Pre-IPO gains – like stock options or RSUs – can result in significant tax liabilities depending on where you live. Here’s a quick breakdown of how the US, EU, and UAE handle these gains:

- US: Taxed on worldwide income. Gains are subject to federal rates (up to 37%), plus a 3.8% Net Investment Income Tax (NIIT) for high earners. Long-term capital gains (held over a year) are taxed at lower rates (0%, 15%, or 20%). Tools like Section 83(b) elections and QSBS exclusions can help reduce taxes.

- EU: Rules vary by country. Some, like Luxembourg, offer 0% tax after short holding periods, while others, like Germany, impose stricter regulations and exit taxes. The EU enforces fair value rules and anti-tax avoidance measures.

- UAE: No personal income or capital gains taxes. However, US citizens living in the UAE remain subject to US taxes. UAE corporations can avoid the 9% corporate tax through exemptions like the Participation Exemption.

Key Takeaway: Tax strategies depend heavily on your location, holding periods, and planning. For instance, exercising options early in low-tax years or relocating to tax-friendly jurisdictions can significantly lower your liabilities.

Your Pre-IPO Equity Needs a Game Plan. Here’s the Framework.

sbb-itb-7e716c2

US Tax Treatment of Pre-IPO Gains

In the United States, pre-IPO gains are taxed based on worldwide income. The rates depend on how long you’ve held the assets and the type of equity compensation you have. Federal tax rates can range from 20% to 37%, with additional state and surtaxes potentially applying.

Capital Gains Tax Rates and Net Investment Income Tax

The IRS taxes short-term capital gains – assets held for a year or less – at ordinary income tax rates, which range from 10% to 37%. On the other hand, long-term capital gains (for assets held longer than a year) are taxed at 0%, 15%, or 20%, depending on your taxable income.

For higher earners, there’s an added 3.8% Net Investment Income Tax (NIIT) on investment income, including pre-IPO gains. This applies if your Modified Adjusted Gross Income exceeds $200,000 for single filers or $250,000 for married joint filers. This brings the top federal rate for long-term capital gains to 23.8%. If you live in a high-tax state like California, the combined federal and state tax rate on short-term gains can exceed 50%.

Looking ahead to 2026, single filers earning up to $49,450 will pay 0% on long-term capital gains, while those earning over $545,500 will pay the top rate of 20%. Non-Qualified Stock Options (NSOs) are taxed as ordinary income at the time of exercise, potentially at a federal rate of 37%. Meanwhile, Incentive Stock Options (ISOs) allow for deferred taxation until the sale of the stock, provided specific holding periods are met.

Next, let’s explore Section 83(b) elections and ISO holding requirements, which offer additional tax-planning opportunities.

Section 83(b) Elections and ISO Holding Periods

A Section 83(b) election can be a game-changer for equity compensation. It allows you to pay taxes on the value of stock at the time it’s granted, rather than when it vests. This means any future appreciation is taxed as capital gains instead of ordinary income. However, filing this election with the IRS must happen within 30 calendar days of receiving the stock – no exceptions or extensions.

"Missing the 30-day deadline is irreversible." – Promise Legal

For example, a founder who filed an 83(b) election on 1,000,000 shares paid $18,130 upfront and $5,008,130 in total taxes at exit, saving $2,116,870 compared to paying ordinary income tax as the stock vested.

When it comes to ISOs, timing is everything. To qualify for long-term capital gains treatment, you must hold the shares for at least two years from the grant date and one year from the exercise date. Selling too soon results in a "disqualifying disposition", which means the gains are treated as ordinary income. Exercising ISOs can also trigger Alternative Minimum Tax (AMT) liability on the difference between the strike price and the stock’s fair market value. For 2026, federal AMT rates are expected to be 26% on income up to $232,600 and 28% on income above that.

By using tools like Section 83(b) elections and understanding ISO holding periods, you can better manage your tax liability. Strategic timing and planning are key to optimizing pre-IPO tax outcomes.

Tax Strategies for Pre-IPO Investors

Timing and holding periods are critical when it comes to minimizing taxes on pre-IPO gains. For example, exercising options just before a company’s valuation increases can reduce your taxable spread and limit AMT exposure. As Vieje Piauwasdy, Senior Director at Secfi, explains:

"The earlier you exercise, the less upfront cash you need to exercise".

