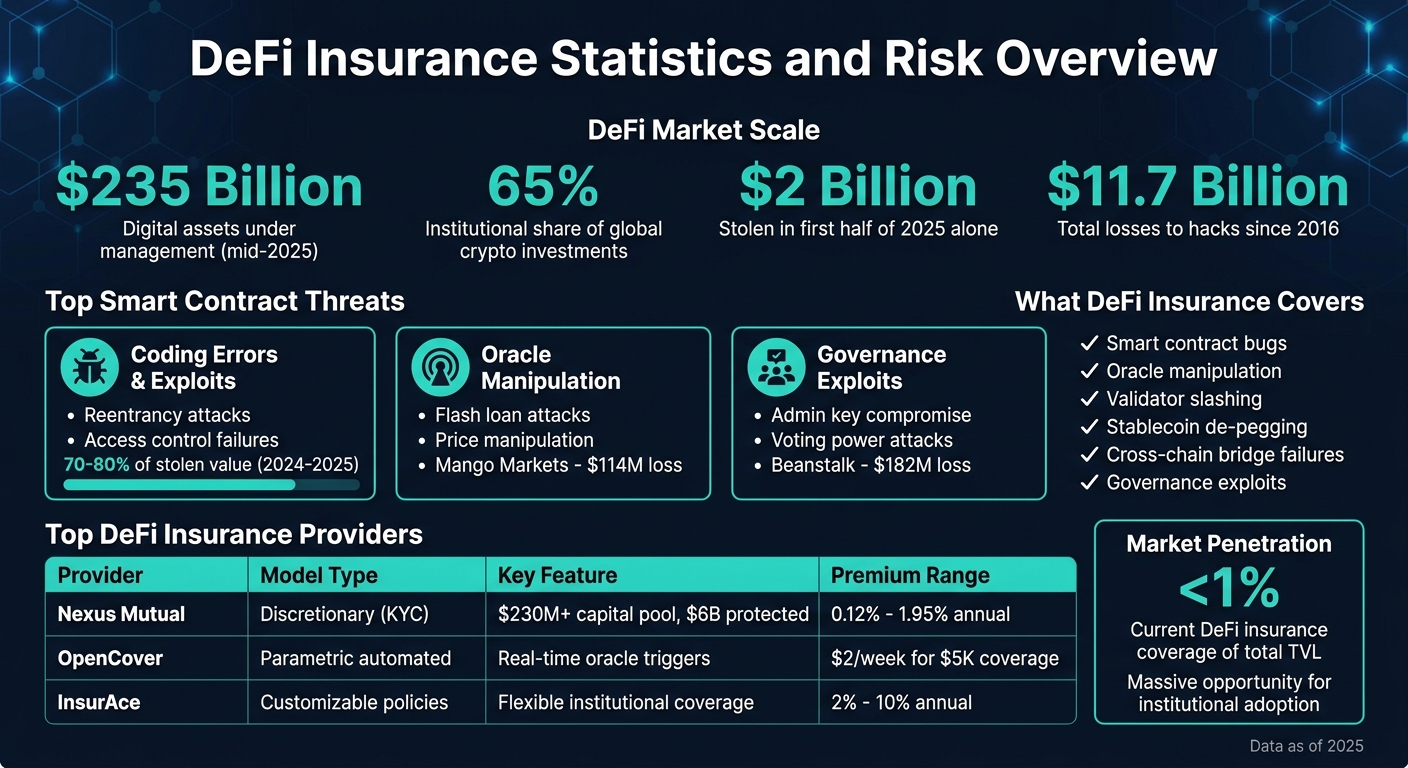

As decentralized finance (DeFi) continues to attract institutional investors, managing risks tied to smart contracts has become a top priority. With over $235 billion in digital assets under management by mid-2025 and institutions accounting for 65% of global crypto investments, the stakes are high. Common vulnerabilities like reentrancy attacks, oracle manipulation, and governance exploits have already caused billions in losses, with $2 billion stolen in just the first half of 2025.

DeFi insurance offers a solution by covering risks such as smart contract bugs, stablecoin de-pegging, and cross-chain bridge failures. Automated claims and decentralized governance make payouts faster and more transparent. Providers like Nexus Mutual, OpenCover, and InsurAce are leading the way, offering tailored policies for institutions.

Key Takeaways:

- Risks: Smart contract flaws, oracle failures, governance exploits.

- Losses: Over $11.7 billion lost to hacks since 2016.

- Insurance Coverage: Includes oracle manipulation, validator slashing, and stablecoin de-pegging.

- Leading Providers: Nexus Mutual, OpenCover, InsurAce.

