rate risks and ensures yields adjust quickly when the Federal Reserve changes its policies. It’s important to note that, unlike bank deposits, money market funds are not covered by the FDIC. However, they are subject to strict liquidity rules set by the SEC.

After facing liquidity challenges in 2008 and 2020, the SEC implemented significant reforms in July 2023. These changes introduced stricter liquidity requirements, removed redemption "gates" that could block withdrawals, and added mandatory liquidity fees for certain funds during periods of high redemptions. These measures aim to prevent scenarios where investors rush to withdraw their money all at once.

"With these reforms in place, Paul Olmsted, a Morningstar principal for fixed-income strategies, considers most money market funds a relatively safe bet." – Paul Olmsted, Principal for Fixed-Income Strategies, Morningstar

Thanks to their short-term assets, money market funds can quickly adjust yields in response to Federal Reserve rate changes. For example, in March 2026, the average yield for these funds was around 4.5%, a significant increase from the historic low of 0.01% in 2013-2014.

Government vs. Prime Money Market Funds

There are two main types of money market funds, each with a unique balance of safety and returns.

Government money market funds invest at least 99.5% of their assets in cash, U.S. Treasury securities, and repurchase agreements backed by government securities. As of April 29, 2026, these funds accounted for $6.26 trillion in assets, dominating the market. They are considered the safest option because they’re backed by the U.S. government’s credit.

Prime money market funds, on the other hand, have a broader investment scope, including corporate commercial paper, certificates of deposit, and floating-rate debt from private corporations and financial institutions. By April 2026, these funds held $1.22 trillion in assets. Prime funds typically offer higher yields to offset the additional credit risk. For instance, in April 2026, the Schwab Prime Advantage Money Fund yielded 3.49%, slightly higher than the 3.38% yield of the Schwab Government Money Fund, showing an 11-basis-point difference.

The regulatory framework for these funds also varies. Institutional prime funds use a floating NAV, meaning their share price can fluctuate above or below $1.00. In contrast, retail and government funds maintain a stable $1.00 NAV. During times of extreme market stress, prime funds may impose liquidity fees or temporarily halt redemptions, though many government funds, like Vanguard‘s, opt not to use these measures.

These differences in structure and regulation cause the two fund types to respond differently to shifts in the market, particularly when influenced by Federal Reserve policies.

Federal Reserve Impact on Money Market Funds

Unlike DeFi platforms, which rely on algorithms, money market funds are directly influenced by Federal Reserve decisions. When the Fed adjusts the federal funds rate, the yields on the short-term debt held by these funds respond almost immediately.

This close connection is due to SEC rules that limit the weighted average maturity (WAM) of fund portfolios to 60 days or less. This ensures liquidity and forces funds to reinvest maturing securities at current market rates, making their yields highly sensitive to Fed policy.

The historical trends underline this relationship. For example, in 1981, money market fund yields soared to 13.4% as the Fed aggressively raised rates to curb inflation. Conversely, yields dropped to just 0.01% during the 2013-2014 zero-interest-rate period following the financial crisis. More recently, the Fed’s rate hikes brought yields back to the 4.5% range by March 2026.

This rapid adjustment makes money market funds appealing during rising-rate periods, as investors can benefit from higher yields without committing to long-term fixed rates. However, when the Fed cuts rates, these yields drop just as quickly, which may prompt investors to explore other options. These dynamics set money market funds apart from DeFi lending platforms, directly affecting their yield and risk profiles.

Yield Comparison: DeFi Lending vs. Money Market Funds

This section dives into how yields from DeFi lending platforms stack up against those from money market funds, highlighting key differences that investors should consider. By 2026, the yield landscape has shifted dramatically. For the first time in DeFi’s history, traditional savings and money market rates have outpaced major DeFi lending platforms. This is a far cry from the double-digit returns DeFi platforms boasted in 2021–2022, when Aave’s lending rates peaked at an impressive 20%. This shift underscores changing patterns in borrowing behavior and asset demand.