Another strategy involves leveraging Section 1202, which allows for Qualified Small Business Stock (QSBS) exclusions. If certain conditions are met, you can exclude up to 100% of capital gains (capped at $10 million or 10× the basis) if the stock is held for at least five years. However, some states, like California, New York, and Massachusetts, don’t align with the federal exclusion. To qualify, the company must have had less than $50 million in gross assets when the stock was issued – or $75 million for stock issued after July 4, 2025.

Income smoothing is another effective tactic. By dividing large secondary share sales across two tax years – selling half in late 2025 and the other half in early 2026 – you can avoid being pushed into the highest tax brackets. Alternatively, donating highly appreciated shares to a Donor-Advised Fund before an IPO allows you to claim a fair market value deduction while avoiding capital gains taxes altogether.

These strategies show how careful planning can make a significant difference in managing pre-IPO tax burdens.

EU Tax Treatment of Pre-IPO Gains

In the EU, pre-IPO taxation revolves around strict fair value rules, cross-border anti-avoidance measures, and unexpected exit taxes. These mechanisms shape how pre-IPO investors handle their tax obligations and navigate potential pitfalls.

Fair Value Purchase Requirements for Equity

In the EU, acquiring shares below their fair market value can result in a taxable "benefit in kind", which is treated as ordinary income rather than capital gains. This creates the "dry-income" issue – you owe taxes on shares that you can’t sell to cover the liability.

Germany has taken steps to address this. The Future Financing Act now allows tax deferral until the shares are sold, provided the employer agrees to assume wage tax liability. Starting January 1, 2024, the eligibility threshold for startups in Germany will expand to companies with up to 1,000 employees (previously 250) and €100 million in annual revenue. Employees of eligible companies can take advantage of a €2,000 annual tax allowance for qualified equity plans.

"Taxation can now be deferred in full until the shares are finally sold and there is sufficient liquidity to fund the wage taxes payable, provided that the employer agreed to its unrestricted liability." – Alvarez & Marsal

However, Germany’s "long-stop taxation" rule ensures that deferred taxes become due after 15 years if the shares remain unsold, unless further deferral conditions are met. Employees should confirm their company meets the specific "startup" criteria, such as being under 20 years old, to qualify for these tax benefits.

Impact of the Anti-Tax Avoidance Directive (ATAD)

The EU also enforces strict anti-tax avoidance measures. The Anti-Tax Avoidance Directive (ATAD) plays a significant role in how cross-border pre-IPO holdings are taxed. For instance, Article 5 of ATAD I requires member states to tax unrealized capital gains when assets or tax residence are transferred out of a jurisdiction. This ensures that gains generated in one country cannot escape taxation by moving to another.

ATAD II, effective January 1, 2020, targets hybrid mismatches in holding structures. If a holding company is treated as transparent in one country but opaque in another, tax deductions on intercompany payments may be denied. ATAD III takes it further, denying treaty benefits to "shell companies" that lack sufficient substance, such as local employees or physical office space.

"Where taxpayers are not expected to meet the minimum substance tests, they may be denied the benefit of the EU Parent-Subsidiary and the Interest and Royalties Directive… and be subject to higher withholding tax rates." – RSM US

To avoid being classified as a shell company, ensure your entity demonstrates real economic activity – like having local employees, conducting in-person board meetings, and maintaining a physical office. With over 100 jurisdictions participating in automatic financial account information exchanges, pre-IPO holdings are now fully visible to EU tax authorities.

Exit Taxes on Residency Change

Relocating before an IPO can trigger exit taxes on unrealized gains. Countries like France, Germany, Spain, and Belgium impose these taxes on high-net-worth individuals who relocate.

Germany’s 2022 reforms replaced indefinite deferrals for EU/EEA relocations with a 7-year installment payment plan. To qualify, you’ll need collateral, such as real estate or treasury bonds, since shares are often not accepted as security. Belgium, starting January 1, 2026, will impose a 10% tax on capital gains realized by individuals on financial assets.

Some countries offer "returnee" provisions. For example, in Germany, the exit tax may lapse if you return within 7 to 12 years without selling the shares. In Belgium, the timeframe is 24 months. As Thomas Kollruss, an independent tax expert, explains:

"Member States are obliged, under EU law, to grant a full deferral, without interest, of the assessed exit tax until an actual disposal of the shares."

Timing is critical. For those moving to Belgium after January 1, 2026, the market value of assets upon arrival will be considered the acquisition value. This effectively exempts gains accrued before residency. If relocating from Germany, carefully document your intent to return, as this can help you qualify for retrospective exit tax exemptions.

