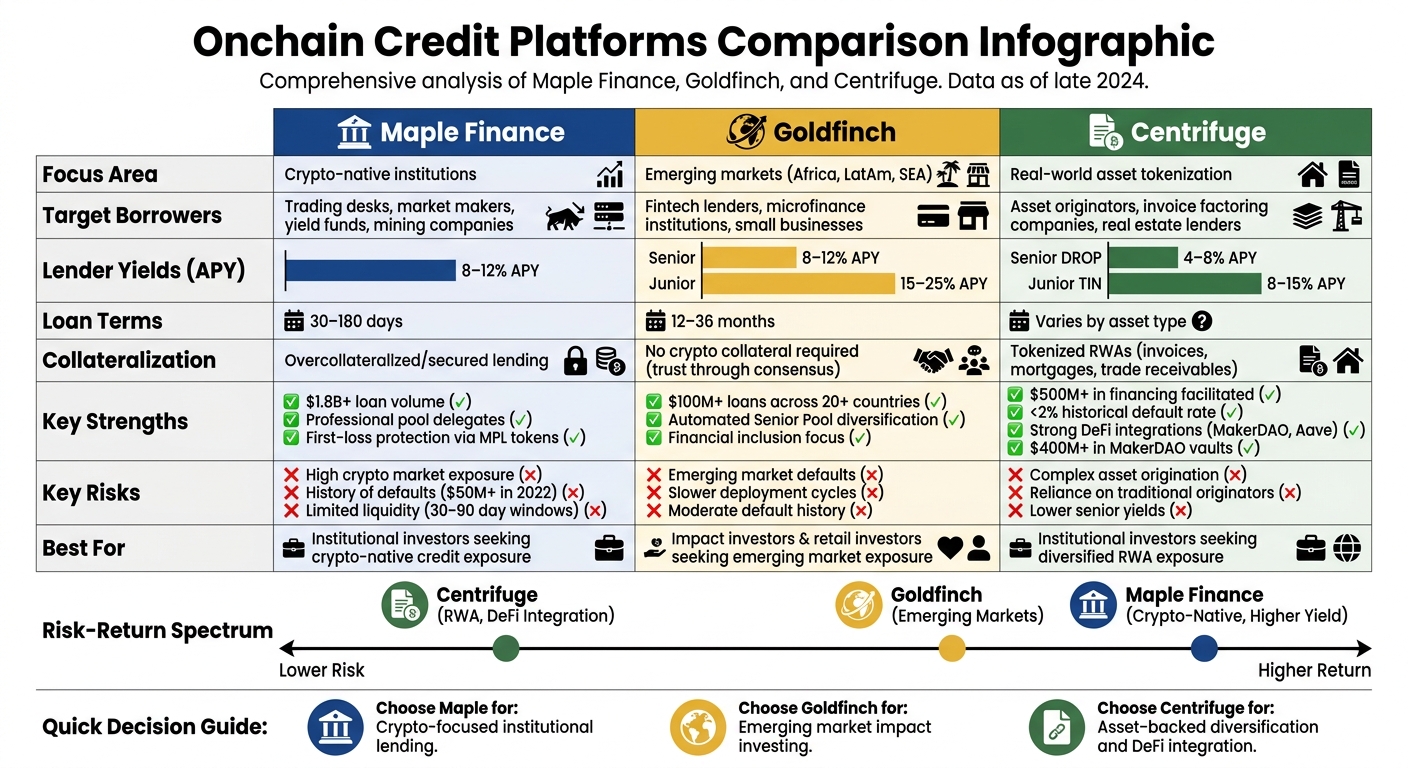

Onchain credit platforms are transforming lending by connecting borrowers and lenders directly through blockchain, cutting out intermediaries and reducing costs. These platforms focus on tokenizing assets like invoices and real estate, offering decentralized financing options with yields typically ranging from 8% to 20% APY. Maple Finance, Goldfinch, and Centrifuge are leading the way, each with unique approaches:

- Maple Finance: Targets crypto-native institutions with short-term loans (30–180 days) and offers 8–12% APY for lenders. It uses expert delegates for oversight and emphasizes secured lending after past losses.