What Influences DeFi Lending Yields

DeFi lending yields are closely tied to utilization rates. When borrowing activity increases, protocols raise interest rates to maintain liquidity. This creates a direct connection between crypto market sentiment and DeFi yields. For example, during bull markets, borrowing surges as traders leverage their positions, pushing up utilization and yields. A clear illustration of this was the CoinDesk Overnight Rate (CDOR), which soared above 35% during 2023–2024 before dropping to around 3.5% by April 2026.

As of early 2026, the cooling demand for borrowing is reflected in current rates. Aave’s USDC supply rate is at 2.61%, while Compound V3 offers yields in the 3.0% to 4.5% range. These rates fluctuate in real time, driven by borrowing activity, unlike the steadier rates seen in traditional funds. The transition from "circular" yields – propped up by temporary token incentives – to "structural" yields based on actual borrower demand has compressed returns significantly. Some DeFi protocols are adapting by incorporating Real-World Assets (RWAs) like U.S. Treasuries. For instance, the Sky Savings Rate has attracted $6.5 billion in deposits, offering yields between 3.75% and 4.5%, primarily funded through off-chain Treasury products.

"Undifferentiated lending converges toward risk-free rates because when every depositor shares the same collateral, the same parameters, and the same outcome, there is limited room for specialization and returns compress." – Paul Frambot, Co-founder, Morpho

In contrast, money market fund yields are shaped by broader economic policies rather than crypto-specific factors.

What Influences Money Market Fund Yields

Money market fund yields operate on an entirely different mechanism. They are driven by macroeconomic factors, especially the Federal Reserve’s target interest rates and U.S. Treasury bill yields. When the Fed adjusts the federal funds rate, money market funds respond almost immediately. This is because SEC regulations limit their weighted average maturity to 60 days or less, forcing continuous reinvestment at current market rates. As a result, these yields are highly sensitive to Federal Reserve policy.

By January 2026, the federal funds rate stood at 3.50% to 3.75%. Money market funds closely tracked this, with average yields reaching 4.5% by March 2026. High-yield savings accounts (HYSAs) provided even more competitive returns, ranging from 4.0% to 5.5% APY, with some hitting 5.00% in February 2026. Unlike DeFi’s algorithm-driven, volatile rates, money market fund yields are relatively stable and predictable, as they are determined by institutional issuers and Fed policy rather than fluctuating market dynamics. While this stability is appealing, it comes with a downside: yields decline quickly when the Fed lowers rates. However, these funds benefit from government backing or FDIC insurance up to $250,000, adding a layer of security.

Yield Comparison Table

| Asset/Platform | Type | Feb/March 2026 Yield (APY) | Key Driver |

|---|---|---|---|

| Varo Money (HYSA) | TradFi | 5.00% | Fed policy and bank competition |

| U.S. Treasury Bills | TradFi | ~4.5% | Fed funds rate |

| Sky Savings Rate (sUSDS) | DeFi (RWA) | 4.5% – 5.52% | U.S. Treasuries and protocol |

| Compound V3 USDC | DeFi | 3.0% – 3.83% | Utilization and borrowing demand |

| Aave V3 USDC (Ethereum) | DeFi | 2.3% – 3.5% | Pool utilization |

| Interactive Brokers Cash | TradFi | 3.14% | Fed policy |

The comparison paints a clear picture: traditional financial options now rival or surpass most DeFi lending rates. Even when DeFi platforms advertise competitive rates, investors must weigh additional considerations like smart contract risks, gas fees, and tax implications. To account for these risks, professional analysts often apply a "Smart Contract Risk Discount" of 1% to 3% to gross DeFi APYs.

"DeFi: earn 1% below T-bills and lose all your money one time per year." – James Christoph, Trader

This blunt observation underscores the risks involved. In just the first half of 2025, hackers stole over $2.47 billion in cryptocurrency. When these risks are considered, the net returns from DeFi often fall short of FDIC-insured alternatives that provide similar or better yields without the technical vulnerabilities.

Risk Comparison: DeFi Lending vs. Money Market Funds

When weighing investment options, understanding the risks is just as important as analyzing the returns. DeFi lending and money market funds come with distinct risk profiles, shaped by their underlying frameworks and vulnerabilities. Knowing these risks can help you make smarter decisions about where to allocate your capital.