UAE Tax Treatment of Pre-IPO Gains

The UAE stands apart from regions like the US and the EU with its straightforward, investor-friendly tax policies for pre-IPO gains. While the EU has intricate fair value rules and exit taxes, the UAE offers a much simpler zero-tax framework, particularly for personal investments.

Zero Personal Income and Capital Gains Tax

In the UAE, individuals enjoy a 0% personal income and capital gains tax on share sales conducted in a personal capacity. This means investors retain the entire gain without additional deductions or reporting requirements. The same zero-tax treatment applies to dividends and interest income, whether the earnings are domestic or international. Furthermore, there’s no withholding tax on outbound payments, allowing dividends distributed by UAE entities to foreign shareholders to remain untaxed.

As Marc Cantavella, Manager at The Global Wealth, puts it:

"The UAE has built a reputation as one of the world’s most investor-friendly jurisdictions. At the heart of that reputation sits a powerful incentive: individuals in the UAE pay zero capital gains tax on the sale of shares, property, crypto, and other personal investments."

For those using corporate holding structures, the UAE offers a "Participation Exemption". This allows companies to avoid the 9% corporate tax on share disposal gains, provided they hold at least 5% of the entity for a minimum of 12 months. Additionally, Qualifying Free Zone Persons can benefit from a 0% corporate tax rate on qualifying income, including capital gains from such disposals. However, to maintain this zero-tax status, share-trading activities must be personal rather than operating as a systematic business.

While these tax benefits are appealing, they contrast sharply with the obligations that US citizens face, even when residing in the UAE.

US Citizens in the UAE: Worldwide Taxation

US citizens and green card holders are still subject to US taxes on worldwide income, regardless of their UAE residency. Short-term gains are taxed as ordinary income at rates up to 37%, while long-term gains may qualify for preferential rates of 0%, 15%, or 20%. Additionally, high earners face a 3.8% Net Investment Income Tax. Unfortunately, there is no double taxation agreement between the US and the UAE to ease these obligations.

Marc Cantavella explains:

"US citizens and green card holders remain subject to US tax on worldwide income regardless of where they reside. Relocating to the UAE does not eliminate US tax obligations."

US-sourced dividends are also subject to a 30% withholding tax. However, investors can offset gains by deducting up to $3,000 in capital losses annually. Filing requirements include Form 1040 (Schedule D) and Foreign Bank Account Reports (FBAR) for accounts exceeding $10,000 during the year.

Meanwhile, the broader investment landscape in the Gulf Cooperation Council (GCC) region continues to evolve, shaping opportunities for pre-IPO investors.

IPO Market Trends in the GCC

The UAE is positioning itself as a low-tax, high-compliance jurisdiction. Since introducing federal corporate tax in 2023 and implementing stronger anti-money laundering measures, the country has been removed from the FATF grey list. By 2026, the UAE will roll out the Crypto-Asset Reporting Framework (CARF) and updated Common Reporting Standards (CRS 2.0) to enhance transparency in digital asset holdings.

The UAE has also signed over 130 double taxation agreements to encourage international investment. Its Golden Visa program offers a clear path to residency, and regulatory bodies like VARA in Dubai and FSRA in Abu Dhabi provide robust oversight, reinforcing the UAE’s appeal as a hub for tech-driven pre-IPO equity.

