Restaking lets you earn more from staked ETH by securing multiple protocols, but it comes with higher risks. EigenLayer, the leader in this space with $18 billion in locked value by early 2026, offers a marketplace connecting stakers, node operators, and services (AVSs). While restaking can boost yields to 8–12% annually, it introduces risks like slashing penalties, correlated losses, and operator failures. Institutions must carefully manage exposure, diversify operators, and monitor performance to balance returns and risks. For safer participation, limit restaking to 5–25% of your ETH holdings and consider insurance or technical safeguards.

Key points:

- Yields: Base staking (3.5–4%) + AVS fees + token rewards.

- Risks: Slashing (Ethereum & AVS-specific), operator failures, and liquidity delays.

- Options: Native restaking (requires 32 ETH) vs. liquid restaking (via LSTs, easier but riskier).

- Mitigation: Diversify operators, cap exposure, monitor performance, and use insurance.

Restaking is not "free APY." Treat it as lending your security and price the risks accordingly.

Sreeram Kannan & Kartik Talwar I Restaking Risks with EigenLayer I Pragma Denver 2024

sbb-itb-7e716c2

How Restaking Works in EigenLayer

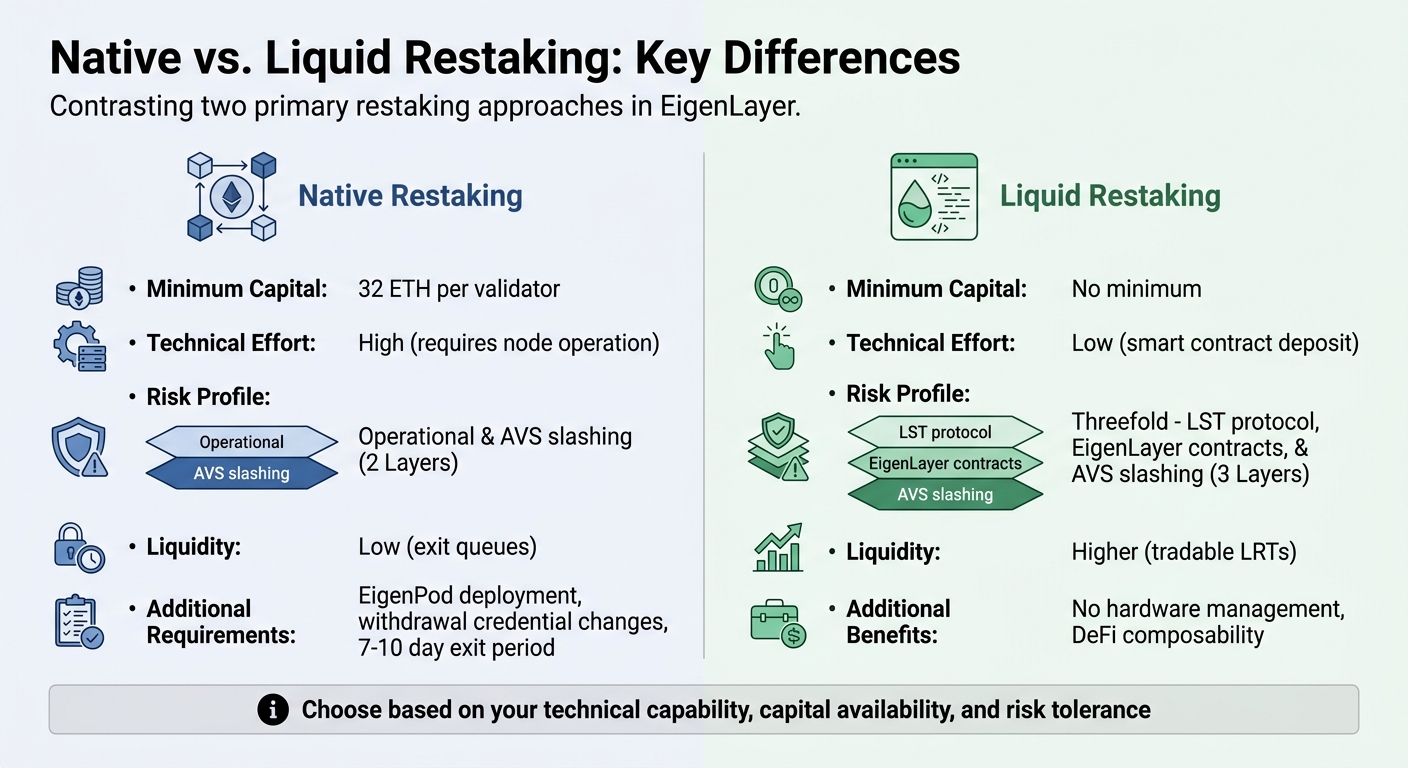

Native vs Liquid Restaking Comparison: Capital Requirements, Risk Profiles, and Liquidity

EigenLayer functions as a three-sided marketplace, connecting three key participants: restakers (those providing capital), operators (node runners), and Actively Validated Services (AVSs) that require added security layers. Instead of building a validator network from scratch, these services leverage Ethereum’s existing security framework. The process is straightforward: deposit capital, delegate it to a qualified operator, and earn layered yields. Let’s break down the different restaking approaches and how they affect risk and potential returns.

At the heart of this system are two main participants. Restakers deposit ETH or Liquid Staking Tokens (LSTs) and delegate them to operators – professional node runners who manage AVS infrastructure. Operators typically charge a commission of 5–15% for their services. This setup allows institutions to participate without running their own validator nodes, though that option remains open for those who want direct control.

Native Restaking vs. Liquid Restaking

The choice between native and liquid restaking significantly impacts your risk exposure and operational effort.