DeFi Lending Risks

DeFi lending operates on decentralized platforms, which introduces a range of technical and operational risks.

Smart contract vulnerabilities are a major concern. Even rigorously audited code can have flaws, and upgradeable contracts can be exploited through compromised admin keys. For instance, in April 2026, the Drift Protocol on Solana faced a $270 million exploit due to an issue with Solana’s durable nonce feature. Around the same time, the Kelp DAO exploit drained $292 million, severely impacting Aave’s USDC pool, which hit 99.87% utilization and temporarily froze withdrawals.

Past incidents highlight these risks. In March 2023, Euler Finance lost $197 million when an attacker used a flash loan to exploit a vulnerability in its donation mechanism. Although the funds were eventually recovered, depositors were locked out of their capital for three weeks. Similarly, in April 2022, Beanstalk Farms suffered a $182 million loss when a flash loan allowed an attacker to gain a voting majority and transfer the protocol’s treasury to their own wallet.

Liquidation risk is another challenge. If collateral values drop below required thresholds, automated liquidations can trigger, often at discounted rates. This can create a domino effect, driving prices down and causing further liquidations.

"If you cannot identify exactly which risks you are taking on for a given yield, you are probably the exit liquidity." – Jorge Rodriguez, Risk Management, Lince Yields

Oracle risk also poses a threat. DeFi protocols rely on external price feeds, and inaccurate or manipulated data can lead to errors. Additionally, when pool utilization exceeds 90-95%, lenders may face withdrawal restrictions until borrowers repay or new liquidity enters.

Money Market Fund Risks

Money market funds operate in a regulated environment, which reduces many of the risks seen in DeFi lending. However, they come with their own set of vulnerabilities.

Credit exposure and liquidity crunches are key risks. During the March 2020 market turmoil, investors pulled $139 billion from prime money market funds in just a few weeks – about 17% of fund assets. This forced the Federal Reserve to step in with emergency facilities to stabilize the market.

Interest rate sensitivity directly impacts returns. When the Federal Reserve cuts rates, money market fund yields drop quickly due to SEC rules requiring short maturities (60 days or less). This forces continuous reinvestment at lower rates during rate-cutting cycles, leading to yield compression.

Redemption mechanics can also become problematic during periods of stress. While redemptions are typically offered at Net Asset Value (NAV), funds may impose liquidity fees or temporary withdrawal restrictions ("gates") to manage outflows. Despite these challenges, money market funds benefit from regulatory oversight, central bank backstops, and protections like SIPC insurance for brokerage cash sweeps – advantages that DeFi platforms lack.

The key distinction lies in intervention capacity. Traditional finance relies on mechanisms like Federal Reserve support and institutional insurance to manage risks. In contrast, DeFi operates under a "code is law" principle, with limited safety nets beyond protocol-specific insurance options like Aave’s staked AAVE Safety Module.

Risk Comparison Table

| Risk Type | DeFi Lending | Money Market Funds | Mitigation Options |

|---|---|---|---|

| Smart Contract/Code | High: $270M Drift exploit (April 2026) | None | Diversify protocols; verify audits; prefer battle-tested platforms |

| Liquidation/Forced Sales | High: Cascading liquidations during volatility | Low: Regulated diversification limits | Maintain health factors >1.5; use automation tools |

| Liquidity/Withdrawal | Medium-High: Blocked at 100% utilization | Medium: Gates/fees during stress | Monitor utilization rates <90% |

| Credit/Counterparty | Medium: For DeFi, this risk arises from protocol solvency | Low-Medium: Regulated funds face issuer default risk | Choose protocols with proven track records |

| Regulatory | High: Evolving frameworks and uncertain compliance | Low: Established SEC oversight | Stay informed on regulatory developments |

| Systemic/Contagion | High: Interconnected protocols amplify failures | Low: Central bank backstops available | Diversify across chains and ecosystems |

| Oracle/Price Feed | Medium-High: Manipulation or stale data | None | Protocol-dependent; limited user control |

| Governance | Medium: Flash loan attacks on voting | None | Monitor time-locks and proposal activity |

Managing Risks

Experienced DeFi users employ proactive strategies to navigate these risks. They maintain conservative health factors of 1.5 or higher, setting alerts at 1.3–1.5 to act before liquidation. Diversification is another key tactic, spreading investments across established protocols like Aave and Compound and across multiple blockchains (e.g., Ethereum, Solana, Layer 2s) to reduce single points of failure. Automation tools, such as DeFi Saver, can also help by automatically selling collateral or repaying debt if health factors fall below target levels.