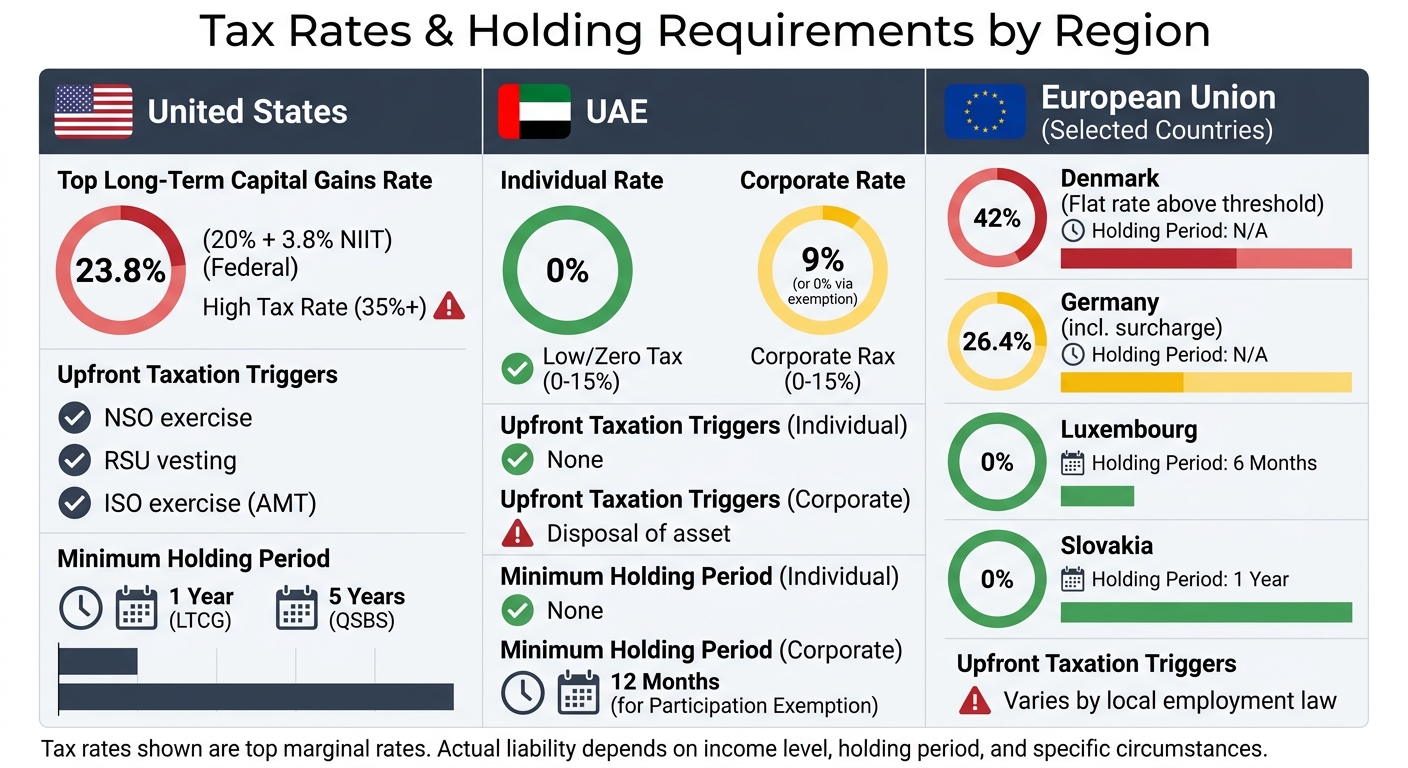

Comparison of Tax Rates and Holding Requirements

Pre-IPO Tax Rates and Holding Requirements: US vs EU vs UAE Comparison

Tax policies on pre-IPO gains differ widely depending on the jurisdiction, with each region applying its own rules for holding periods and tax rates. In the US, for instance, failing to meet the one-year holding period for long-term capital gains can push the federal tax rate from 20% to a hefty 39.6% starting in 2026, significantly cutting into profits. Meanwhile, individuals in the UAE enjoy a 0% personal capital gains tax with no required holding period. In the EU, tax rates range broadly – from 0% in countries like Luxembourg and Slovakia (after relatively short holding periods) to as high as 42% in Denmark.

Tax Rates and Requirements by Region

Here’s a breakdown of how tax rates and holding requirements vary across key regions:

| Region | Top Long-Term Capital Gains Rate | Upfront Taxation Triggers | Minimum Holding Period for Best Rate |

|---|---|---|---|

| United States | 20% + 3.8% NIIT (Federal) | NSO exercise, RSU vesting, ISO exercise (AMT) | 1 Year (LTCG); 5 Years (QSBS) |

| UAE (Individual) | 0% | None | None |

| UAE (Corporate) | 9% (or 0% via exemption) | Disposal of asset | 12 Months (for Participation Exemption) |

| Denmark | 42% | Varies by local employment law | N/A (Flat rate above threshold) |

| Germany | 26.4% (incl. surcharge) | Varies by local employment law | N/A |

| Luxembourg | 0% | Varies by local employment law | 6 Months |

| Slovakia | 0% | Varies by local employment law | 1 Year |

This table highlights just how varied tax obligations can be, making it essential to understand the specifics of each region. For example, US investors often face multiple taxation events, such as those triggered by NSO exercises or RSU vesting, while UAE individuals are exempt from personal capital gains taxes entirely. UAE corporations, however, are subject to a 9% tax on income over AED 375,000 unless they qualify for the Participation Exemption, which requires holding at least 5% of a company for 12 months.