Native restaking involves running an Ethereum validator node, which requires a minimum of 32 ETH per validator. Validators must redirect their withdrawal credentials to an "EigenPod" smart contract, which monitors balances and enables EigenLayer to track the stake. While this approach avoids risks tied to LST protocols, it demands technical expertise and locks capital in validator exit queues.

On the other hand, liquid restaking simplifies the process. By depositing LSTs like stETH or rETH into EigenLayer’s smart contracts, you avoid hardware management and bypass minimum deposit requirements. However, this convenience comes with a threefold risk profile: exposure to the LST protocol, EigenLayer’s smart contracts, and AVS-specific slashing risks. Liquid restaking also provides flexibility through Liquid Restaking Tokens (LRTs), which can be traded or used in DeFi protocols.

| Feature | Native Restaking | Liquid Restaking |

|---|---|---|

| Minimum Capital | 32 ETH per validator | No minimum |

| Technical Effort | High (requires node operation) | Low (smart contract deposit) |

| Risk Profile | Operational & AVS slashing | LST protocol, EigenLayer, & AVS slashing |

| Liquidity | Low (exit queues) | Higher (tradable LRTs) |

Native restakers also face additional steps, such as completing a "Checkpoint Proof" process to convert validator ETH into restaked shares. This process can take days due to exit queue delays. Validators with 0x01 execution layer withdrawal addresses must fully exit the beacon chain and redeploy with EigenPod credentials, further extending the timeline.

How Yields Are Generated

Restaking in EigenLayer generates yields across three distinct layers, each with its own payment mechanism:

- Base Ethereum Staking Rewards

Restakers earn the standard Ethereum staking yield of approximately 3–4% annually. This comes from consensus participation and execution layer fees and remains consistent regardless of restaking activities. - AVS Protocol Fees

Additional fees are paid by AVSs for the security provided. These fees can be in ETH, stablecoins, or the AVS’s native token, depending on the service. For instance, EigenDA compensates operators for providing data availability bandwidth to Layer 2 rollups like Celo and Mantle. During production testing in December 2025, EigenDA achieved a peak throughput of 1 GB/s across 100 global operators. - Protocol Incentives

EigenLayer also rewards participants through its "restaked points" system and the EIGEN token, which launched in October 2024. EIGEN incentivizes "intersubjective staking", which resolves disputes about off-chain behavior that cannot be fully verified through cryptographic proofs.