For money market fund investors, regulatory safeguards handle many risks through diversification requirements, maturity limits, and access to Federal Reserve facilities during stress periods. The trade-off is clear: DeFi offers higher potential returns and 24/7 access but demands active risk management and tolerance for technical risks. On the other hand, money market funds provide stability and regulatory protection but come with lower yields and limited flexibility.

Investor Profiles and Preferences

Deciding between DeFi lending and money market funds often boils down to your personality as an investor – how much risk you’re comfortable with, the size of your portfolio, and what financial decisions might keep you awake at night.

Who Chooses DeFi Lending?

Crypto-native investors are naturally drawn to DeFi lending for its yields and structural perks like 24/7 liquidity and composability. These investors appreciate the flexibility to stack yields and access their funds anytime. By Q1 2026, DeFi lending made up 43% of all DeFi Total Value Locked (TVL), with Aave leading the pack, holding a 60% market share and over $25 billion in TVL.

High-yield seekers, willing to take on the risks tied to smart contracts, often move their capital to isolated markets like Morpho Blue or restaking protocols. They aim for returns in the range of 5–15% APY. However, they are well aware that these higher returns come with risks, including exploits and concentration risk. For instance, in just the first half of 2025, hackers stole over $2.47 billion in cryptocurrency.

Institutional allocators are stepping into the DeFi space through tailored lending arrangements. Firms like Apollo are leveraging customized risk-return models that go beyond traditional pooled structures. Similarly, transparency advocates – those who distrust centralized intermediaries – are drawn to DeFi’s non-custodial nature and its "code-is-law" ethos. DeFi also eliminates the creditor status tied to traditional bank deposits.

That said, DeFi lending isn’t for everyone. Gas fees can eat into returns, especially for smaller portfolios. If your portfolio is under $5,000, on-chain DeFi lending may not yield competitive returns. These factors highlight how different investors balance risk and reward when choosing technology-driven financial solutions.

Who Chooses Money Market Funds?

On the flip side, risk-averse individuals often lean toward money market funds, especially when saving for short-term goals like a home down payment or a tax bill. As of April 2026, U.S. high-yield savings accounts offered returns of 4.0–4.5%, while Interactive Brokers provided a 3.14% yield on idle USD cash for accounts exceeding $100,000. These options deliver stability and predictability, avoiding the volatility tied to DeFi platforms.

Small portfolio holders also prefer traditional accounts, as fees and gas costs can erode returns in DeFi. Analysts often apply a "Smart Contract Risk Discount" of 1% to 3% to DeFi yields. This means a 12% APY in DeFi could realistically net just 4.2%, barely competing with a Treasury bill.

"If you are only earning an extra 1% for the headache of managing private keys, monitoring pool ratios, and worrying about protocol hacks, you aren’t being compensated enough for the risk." – Calcix Research Team

Tax-conscious investors also gravitate toward money market funds. These funds simplify annual tax reporting, avoiding the frequent taxable events tied to DeFi rebalancing and reward claims. Every reward claim in DeFi triggers a taxable event, adding complexity to accounting. Additionally, institutional investors focused on regulatory compliance and seeking SIPC protection (up to $500,000 for brokerage accounts) often stick with traditional options.

The psychological aspect is worth noting too. Money market funds attract those who want to avoid the stress of managing private keys or dealing with price volatility. High-profile exploits, like the $270 million Drift Protocol drain in early 2026, have driven many investors toward FDIC-insured or sovereign-backed assets.