- Goldfinch: Focuses on emerging market fintechs and small businesses, offering loans without requiring crypto collateral. Lenders earn 8–12% APY (senior pool) or 15–25% APY (junior pool), but risks include defaults in high-risk regions.

- Centrifuge: Tokenizes assets like invoices and trade receivables, catering to asset originators. It offers 4–8% APY for senior tranche investors and 8–15% APY for junior tranche investors, with low default rates and strong DeFi integrations.

Each platform offers distinct benefits and trade-offs based on risk, returns, and borrower focus. Below is a quick comparison:

| Platform | Focus Area | Lender Yields | Borrower Type | Key Risks |

|---|---|---|---|---|

| Maple Finance | Crypto-native institutions | 8–12% APY | Trading desks, market makers | Crypto market exposure |

| Goldfinch | Emerging markets | 8–12% (senior), 15–25% (junior) | Fintechs, small businesses | Emerging market defaults |

| Centrifuge | Asset tokenization | 4–8% (senior), 8–15% (junior) | Asset originators | Complexity of origination |

Choose based on your investment goals: crypto-focused lending (Maple), emerging market impact (Goldfinch), or asset-backed diversification (Centrifuge).

Maple Finance vs Goldfinch vs Centrifuge: Platform Comparison

1. Maple Finance

Operational Model

Maple Finance operates using a Pool Delegate model, where experienced credit managers oversee lending pools, perform off-chain due diligence, and underwrite loans. To align their financial interests with lenders, these Pool Delegates commit their own MPL tokens as first-loss protection. This means their capital absorbs initial losses, creating a safety net before any impact reaches the liquidity providers.

In 2025, Maple facilitated over $11.27 billion in loans, significantly increasing its assets under management from $516 million to $4.59 billion – a jump of 767%. During the same period, the platform generated $49 million in interest for its lenders. Pool shares are issued as ERC-20 tokens, making them tradable on secondary markets like Uniswap. However, Maple’s composability with other DeFi protocols remains somewhat limited. This operational framework supports Maple’s strategy of catering to a broad range of borrowers.

Target Borrowers

Maple’s primary clients include crypto-native institutions such as market makers, trading desks, yield funds, and mining companies. It also serves neobanks, fintech firms, and traditional financial institutions looking for on-chain asset management options. By the end of 2025, the platform had 65 active borrowers, with 42 new clients joining that year alone.

To maintain trust in its decentralized lending environment, all borrowers go through KYC checks and credit evaluations conducted by Pool Delegates. Loan terms typically range from 30 to 180 days, with interest rates historically falling between 10% and 18%. Lenders, on the other hand, generally earn an APY of 8-12%.

Collateralization Approach

Maple has refined its approach to collateralization after experiencing early credit losses. Initially focused on uncollateralized or undercollateralized corporate credit, the platform faced over $50 million in losses from crypto-native firm defaults in 2022. In response, Maple shifted to a more conservative strategy, emphasizing overcollateralized and secured lending.

Its Institutional-Secured Lending product now offers depositors an APY of around 10.31%. Loans are backed by various forms of collateral, such as crypto assets, company revenue streams, or other assets. Unlike many DeFi platforms that rely on automated liquidation mechanisms, Maple takes a manual approach to managing stress events. Borrowers are given time – often hours – to address margin calls before any forced liquidations occur. This hands-on method helps mitigate risks while maintaining flexibility.

sbb-itb-7e716c2

2. Goldfinch

Operational Model

Goldfinch takes a different approach to crypto lending by replacing the need for collateral with a "trust through consensus" system. This system evaluates a borrower’s creditworthiness based on human judgment rather than automated collateral ratios. Unlike platforms like Maple Finance that rely heavily on crypto collateral, Goldfinch’s model aims to broaden access to credit by removing these traditional requirements.