"Restaking is not ‘free APY.’ Treat it as secured lending of your trust. Price the extra yield against the specific slashing surface you’re assuming." – TokenToolHub Guide

Depending on the AVSs you select, your total APY can vary from modest to highly aggressive configurations. However, each additional AVS introduces new slashing conditions, making careful operator selection and ongoing monitoring essential for managing risk effectively.

Risk Factors for Institutional Allocators

Restaking introduces a complex risk structure that goes far beyond traditional Ethereum staking. While the allure of 7–12% net yields might attract institutional investors, the potential downsides require careful scrutiny. By February 2026, EigenLayer’s total value locked had exceeded $25 billion, with nearly $5 billion tied up in leverage through Liquid Restaking Tokens (LRTs). This concentration of capital heightens the consequences of any single failure within the ecosystem.

The risks can be grouped into three main categories: direct slashing penalties, correlated loss propagation, and broader effects on Ethereum’s consensus security. Institutions must carefully evaluate these interconnected risks before committing resources. Let’s break down the key risk areas and explore potential mitigations.

Slashing Risks and How to Reduce Them

Restakers face a dual-layer slashing risk. Assets are vulnerable not just to Ethereum’s base-layer consensus rules – like penalties for downtime or double-signing – but also to additional conditions specific to AVS (Active Validator Set) operations, such as oracle failures or data availability issues. A single error could result in penalties on both layers.

Unintended slashing poses a particularly serious threat. Honest operators can face penalties due to programming bugs, network disruptions, or misconfigurations rather than malicious activity. During EigenLayer’s initial phase, a Protocol Council of Ethereum experts reviews slashing incidents and can veto penalties deemed unjustified. However, institutions should not rely on this temporary governance safety net indefinitely.

Collusion among operators adds another layer of risk. If a quorum of operators – potentially as low as 50% – collaborates to attack an AVS, their success depends on whether the Profit-from-Corruption outweighs the Cost-of-Corruption. With the top 10 operators controlling 40–60% of delegated stake as of March 2026, the failure of a single operator could have widespread consequences.

To mitigate these risks, institutions should consider the following strategies:

- Limit exposure: Cap restaking allocations to 5–25% of total ETH holdings to reduce the impact of slashing cascades.

- Diversify operators: Delegate stakes across 5–10 operators with strong track records. For example, P2P.org ($3.2 billion delegated) and Figment ($1.7 billion delegated) have achieved uptimes of 99.98%–99.99% with no recorded slashing incidents.

- Evaluate infrastructure: Choose operators with multi-region setups and avoid reliance on single-provider solutions.

- Use monitoring tools: Implement real-time tracking with predefined exit triggers, such as repeated downtime or significant shifts in slashing economics.

- Adopt technical safeguards: Technologies like Unique Stake Allocation can isolate assets per AVS, minimizing the risk of widespread slashing.

- Consider insurance: AVS-specific slashing insurance, typically priced at 1–2% annual premiums, can further limit downside risk.

Correlated Loss and System-Wide Risk

Restaking introduces the potential for correlated losses that can ripple through an entire portfolio. When multiple AVSs are secured with the same ETH collateral, a failure in one AVS can cascade into penalties across all shared stakes. Simulations indicate that a 5% loss in one AVS could translate into a 20–30% portfolio loss due to high correlation.

LRTs add another layer of complexity. With $5 billion in leverage, these tokens create a structure reminiscent of pre-2008 Collateralized Debt Obligations (CDOs), where nested positions obscure the true level of risk. During periods of market stress, this leverage can trigger cascading liquidations across lending platforms and decentralized exchanges.