Institutions can combine DeFi insurance with strategies like third-party audits, diversification, and regulatory compliance to safeguard their capital. While insurance isn’t a cure-all, it’s a critical layer in a broader risk management framework.

DeFi Insurance Market Statistics and Risk Landscape 2025

Decentralized insurance explained. Can smart contracts cover disasters?

sbb-itb-7e716c2

Smart Contract Risks That Threaten Institutional Capital

To protect their capital effectively, institutions need to grasp the various smart contract risks that DeFi insurance is designed to address.

Coding Errors and Security Exploits

Flaws in smart contract code can leave institutional funds vulnerable to direct attacks. A prime example is reentrancy attacks, where a contract hands over control to an external address before finishing its internal processes. This loophole allows attackers to repeatedly withdraw funds. Modern variations – like cross-function, cross-contract, and read-only reentrancy – make these exploits even harder to detect.

Another critical issue is access control failures. Misconfigured permission checks or function visibility can allow attackers to execute privileged actions meant only for administrators. For instance, in February 2025, Bybit experienced a massive theft of approximately $1.5 billion in ETH. Attackers exploited vulnerabilities in key and approval workflows, enabling large unauthorized transfers without directly exploiting the code itself.

Between 2024 and 2025, access control failures, private key compromises, and governance exploits accounted for 70–80% of stolen value, overshadowing simple coding mistakes. As Wijdan Khaliq, Education Lead at Coin Bureau, explains:

Instead of one obvious bug, attackers often chain together smaller weaknesses across connected systems to create a much larger failure.

Institutions must also be vigilant against risks involving external data manipulation, which can further complicate the landscape.

Oracle Manipulation and Data Failures

Smart contracts depend on external oracles to provide real-world data, such as asset prices. This reliance creates a major vulnerability. Attackers can use flash loans to borrow large sums, manipulate prices in low-liquidity pools, and force oracles to report false information. Once the protocol acts on this incorrect data, it can lead to drained liquidity or borrowing against inflated collateral.

A notable example occurred in October 2022 when Mango Markets lost $114 million. An attacker manipulated the price oracle for the MNGO token, artificially inflating its value to borrow and drain the protocol. This case highlights a broader issue: DeFi insurance protocols often use the same oracles as the platforms they cover. As ChainScore Labs points out:

The oracle is the policy. The reliability of a Nexus Mutual or InsurAce claim payout is not a function of their smart contract code, but of the data feed from Chainlink or Pyth.

Data staleness and network congestion introduce additional risks, such as incorrect liquidations or arbitrage opportunities caused by price gaps. For institutions managing significant DeFi portfolios, these oracle-related issues represent threats that traditional audits may fail to address. Beyond oracles, governance vulnerabilities pose another layer of risk.

Governance Exploits and Protocol Breakdowns

Governance mechanisms, intended to decentralize decision-making, have become attractive targets for attackers. By compromising admin keys or acquiring enough voting power, attackers can pass harmful proposals to drain treasuries, change key parameters, or seize control.

In April 2022, the Beanstalk protocol fell victim to a $182 million attack. The attacker used a flash loan to temporarily gain a voting majority and passed a proposal to drain the treasury. The protocol operated as designed, but its governance structure exposed a critical design flaw.

For institutions, governance exploits can cause more than financial losses. They can disrupt operations, delay Net Asset Value reporting, and lead to inaccurate fund statements. The Immunefi Foundation underscores the challenge:

Humans cannot reliably defend systems that operate at machine speed. Manual triage, governance approvals, and ad-hoc coordination introduce delays that attackers exploit systematically.

As smart contract auditing becomes more robust, attackers are shifting their focus to the people and systems managing the keys. Social engineering and credential theft are growing threats, emphasizing the need for institutions to safeguard not just their funds but the entire operational ecosystem surrounding their DeFi investments. Addressing these interconnected risks underscores the importance of comprehensive DeFi insurance solutions.

How DeFi Insurance Protocols Function

DeFi insurance protocols use smart contracts to automate insurance processes, protecting institutional investments from risks like smart contract vulnerabilities. By understanding how these systems operate, institutions can better manage the risks associated with decentralized finance.

Parametric Insurance and Automated Triggers

Parametric insurance leverages smart contracts to automatically process payouts when specific conditions are met. Unlike traditional insurance, this model eliminates the need for manual claim reviews or proof-of-loss submissions. Instead, payouts are triggered by objective data, such as a stablecoin dropping below $0.88 or a smart contract being drained of funds.

Decentralized oracle networks play a key role in supplying the data that activates these triggers. As Chainlink explains:

In parametric models, smart contracts automatically trigger payouts when specific data conditions are met, eliminating the need for manual review.