"Removing the collateral requirement would be the crucial step that finally opens crypto lending to the majority of the world." – Mike Sall, CEO and Co-Founder, Goldfinch

The platform divides its capital into two distinct tranches. Backers provide first-loss capital and earn between 15%–25% APY, while Liquidity Providers contribute passive funds, earning 8%–12% APY. This setup ensures that Backers carefully evaluate borrowers since they bear the initial risk of any default.

To enhance security, Goldfinch uses a Unique Identity (UID) system, a non-transferable NFT representing on-chain KYC/KYB verification. In February 2021, Goldfinch deployed its first $1 million in loans through partnerships with companies like PayJoy in Mexico (for smartphone financing), QuickCheck in Nigeria (personal loans), and Aspire in Southeast Asia. These businesses converted USDC into fiat currency to fund thousands of local borrowers. By October 2025, the platform had facilitated over $230 million in loans across more than 20 countries.

Goldfinch also introduced Goldfinch Prime, an institutional-grade offering. This initiative tokenizes private credit funds managed by top-tier asset managers like Apollo and Ares, who collectively oversee over $1 trillion in assets. This allows investors to gain on-chain exposure to diversified credit portfolios while maintaining Goldfinch’s emphasis on emerging market lending.

Target Borrowers

Goldfinch primarily serves fintech lenders, microfinance institutions, and small business lending platforms operating in emerging markets like Africa, Latin America, and Southeast Asia. These borrowers typically require loans with terms ranging from 12 to 36 months to fund activities such as consumer lending, motorcycle loans in Kenya, and small business financing.

This focus sets Goldfinch apart from crypto-native platforms like Maple, which cater to trading desks with much shorter loan terms (30 to 180 days). Goldfinch, on the other hand, targets businesses with strong off-chain revenue streams but no on-chain assets. However, this approach is not without risk. For example, in April 2024, borrower Lend East defaulted on a $10.2 million loan, repaying only $4.25 million and resulting in a $5.9 million loss. This incident underscored the challenges of undercollateralized lending in emerging markets.

Collateralization Approach

Goldfinch allows borrowers to secure loans without relying on crypto collateral. Instead, loans are backed by off-chain assets and income, protected through legal contracts. Borrowers and Backers often establish off-chain agreements that enable legal recourse or asset seizure in case of default.

The platform also encourages repayment by maintaining a public on-chain credit history. Any late payment can prevent borrowers from accessing further credit across the protocol. To manage risk, the Junior Tranche absorbs losses first, creating a safety buffer for Senior Pool investors. The Senior Pool only allocates funds to a Borrower Pool once enough Backers have committed their own capital, ensuring that incentives remain aligned.

DeFi Integrations

Goldfinch’s innovative lending and collateral strategies have paved the way for partnerships with major players in the DeFi ecosystem. The platform collaborates with organizations like Circle, a16z, Coinbase Ventures, BlackRock, and Apollo to expand access to institutional-grade credit. Its senior pool token, FIDU, integrates with platforms like Curve to provide liquidity options for lenders. These partnerships not only enhance liquidity but also reinforce Goldfinch’s mission of supporting lending in emerging markets.

3. Centrifuge

Operational Model

Centrifuge acts as a platform for turning real-world assets into digital tokens. Companies that already manage loan portfolios can use the Centrifuge Chain – a blockchain with a secure and privacy-focused document layer – to tokenize their assets as NFTs. These tokenized assets, such as invoices, mortgages, and trade receivables, are then used as collateral in decentralized finance (DeFi) pools.

The protocol employs two types of tokens for its tranches: DROP tokens for the senior tranche, offering yields between 4–8% APY, and TIN tokens for the junior tranche, with higher returns of 8–15% APY but also absorbing the first losses. Unlike platforms like Maple or Goldfinch, which rely on pool delegates or community backers, Centrifuge depends on traditional asset originators to perform off-chain due diligence. This ensures that existing loan portfolios are carefully vetted before they are tokenized.