"LRTs have baked in $5B leverage, mirroring pre-2008 CDO opacity. Transparency erodes as nested positions obscure true risk." – Owen Maddox, Technical Analyst

Operator concentration compounds these risks. A single operator’s failure could simultaneously affect multiple AVSs. To mitigate this, institutions should:

- Diversify across AVSs: Secure stakes in 3–5 uncorrelated AVSs to balance risk and returns. Exceeding 10 AVSs can increase exposure to tail risks.

- Avoid overlapping dependencies: Select operators with distinct infrastructure to minimize shared vulnerabilities, such as reliance on the same cloud providers or software clients.

Impact on Ethereum Consensus Security

The risks tied to operator failures and correlated losses can strain Ethereum’s consensus mechanism, creating systemic vulnerabilities. Large-scale restaking challenges Ethereum’s base layer by introducing complex, subjective faults from interconnected AVSs – issues the network was not originally designed to handle. With restaking TVL nearing $25 billion, these stresses are becoming more pronounced.

To address these challenges, the EIGEN token was introduced. This token enables a "slashing-by-forking" mechanism, adding a secondary security layer. However, this approach also introduces governance complexities that could disrupt validator incentives during contentious disputes.

"When the cost of corruption is significantly higher than the Profit-from-Corruption (PfC), the system is thought to be extremely secure." – Peter Schöllauf, Research, DAIC Capital

Centralization is another major concern. If a small group of institutional operators gains control over the majority of restaked ETH, they could manipulate AVS outcomes or extract excessive fees, mirroring the centralization issues seen in traditional finance. Institutions must evaluate whether their restaking activities contribute to systemic fragility. Allocating to operators with decentralized practices – such as stake caps, open-source tools, and transparent governance – can help mitigate these risks.

Liquidity risks also play a role. Unstaking delays in AVSs can extend weeks beyond Ethereum’s standard churn limits as of 2026. This delay forces holders to sell at unfavorable prices during market volatility, adding another layer of complexity. The next section will outline a detailed framework for managing these risks effectively.

Risk Management Framework for Institutions

Institutions engaging in restaking must implement a well-structured risk management framework. With over $15 billion in Total Value Locked (TVL) and more than 4.3 million ETH restaked as of early 2026, the stakes are high. This framework builds on key risks like slashing and correlated losses, offering actionable steps to mitigate exposure. A tailored approach is essential, addressing both Ethereum consensus penalties and AVS-specific risks. The framework focuses on three main pillars: defining risk boundaries, continuous performance monitoring, and thorough due diligence.

Mapping Risk Boundaries and Exposure

To start, calculate the Cost of Corruption (CoC) threshold for each AVS. This metric reflects the capital an attacker would need to compromise the AVS. The system remains secure as long as CoC significantly exceeds the potential Profit-from-Corruption (PfC). Research suggests that diversifying across 3–5 uncorrelated AVSs strikes the best balance between risk and return, while exposure to 10 or more services introduces considerable tail risk.

Position sizing is critical. Limit restaking allocations to 5–25% of total ETH holdings to avoid concentration risk. Divide your capital into "core reserves" (low-risk, liquid assets) and "productive treasury" (assets allocated for staking and yield generation). Keep a close watch on operator concentration; by late 2024, the top 10 operators controlled about 60% of the delegated stake, creating potential systemic vulnerabilities.

Use cryptoeconomic dashboards to evaluate operator capacity and ensure that risk boundaries are well-defined. Once these boundaries are set, focus on continuous performance monitoring to catch potential issues early.

Monitoring Validator Performance

Real-time monitoring is a hallmark of proactive risk management. Set up 24/7 alerts to track uptime, client diversity, and geographic distribution across cloud providers.

Keep an eye on your "productive stake" at all times. Passive deposits typically yield less than active participation. Establish clear exit criteria for situations like repeated downtime, sudden changes in operator exposure, or shifts in slashing economics. Don’t forget to account for EigenLayer’s withdrawal delay, which typically takes 7 days. This escrow period should factor into your liquidity planning.

Alongside real-time tracking, ensure that rigorous due diligence is a constant part of your strategy.