This automation reduces administrative overhead and ensures near-instant liquidity, which is essential for managing time-sensitive financial needs. These systems have proven reliable during significant DeFi incidents, highlighting their effectiveness.

Before committing to parametric coverage, institutions should carefully evaluate the oracle network a protocol relies on and review the specific conditions that trigger payouts. Since payouts are strictly tied to predefined data points, understanding these triggers is crucial.

Liquidity Pools and Risk Assessment

Liquidity pools are the financial backbone of DeFi insurance protocols. Instead of relying on centralized reserves, these pools use crowdsourced capital from liquidity providers, offering transparency and real-time solvency verification through on-chain data.

Premium costs are determined through risk assessment. One common approach uses the amount of capital staked against a project as a measure of its safety. Projects with higher staked amounts are seen as more secure, resulting in lower premiums. Risk assessors stake their own tokens on protocols they consider safe; if a hack occurs, their staked tokens are used to compensate victims, aligning incentives and ensuring accurate risk pricing.

A critical metric to monitor is the Minimum Capital Requirement (MCR), which defines the minimum funds a protocol must maintain to stay solvent. Falling below this threshold can halt the issuance of new policies. For example, Nexus Mutual – holding over 68% of the DeFi insurance market – initially set its MCR at 12,000 ETH in May 2019, later adjusting it to 7,000 ETH. Monitoring the MCR percentage is vital, as a level below 100% could indicate over-leverage and an inability to process claims.

Nexus Mutual calculates premiums using this formula: Risk Cost × (1 + Surplus Margin) × (Cover Period / 365.25) × Cover Amount, with a current surplus margin of 30%.

Smart Contract-Based Claim Settlements

DeFi insurance protocols employ two main settlement models: parametric settlements, which automatically trigger payouts based on oracle-verified data, and discretionary settlements, which require policyholders to submit claims reviewed and approved by token holder votes. Once approved, smart contracts release the appropriate funds from the liquidity pool.

For instance, in April 2022, Nexus Mutual processed claims amounting to 20 ETH and 5,008,000 DAI after the Rari Capital Fuse Market exploit caused by a reentrancy vulnerability. Automated settlements streamline the process, delivering payouts immediately or within the same day. As Chainlink explains:

The rules governing premium pricing, capital requirements, and claim payouts are hardcoded into smart contracts. This ensures execution strictly follows predefined logic.

For institutions, this means faster settlements and the ability to independently verify a protocol’s solvency without relying on periodic audits. However, because parametric insurance depends entirely on external data, it’s essential to use redundant and cross-verified oracle feeds to avoid inaccuracies or reliance on faulty data.

DeFi Insurance Providers for Institutions

To address the risks associated with smart contract vulnerabilities and safeguard institutional capital, several DeFi insurance providers have crafted specialized solutions. These platforms vary in their claims processes, coverage options, and pricing structures, offering institutions flexibility to match their unique risk profiles and operational requirements. By automating claims and refining coverage parameters, these solutions integrate seamlessly into institutional risk management strategies. Below, we explore how leading providers like Nexus Mutual, OpenCover, and InsurAce cater to institutional needs by combining smart contract automation with adaptable coverage options.

Nexus Mutual Smart Contract Cover

Nexus Mutual operates with a $100M capital pool and has protected over $6B in crypto assets since its launch in 2019. The platform has paid out more than $18.5M in claims, showcasing its ability to manage diverse smart contract risks.

The Fund Portfolio Cover is specifically designed for professional allocators, offering protection for yield-generating portfolios against risks such as smart contract vulnerabilities, governance attacks, custody failures, and depeg events. Coverage is tokenized as ERC-721 NFTs, allowing institutions to adjust coverage amounts, renew terms, and file partial claims without needing to replace the token. In 2025, Nexus Mutual generated $5.7M in cover fees and processed nearly $100,000 in claims related to the Stream Finance incident.

Premiums for Nexus Mutual’s Fund Portfolio Cover start at 0.12% annually for protocol coverage and 1.95% per year for custody coverage. Alessandro Buser, CTO of Dialectic, highlights its value:

The cost-efficient Fund Portfolio Cover from market-leader Nexus Mutual allows us to provide an even more asymmetric risk-return profile in our yield-generating funds. Nexus Mutual is the only company we trust to issue a cover that fits the complexities of our operations.

This product exemplifies how tailored coverage can enhance institutional confidence in navigating smart contract risks.

OpenCover Protocol Coverage

OpenCover simplifies on-chain insurance by automating claims through real-time data and oracle feeds. This automated process removes the need for manual claim reviews, ensuring payouts are triggered promptly when specific conditions – like protocol hacks or major economic events – are verified on-chain.