In the EU, the tax landscape is even more diverse. Belgium plans to tax share capital gains exceeding €10,000 at 10% starting in 2026, while the Czech Republic has removed its cap on capital gains exemptions, effectively making the rate 0% for long-held shares. Some countries, like Slovenia, require a holding period of up to 15 years to achieve a 0% rate, whereas Luxembourg offers full exemption after just six months. In stark contrast, the UAE has no holding period requirements for individuals, making it one of the most flexible jurisdictions for managing pre-IPO gains.

Compliance Strategies and Tax Optimization

Navigating pre-IPO gains requires careful planning to reduce tax liabilities and stay compliant. This section highlights how strategic decisions and managing residency can help make the most of your tax situation.

Tax Residency Shifts and Exemptions

Relocating to low-tax regions can significantly lower your tax obligations, but it requires precise timing and documentation. For instance, US-based founders moving to states like Florida, Texas, or Nevada – where there’s no state income tax – should be mindful of when and where their equity was earned. States like California and New York may tax equity based on where the work occurred during the vesting period. Keeping a daily log of work locations can help substantiate your tax position.

For those considering a move to the UAE, meeting the Economic Substance Regulations is key to qualifying for the 0% corporate tax rate. This involves maintaining a physical presence, hiring local staff, and making local decisions. Additionally, obtaining a UAE Tax Residency Certificate is critical for accessing benefits under the country’s extensive double taxation agreements. However, US citizens remain subject to worldwide taxation, making pre-immigration planning essential. Non-residents moving to the US can use a "realization event" to reset the cost basis of their assets to fair market value before establishing residency, avoiding US tax on prior appreciation. As Ipanema Partners points out:

"The moment you get that green card… the IRS wants to know about every bank account, investment, business, and trust you own, anywhere on the planet".

In Europe, exit taxes can be a major concern. For example, in France, relocating founders may face a tax of up to 30% on gains exceeding €800,000. To legally sever tax ties, founders must deregister with local authorities, address property ownership, and shift business management to avoid failing the "center of vital interests" test. European tax authorities are increasingly leveraging the Common Reporting Standard (CRS) to track individuals moving to the UAE, which could trigger retroactive exit taxes.

Section 83(b) Elections and EU Equivalents

As discussed earlier, Section 83(b) elections can be a valuable tool, but there are additional strategies to consider. For those holding Qualified Small Business Stock (QSBS), Section 1202 offers a federal tax exclusion on gains – up to $10 million or 10 times the basis – if the shares were acquired after September 27, 2010, and held for at least five years. However, California does not recognize this exemption, meaning residents may still face state taxes of up to 13.3%.

Up-C structures have become increasingly popular for companies seeking public market access while retaining pass-through tax benefits. Over the past five years, more than 50 companies have used Up-C or Up-SPAC structures, which allow pass-through entities to go public and share tax benefits with pre-IPO investors through Tax Receivable Agreements (TRAs). For those with unrealized gains, Charitable Remainder Trusts (CRTs) can help defer taxes and reinvest gross proceeds, while Charitable Lead Trusts (CLTs) provide immediate tax deductions – up to 50% of income – for realized gains.

In parts of the EU, some jurisdictions allow founders to defer taxes on equity grants until the assets are sold, provided specific conditions are met. However, navigating these rules can be complex, with cross-border tax advisory costs often ranging from €5,000 to €15,000 annually.

Phantom Income and Compliance Challenges

Phantom income – tax on unrealized gains – can create liquidity problems. Incentive Stock Options (ISOs), for example, can trigger Alternative Minimum Tax (AMT) on unrealized gains. Spreading option exercises over two to three years can help avoid crossing AMT thresholds.

US taxpayers holding shares in foreign startups may also face challenges under the Passive Foreign Investment Company (PFIC) regime, where gains are taxed as ordinary income – up to 37% – plus interest charges. A Qualified Electing Fund (QEF) election allows taxpayers to report annual earnings and preserve capital gains treatment upon sale. Immigrants establishing US residency should consider liquidating foreign mutual funds or ETFs beforehand to avoid punitive interest charges that could exceed 100% of the gain. Filing IRS Form 8832 to "check-the-box" before residency begins can simplify matters by treating foreign corporations as disregarded entities, avoiding the complexities of Controlled Foreign Corporation (CFC) and GILTI tax rules.