Due Diligence Process for Restaking

Ongoing due diligence is non-negotiable. Start by ensuring that each AVS codebase has undergone multiple independent security audits. Even honest operators are vulnerable to unintended slashing caused by programming bugs or configuration errors.

Examine the reputation and governance structure of each AVS. Pay particular attention to slashing contracts, as extreme penalties could result in validators losing up to 100% of their restaked ETH.

Consider the role of EigenLayer’s veto committee, a reputation-based body that can overturn unjustified slashing events. While this provides some protection during the protocol’s early stages, it should not be relied upon as a long-term safety measure.

Distinguish between sustainable yields generated from AVS service fees and temporary yields driven by token emissions. As the ecosystem matures, sustainable yields are expected to stabilize in the 5–10% range. Operators offering higher yields (8–12% or more) often carry significantly higher slashing risks. Lastly, verify operator infrastructure by reviewing disaster recovery plans, hardware diversity, and transparency in incident reporting.

"Restaking is not only about ‘more yield.’ It’s about choosing what you’re underwriting." – EigenCloud

Implementation and Market Analysis

Implementation Challenges and Security Requirements

Getting started with native restaking involves some serious technical adjustments. Institutions opting for this route must run a full Ethereum validator node, which requires a minimum of 32 ETH, and deploy an EigenPod – a specialized smart contract that tracks balances and withdrawal statuses. For existing validators, there’s an additional hurdle: they must exit their current setup and redeploy under EigenPod credentials. This process results in a 7–10 day gap in rewards.

"For native restaking of an existing Ethereum validator, it would need to be exited and redeployed, since the withdrawal credential cannot be changed per the protocol security rules" – Freddy Zwanzger, Blockdaemon

For those looking to avoid this complexity, liquid restaking offers a simpler alternative. By depositing Liquid Staking Tokens (LSTs) like stETH, rETH, or cbETH into EigenLayer contracts, institutions can bypass the need for validator hardware. However, liquid restaking comes with its own risks, primarily related to the smart contracts involved. These include vulnerabilities in the EigenLayer core, EigenPod, AVS-specific contracts, and Liquid Restaking Token (LRT) contracts.

Once capital is committed, the entire restaked balance must be allocated to a single operator for each AVS. Each AVS also requires its own off-chain node software. A critical point to note: the address that deploys an EigenPod retains permanent ownership, meaning restaking and withdrawal permissions cannot be transferred.

With these technical and security considerations in mind, it’s essential to evaluate how these factors influence market dynamics and adoption.

Market Adoption and Performance Metrics

After implementation, keeping a close eye on market trends and performance metrics is key. The challenges tied to setup and security directly shape investor confidence and adoption.

EigenLayer currently dominates the restaking market. By March 2026, it held over $15 billion in Total Value Locked (TVL), accounting for about 94% of the overall restaking market. More than 4.3 million ETH has been restaked, with participants earning cumulative rewards exceeding $28 million. Interestingly, Liquid Restaking Tokens now make up roughly 70% of EigenLayer’s TVL.

That said, growth has been anything but steady. Daily active deposit users dropped dramatically – from thousands in mid-2024 to fewer than 30 by 2025. Similarly, token prices for major restaking projects saw a steep decline, falling over 70% from their peaks during the same period. This volatility highlights a major challenge: evaluating performance remains tricky. Early AVS yields ranged from 5–15%, but as the market matures, returns are expected to stabilize between 3.8% and 6%. Operators promising higher yields of 8–12% or more often come with elevated slashing risks.

For institutions, monitoring "productive stake" is essential. This refers to capital actively securing live AVSs, which is the only type of stake eligible for maximum EIGEN token incentives. Another critical metric is operator concentration. By late 2024, the top 10 operators controlled roughly 60% of delegated stake, raising concerns about systemic risks. Withdrawal delays are another factor to consider, as they include both Ethereum’s standard unstaking period and additional escrow windows for resolving AVS slashing disputes. To manage these risks, most institutions now cap their restaking exposure at 10–20% of their total Ethereum staking positions.