Premiums start at just $2 per week for $5,000 worth of coverage. In July 2025, OpenCover collaborated with Nexus Mutual to pay out over $250,000 to users affected by the Arcadia Finance protocol exploit. For institutions seeking multi-protocol protection, OpenCover offers strategies costing approximately 0.37% per month, providing flexible coverage across various DeFi positions. This approach highlights how parametric coverage can streamline institutional risk management processes.

InsurAce Institutional Policies

InsurAce offers extensive policies that address DeFi exploits, stablecoin depegging, and custody risks. Annual premiums for general DeFi insurance range from 2% to 10%, depending on the protocol’s risk profile and the duration of coverage. For institutions requiring more tailored solutions, InsurAce provides customizable policies through annex documents, enabling them to address unique risks, such as governance or oracle vulnerabilities, specific to their investment strategies. This level of customization allows institutions to align their insurance coverage with their overall risk mitigation frameworks effectively.

Using DeFi Insurance with BeyondOTC TVL Advisory

Evaluating Protocol Risks Before Investment

Before deploying institutional funds into DeFi protocols, BeyondOTC’s TVL advisory services focus on identifying and assessing risks tied to smart contracts. This involves a thorough risk assessment process that verifies independent code audits and incorporates real-time monitoring to detect vulnerabilities like reentrancy attacks, oracle manipulation, and flash loan exploits.

The advisory also evaluates the TVL-to-active-cover ratio, ensuring that insurers maintain solvency. For institutional clients, BeyondOTC goes further by vetting protocols for compliance with KYC/AML standards in permissioned pools and assessing the stability of decentralized governance systems. Given that insurance premiums typically range between 2% and 10% annually, these costs are factored into TVL deployment strategies to ensure attractive, risk-adjusted returns. These comprehensive evaluations feed directly into BeyondOTC’s integrated TVL and insurance strategies.

Pairing Insurance with BeyondOTC TVL Solutions

BeyondOTC combines its TVL advisory with DeFi insurance to create a comprehensive risk management framework. By addressing smart contract vulnerabilities, these solutions help mitigate systemic risks. While high yields can attract capital, effective insurance is key to safeguarding it during periods of market turbulence.

BeyondOTC’s advisory also points out that on-chain insurance markets can act as early warning systems. For instance, a sudden rise in premiums for a specific protocol might signal potential issues before an exploit occurs.

For additional protection, BeyondOTC integrates TVL solutions with insurance that secures principal capital. Their network and legal services assist clients in connecting with regulated, institutional-grade insurers like Chainproof or KYC-compliant mutuals such as Nexus Mutual, ensuring alignment with regulatory and compliance requirements.

Coverage Options Comparison

To aid in decision-making, BeyondOTC evaluates and compares leading DeFi insurance providers. Below is a summary of the key features offered by some of the top options:

| Provider | Model Type | Key Institutional Feature |

|---|---|---|

| Nexus Mutual | Discretionary mutual (KYC required) | Large capital pool (exceeding US$230M) with community-driven claims |

| OpenCover | Parametric, automated settlement | Real-time claim triggers leveraging on-chain oracles |

| InsurAce | Customizable institutional policies | Coverage options with premiums typically ranging from 2% to 10% annually |

When assessing these providers, institutions should carefully monitor the Minimum Capital Requirement (MCR). If a provider’s capital pool falls below its MCR, it may restrict the issuance of new policies. BeyondOTC supports clients by verifying solvency metrics on-chain and recommending diversification across multiple insurance providers to mitigate the risk of a single insurer’s failure.

Currently, DeFi insurance accounts for less than 1% of the total value locked in DeFi protocols. This presents an opportunity for early institutional adopters to establish robust risk management frameworks ahead of broader market adoption.

Additional Risk Management Strategies for DeFi

Third-Party Smart Contract Audits

Insurance can only go so far in mitigating smart contract risks. Independent security audits play a crucial role in identifying vulnerabilities before they can be exploited. Institutions should favor protocols that have undergone reviews by multiple trusted firms.

An effective audit process typically combines automated tools, manual code reviews, and simulated attacks to uncover potential issues in complex logic. However, even the most thoroughly audited protocols aren’t immune to hidden flaws. For instance, in November 2025, Balancer – a well-established DeFi protocol with a solid history of security audits – suffered a $110 million exploit due to misconfigured access controls. This was its third major breach since 2021. Similarly, in January 2026, Truebit faced a $26.4 million loss from a price calculation overflow bug in a contract deployed back in 2021. These incidents highlight that even older, seemingly stable code can lead to significant risks.