By February 2026, Centrifuge had facilitated over $500 million in financing, maintaining a historical default rate of under 2%. The protocol also boasts over $250 million in active Total Value Locked (TVL) and supports more than $100 million of DAI within MakerDAO vaults. These yield ranges demonstrate how Centrifuge balances risk and return, making it a key player in the onchain credit space.

Target Borrowers

Centrifuge primarily caters to asset originators in traditional financial sectors, such as invoice factoring companies, real estate lenders, trade finance providers, and revenue-based financing firms. These borrowers typically operate in the broader economy rather than within crypto markets. The platform allows them to set up credit facilities in just weeks – far quicker than the months-long process required by traditional banks. Additionally, it provides access to global crypto liquidity, bypassing the challenges of correspondent banking relationships.

Major institutional investors, including BlockTower, have leveraged Centrifuge to manage large-scale credit pools that combine real-world private credit with DeFi’s composability. This approach to collateralization helps investors better manage risks associated with their investments.

Collateralization Approach

Centrifuge tokenizes assets as ERC-20 or ERC-721 (NFT) tokens, offering a detailed breakdown of asset pools. To ensure transparent pricing, the platform uses an on-chain Net Asset Value (NAV) calculation based on a Discounted Cash Flow (DCF) model. Each collateral NFT is assigned to specific risk groups with ceiling ratios that cap borrowing limits and thresholds that trigger asset seizure.

The junior tranche (TIN) plays a critical role by acting as a capital buffer, shielding senior investors from defaults. If debt surpasses the threshold ratio, a "Collector" contract can seize collateral NFTs, linking onchain defaults to real-world asset recovery. Investors can assess risk by examining the size of the junior tranche – a larger TIN allocation typically means greater protection for DROP holders.

DeFi Integrations

Centrifuge is deeply integrated into major DeFi protocols, serving as vital infrastructure. In 2021, it partnered with MakerDAO to launch the first large-scale on-chain private credit facility. This allowed real-world assets, like trade receivables and real estate, to generate institutional-grade yields for DeFi participants. Centrifuge also collaborates with Aave, enabling these platforms to diversify their asset backing beyond crypto-native holdings.

This level of integration sets Centrifuge apart from competitors like Maple, which operates standalone pools, and Goldfinch, which has fewer DeFi connections.

Advantages and Disadvantages

Each platform brings its own set of strengths and challenges, offering different trade-offs when it comes to risk, yield, and liquidity. Let’s break down how these platforms operate and what sets them apart.

Maple Finance is a standout in institutional lending, having facilitated over $1.8 billion in loans. Its professional pool delegates actively manage credit risk and stake their own capital as a form of first-loss protection. This structure ensures a level of accountability. However, Maple’s reliance on crypto-native borrowers exposes it to high correlation with broader crypto market fluctuations. Past default events highlight this vulnerability. Another limitation is its liquidity, which is restricted to withdrawal windows of 30–90 days, reducing flexibility for investors.

Goldfinch takes a global approach, with over $100 million in loans across more than 20 countries. The platform’s Senior Pool simplifies diversification for passive investors, while junior tranches offer higher yields of 15–25% APY. Goldfinch’s "trust through consensus" model relies on decentralized auditors for off-chain due diligence, minimizing reliance on centralized gatekeepers. However, this decentralized process slows down deployment cycles. Additionally, its focus on emerging markets introduces default risks tied to those regions. On the other hand, Centrifuge employs tokenized real-world assets (RWAs) to connect traditional financing with DeFi.

Centrifuge has carved a niche by integrating with major DeFi protocols like MakerDAO and Aave, with over $400 million locked in MakerDAO DAI vaults. Its focus on RWAs results in low correlation with crypto market volatility and a historical default rate below 2%. However, the platform depends on traditional asset originators for due diligence, which can complicate scalability. Tokenizing custom real-world assets also introduces complexity compared to more standardized lending models.