Conclusion

EigenLayer’s restaking framework presents a way to earn attractive yields, but it comes with layered risks that must be carefully evaluated. For institutional allocators, restaking offers an opportunity to achieve approximately 5–10% total APY by extending Ethereum’s security to Actively Validated Services (AVSs). However, this potential yield is paired with risks like consensus failures, AVS-specific slashing, and operator performance issues . Rather than viewing it as a route to "free returns", restaking should be approached as a securitized lending arrangement.

As of March 2026, EigenLayer commands 94% of the restaking market, with over $15 billion in Total Value Locked – a testament to market confidence. Despite this, the possibility of slashing events, which can result in the loss of up to 100% of restaked assets, underscores the need for conservative position sizing . Institutions are generally advised to limit their restaking exposure to 5–25% of their total ETH holdings to manage potential losses effectively.

"EigenLayer is one of the most strategically important crypto primitives because it turns Ethereum security into a programmable market. That matters far beyond yield. It creates new infrastructure business models." – Ali Hajimohamadi, Founder, Startupik

Operational choices also play a critical role in implementing restaking strategies. Native restaking through EigenPods avoids asset co-mingling but requires technical expertise and a minimum of 32 ETH per validator . On the other hand, liquid restaking via Liquid Restaking Tokens (LRTs) provides a simpler entry point but introduces additional risks, such as smart contract vulnerabilities and potential depegging . Institutions should prioritize AVSs that reward in ETH or stablecoins and remain aware of extended withdrawal windows, which can exceed standard Ethereum unstaking periods .

Restaking should complement, not replace, an institution’s core treasury management strategy. It can be positioned as a "Productive Treasury" or a form of "Strategic Ecosystem Exposure" for those willing to take on the associated risks. However, institutions with lower risk tolerance or higher liquidity needs may find standard Ethereum staking a more suitable option. Thorough due diligence on operators and careful consideration of illiquidity are essential for success in this space.

FAQs

How do I choose which AVSs to restake into?

When picking AVSs (Actively Validated Services) for restaking, it’s crucial to dive into a few key factors. Start by understanding their primary purpose – are they focused on tasks like data availability or oracles? Each service will have different roles, and knowing this helps you align your goals.

Next, evaluate their security models and potential risks, such as slashing. Slashing can result in losing a portion of your staked assets, so it’s important to weigh this carefully. Look into how robust their verification processes are and check the reputation of the operators running these services. Operators with a strong track record and transparent practices tend to be more reliable.

Lastly, consider the complexity of the tasks these AVSs handle. Choose services that match your comfort level with risk and ensure they’re run by entities you trust. Transparency and clear mechanisms are key indicators of trustworthy operations.

What should I consider when selecting EigenLayer operators?

When selecting EigenLayer operators, it’s important to assess their track record, dependability, and security measures. Look into how they handle protocol upgrades and governance, as these factors play a key role in ensuring stability. To minimize systemic risks, consider spreading your stakes across multiple operators. Focus on operators with solid risk management frameworks, particularly in managing slashing events and maintaining clear, open communication. Take the time to perform thorough research to confirm the operator meets your security and governance standards.

How can I model worst-case losses from slashing and withdrawal delays?

To understand potential worst-case losses, it’s essential to evaluate risks such as correlated slashing cascades. This occurs when the failure of one AVS (Active Validator Set) leads to penalties spreading across multiple protocols. Here’s how to approach this:

- Identify interconnected AVSs: Map out how different validator sets are linked to pinpoint areas of potential cascading failures.

- Estimate slashing probabilities: Analyze the likelihood of slashing events, especially during periods of instability.

- Factor in penalties and delays: Consider the impact of slashing penalties and withdrawal delays, such as liquidity lock-ups, on overall losses.

By simulating these elements, you can better estimate potential losses and develop strategies to reduce risks. Approaches like diversification and conducting regular risk assessments can play a key role in minimizing exposure.