Ultimately, the decision comes down to balancing the allure of higher yields with the risks of smart contracts versus the stability and regulatory protections of traditional financial products.

Making Your Decision: Yield vs. Risk

The choice between yield and risk boils down to how much extra return you need to justify the added complexity and uncertainty. As the Calcix Research Team aptly states:

"A true professional doesn’t just look for the highest number; they look for the most ‘efficient’ number – the highest return per unit of stress and risk."

Let’s break down when each approach – DeFi lending or money market funds – makes the most sense.

When to Choose DeFi Lending

DeFi lending is a good fit when you can secure a meaningful liquidity premium, typically 3–5% above the current 10-year Treasury yield. For example, in Q1 2026, stablecoin APYs ranged from 3.0% to 7.2% depending on the platform. However, don’t overlook hidden costs. A 12% gross yield in DeFi can drop to just 4.2% after factoring in risks like smart contract vulnerabilities, gas fees, and taxes.

Before diving in, apply the 10x Gas Rule: only proceed if your first-month earnings are at least ten times your total entry and exit gas fees. For portfolios under $5,000, high gas fees can quickly eat into returns. If you’re comfortable managing private keys, monitoring health factors, and handling tax complexities, DeFi could deliver net after-tax APYs of 4–7% in 2026. But remember, this is only suitable if you’re prepared to face risks like smart contract failures, unreliable price oracles, and potential liquidations.

When to Choose Money Market Funds

Money market funds are ideal for capital preservation and short-term financial goals. Whether saving for a house down payment or a tax bill, these funds offer FDIC insurance (up to $250,000) and predictable returns, making them safer and more stable than DeFi. For instance, in April 2026, high-yield savings accounts provided APYs between 4.0% and 4.5%, while Interactive Brokers offered 3.14% APY on idle cash for accounts over $100,000.

The tax process is also simpler – earnings are reported as ordinary income on a 1099-INT. For smaller portfolios or risk-averse individuals, the added benefits of SIPC protection (up to $500,000 for brokerage accounts) and one-business-day liquidity eliminate the complexities of managing private keys or worrying about protocol vulnerabilities.

Next Steps

To strike a balance between yield and risk, consider these actionable steps. A hybrid strategy often works well: keep 3–6 months of living expenses in a traditional high-yield savings account (HYSA) for liquidity and safety. Then, allocate 20–40% of your portfolio to reputable DeFi lending platforms for higher returns, while limiting high-risk DeFi exposure to 5–10%.

Diversify across platforms like Aave, Compound, and Morpho to minimize the risk of a single-point failure. If borrowing, set health factor alerts between 1.3 and 1.5, and act quickly if triggered – a 15% drop in collateral value could lead to liquidation. For tailored strategies that match your financial goals and risk tolerance, consult resources like BeyondOTC for personalized guidance.

FAQs

What’s the safest way to try DeFi lending?

When diving into DeFi lending, it’s wise to stick with trusted platforms like Aave V3. This protocol stands out for its strong liquidation system, dependable oracle feeds, and support across multiple networks like Ethereum, Arbitrum, and Base. To get started, consider making a small deposit using stablecoins. Keep an eye on your health factor and steer clear of high-risk pools offering tempting yields or those overly reliant on a single protocol. This approach helps reduce the risks tied to smart contracts and potential liquidity problems.

How do I estimate my real DeFi yield after fees and taxes?

To figure out your actual DeFi yield, begin with the gross yield advertised by the platform – this usually ranges from 1.8% to over 10% APY. Then, subtract any platform fees, gas fees, and adjustments for potential risks, such as smart contract vulnerabilities. Lastly, factor in taxes. In the U.S., these are typically calculated based on either income or capital gains. By considering all these elements, you can determine your net yield after fees and taxes.

When do money market fund yields fall?

Money market fund yields usually drop when interest rates in the economy go down, often triggered by actions like the Federal Reserve cutting rates or keeping the federal funds rate unchanged. Other factors, such as lower investor demand or heightened competition from safer alternatives like high-yield savings accounts or Treasury bills, can also contribute to this decline. These shifts typically reflect broader economic trends that push rates lower throughout financial markets.