Here’s a quick comparison of their strengths and weaknesses:

| Platform | Key Strengths | Key Weaknesses |

|---|---|---|

| Maple Finance | $1.8B+ loan volume; professional delegates; 8–12% APY yields | History of defaults; high crypto market exposure; limited liquidity |

| Goldfinch | Operates in 20+ countries; automated Senior Pool; 15–25% junior APY | Slower deployment cycles; emerging market risks; moderate default history |

| Centrifuge | Strong DeFi ties; <2% default rate; diverse RWA exposure | Complex asset origination; reliance on traditional originators; 4–8% senior APY |

Lastly, each platform’s regulatory approach adds another layer of differentiation. Maple enforces strict KYC requirements and adheres to established securities norms, catering to institutional players. Goldfinch uses enforceable smart contracts via SPVs, while Centrifuge employs legal SPVs to provide real-world recourse. These strategies reflect their priorities, from decentralization to compliance, offering varying levels of accessibility for different types of investors.

Conclusion

Match your investment goals to the strengths of each protocol.

Maple Finance appeals to those looking for exposure to crypto-native institutional credit. With professional delegates actively managing credit, the platform offers opportunities but also comes with risks like crypto market volatility and significant defaults – over $50 million in 2022 alone. Its 30–180 day loan terms are ideal for investors comfortable with shorter liquidity windows.

Goldfinch focuses on emerging markets and financial inclusion. Investors in its Senior Pool can enjoy passive diversification with returns of 8–12% APY, while junior tranches offer higher yields of 15–25% for those willing to accept first-loss risk and the complexities of emerging market credit.

Centrifuge opens the door to tokenized real-world assets, such as real estate and trade finance. Senior DROP tokens yield 4–8% APY, while junior TIN tokens offer 10–20% APY. Its integration with MakerDAO and Aave provides institutional-grade functionality, though the complexity of asset origination can pose scalability challenges.

Each of these platforms caters to specific investment profiles. For institutional investors, Maple and Centrifuge offer structured credit models, while retail investors may find Goldfinch’s passive Senior Pool more appealing. Crypto-native borrowers often turn to Maple, emerging market fintechs gravitate toward Goldfinch, and asset originators benefit from Centrifuge.

These platforms showcase DeFi’s evolution from synthetic yields to real-world cash flows. The right choice depends on your risk tolerance and liquidity preferences – whether you’re drawn to crypto-native opportunities, emerging market impact, or diversified real-world assets.

FAQs

How do I pick between Maple, Goldfinch, and Centrifuge?

When deciding where to invest, it’s important to weigh each platform’s focus, risk level, and target audience.

- Maple: This platform caters to institutional crypto lending, offering yields in the range of 8-12%. It’s a good option for those looking for a more structured, institutional approach.

- Goldfinch: With a focus on emerging markets and financial inclusion, Goldfinch provides higher yields of 15-25%, though this comes with a potentially higher risk profile.

- Centrifuge: Specializing in a variety of real-world assets, such as trade finance and real estate, Centrifuge offers yields from 4-20%, making it a diverse choice for investors interested in tangible asset backing.

Your decision should align with your comfort level regarding risk, the type of borrowers you prefer, and your overall investment objectives.

What’s the biggest risk for lenders on each platform?

The risks lenders face vary depending on the platform. On Goldfinch, the biggest challenge is ensuring that private credit agreements are enforceable, particularly when dealing with borrowers in emerging markets. This can increase the likelihood of defaults or lead to complex legal disputes. For Centrifuge, the main concerns revolve around borrower defaults and the regulatory gray areas surrounding tokenized real-world assets. These uncertainties could affect how these assets are treated within the on-chain environment.

How liquid are these investments if I need my money back?

Liquidity can differ significantly depending on the platform and the type of investment structure. For instance, Maple’s senior pools tend to provide greater liquidity, offering quicker access to funds. On the other hand, Goldfinch’s junior tranches are typically locked until the underlying loans reach maturity, which limits liquidity. Similarly, Centrifuge’s asset-backed pools, such as Tinlake, show variation in liquidity. Senior tranches in these pools generally allow easier access to funds compared to junior tranches. If quicker access to your investment is a priority, senior pools or tranches are usually the more suitable choice.