"If smart contracts are ever going to be reliably secure, development teams must embrace security as process-integrated throughout the development lifecycle." – John Mardlin, Security Engineer, Consensys Diligence

Institutions should ensure that audit recommendations are fully addressed, maintain ongoing bug bounty programs, and monitor platforms like GitHub for updates and fixes. Since no audit can guarantee complete safety, diversifying investments is another key strategy for reducing risks.

Spreading Capital Across Multiple Protocols

Diversification is a critical second layer of protection. No matter how reputable or well-audited a protocol may be, vulnerabilities can still arise. To minimize exposure, institutions should distribute their liquidity across multiple established protocols like Uniswap, Curve, and Orca, as well as across different blockchain ecosystems and asset types.

Position sizing is equally important. Allocating smaller amounts to individual protocols reduces the impact of potential losses. Institutions should also prioritize contracts with features like immutability or time-locked governance (e.g., 48-hour delays), which allow time to exit positions if a problematic update is introduced. Clear exit strategies are essential, enabling swift withdrawals in response to warning signs such as unusual on-chain activity or sudden premium increases.

Using BeyondOTC’s Network and Legal Services

To complement audits and diversification, institutions can turn to specialized legal and network services for additional security. Deploying capital in DeFi often involves navigating complex regulatory landscapes. BeyondOTC offers access to regulated insurers and legal experts specializing in blockchain law, ensuring adherence to KYC/AML standards and other jurisdictional requirements.

For institutions that prefer permissioned pools – where all participants meet compliance standards – BeyondOTC provides on-chain identity verification and whitelisting solutions. Their legal consultancy also helps clients navigate regulatory risks, such as potential SEC scrutiny over unregistered securities, which can have far-reaching effects on DeFi platforms. By combining technical evaluations with legal guidance, BeyondOTC supports "defense in depth" strategies that address both security and compliance concerns.

Conclusion

Main Points

The risks and safeguards in DeFi highlight how vulnerabilities have led to substantial losses. DeFi insurance, through automated parametric payouts, offers a mechanism to address these risks when specific conditions are met.

Institutions have the option to work with regulated insurers backed by traditional reinsurers. On the decentralized side, platforms like Nexus Mutual have already safeguarded over $6 billion in digital assets since their creation. However, insurance alone isn’t a cure-all. To effectively manage risks, institutions should also employ third-party audits, diversify their capital, and maintain continuous monitoring.

As discussed, effective DeFi insurance is most impactful when paired with proactive legal and technical strategies. BeyondOTC’s TVL advisory services help institutions assess protocol risks, integrate insurance into compliant investment strategies, and navigate the complexities of regulatory landscapes. By combining due diligence with legal and network services, institutions can establish a multi-layered defense against both security threats and compliance challenges.

Next Steps

To strengthen your risk management strategy, begin by evaluating your DeFi exposure and identifying protocols holding your institutional capital. Analyze the specific vulnerabilities tied to these protocols and explore coverage options from providers like Nexus Mutual, OpenCover, and InsurAce. Keep in mind that insurance must be active prior to an exploit – retroactive coverage isn’t an option.

For higher levels of protection, consider regulated insurers that offer tailored policies and real-time monitoring. Spread your capital and insurance coverage across multiple providers to reduce counterparty risk. Reach out to BeyondOTC to learn how their TVL advisory, legal consultation, and network services can help you manage risks effectively while staying compliant with institutional requirements.

FAQs

What does DeFi insurance cover?

Decentralized Finance (DeFi) insurance provides coverage against risks such as smart contract vulnerabilities, hacks, and exploits. This type of protection is particularly valuable for institutional investors, as it helps reduce potential losses stemming from security breaches in decentralized applications and protocols.

How do automated (parametric) DeFi insurance payouts work?

Automated DeFi insurance payouts, often referred to as parametric payouts, work by triggering payments based on predefined conditions rather than relying on traditional damage assessments. For instance, if a smart contract exploit occurs or a stablecoin loses its peg, the system automatically releases funds.

This process relies on smart contracts and oracles to constantly monitor relevant data points. When the set criteria are met, payouts are executed instantly. This approach ensures quicker responses, greater transparency, and streamlined risk management in the ever-evolving DeFi landscape.

How can institutions verify an insurer can pay claims?

When assessing an insurer’s ability to pay claims, institutions should look at both regulatory compliance and reputation. For instance, if an insurer is a regulated provider of cyber insurance for smart contracts, it signals financial stability and adherence to industry norms. Additionally, evaluating the insurer’s monitoring and alerting services can offer insights into their operational reliability and efforts to prevent losses proactively.