Section 409A violations can also create phantom income risks. If a company issues options below fair market value, US employees could face a 20% federal penalty tax plus interest. To avoid this, companies should secure independent 409A valuations annually or after significant events to meet safe harbor requirements.

Lastly, income smoothing can help manage tax bracket creep. For instance, splitting a large secondary share sale across the December 31st boundary – selling part in late 2025 and the rest in early 2026 – can prevent being pushed into the highest marginal tax bracket for the entire gain. As the Calcix Research Team advises:

"Don’t let the ‘tax tail’ wag the ‘investment dog,’ but do use the 2026 tax brackets to decide exactly how many shares to liquidate".

Conclusion

Regional Differences in Tax Treatment

When comparing tax treatments across regions, the US, EU, and UAE reveal striking differences that demand careful planning. In the US, short-term capital gains will face federal rates as high as 39.6% in 2026, alongside a 3.8% Net Investment Income Tax and potential state taxes, which could climb to 13.3% in California. Long-term capital gains are taxed at 0%, 15%, or 20%, and Section 1202 (QSBS) provides an opportunity to eliminate federal taxes on up to $10 million in gains if the stock is held for five years.

In the UAE, personal income and capital gains taxes are nonexistent, though US citizens remain subject to worldwide taxation. Europe presents a patchwork of regulations across its 30 countries. For instance, Estonia, the UK (via the EMI scheme), and France (through BSPCE) offer favorable tax incentives, while other nations impose taxes both at the time of exercise and sale.

Interestingly, European employees in late-stage startups typically hold around 10% of the company, compared to 20% for their US counterparts.

"The Silicon Valley attitude is: we’re asking people to go on an adventure with us. If we find treasure, everyone deserves a piece"

This cultural difference shapes not only ownership structures but also the tax policies that apply before companies go public.

Next Steps for Investors

Given these regional distinctions, here are some practical steps to refine your tax strategy. If you’re moving between tax jurisdictions, document your work location carefully, as states may claim taxing rights during the vesting period. For US investors, filing a Section 83(b) election within 30 days of a grant and exercising ISOs during lower-income years can help minimize exposure to the Alternative Minimum Tax.

If considering a residency change, familiarize yourself with rules on trailing nexus and potential exit taxes before relocating. By 2026, state tax authorities are expected to increase audits on high-value secondary transactions, especially for individuals moving from high-tax to tax-free states.

When selling shares, timing is key. Use the 2026 tax brackets to determine how many shares to sell without pushing into a higher tax bracket. Selling 10–20% of your stake on secondary markets after the one-year holding mark can lock in long-term capital gains rates and hedge against post-IPO market fluctuations.

For a well-rounded strategy, consult tax advisors who specialize in cross-border equity compensation. Their expertise can help you navigate QSBS eligibility, residency transitions, and other complex scenarios, ensuring you avoid errors and maximize your after-tax returns.

FAQs

When should I exercise options before an IPO to reduce taxes?

To cut down on taxes, it’s a good idea to exercise your stock options early – preferably before the company goes public. At this stage, the company’s valuation is typically lower, which reduces the "bargain element" (the difference between the stock’s market value and the exercise price). This, in turn, helps limit potential tax liabilities, including the Alternative Minimum Tax (AMT).

Can moving countries (or states) before an IPO trigger an exit tax?

Relocating before an IPO can sometimes lead to an exit tax, especially if the move is seen as a taxable event. Certain countries – such as France, Germany, and the Netherlands – may impose taxes on unrealized gains, treating them as though the assets were sold. Additionally, moving equity can trigger sourcing rules and even immediate taxation upon leaving, depending on the specific regulations of the jurisdiction.

How do I know if my pre-IPO shares qualify for QSBS?

To see if your pre-IPO shares meet the criteria for Qualified Small Business Stock (QSBS) under IRC Section 1202, make sure they satisfy these conditions:

- U.S. C-Corporation: The stock must be issued by a U.S.-based C-Corporation with gross assets of $75 million or less.

- Issuance Date: Shares need to have been issued on or after July 4, 2025, and held for the required period (typically 3 to 5 years).

- Original Issuance: You must have acquired the stock directly from the company, not through a secondary market transaction.

Since tax rules can be complex, it’s a good idea to consult a tax professional to confirm your shares qualify.