Investing in private companies before they go public can be done through two main methods: secondary markets and direct pre-IPO investments. Each has distinct pricing models, access requirements, and risk profiles.

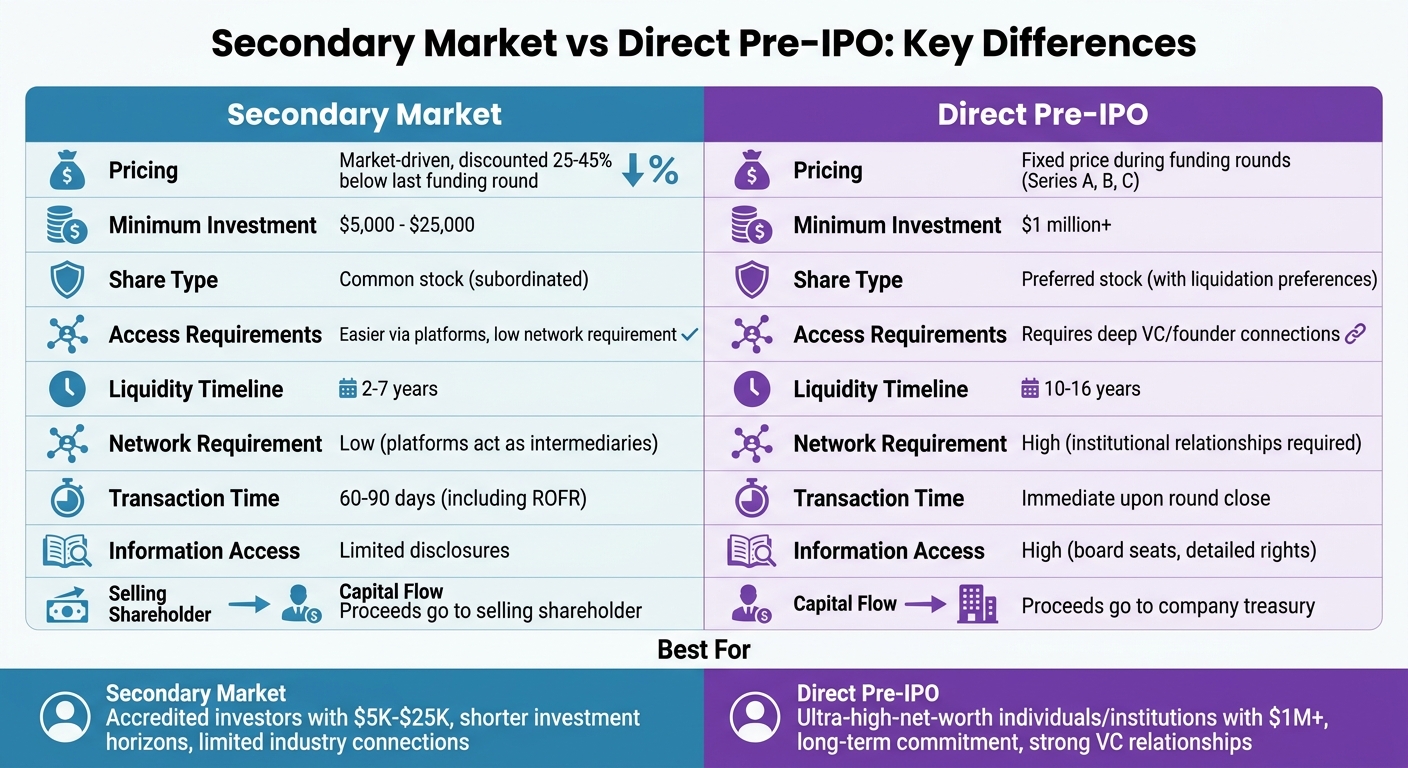

- Secondary Markets: Investors buy shares from existing shareholders (like employees or early investors). Pricing is market-driven and typically discounted 25%-45% below the last funding round. Minimum investments start as low as $5,000, making it more accessible, but shares are usually common stock with fewer protections.

- Direct Pre-IPO Investments: Investors purchase newly issued shares directly from the company during funding rounds (e.g., Series A, B, C). Pricing is set through negotiations with lead investors, often venture capital firms. These deals usually involve preferred stock with added rights, but access requires deep industry connections and minimum investments over $1 million.

Key Differences:

- Secondary markets offer lower entry points, shorter timelines (2–7 years), and easier access but involve common stock and potential transaction failures due to company restrictions.

- Direct pre-IPO deals provide preferred shares with better protections but require larger capital, stronger networks, and longer holding periods (10+ years).

Quick Comparison:

| Feature | Secondary Market | Direct Pre-IPO Investments |

|---|---|---|

| Pricing | Market-driven, discounted | Fixed price during funding |

| Minimum Investment | $5,000–$25,000 | $1 million+ |

| Share Type | Common stock | Preferred stock |

| Access | Easier via platforms | Requires connections |

| Liquidity Timeline | 2–7 years | 10+ years |

Your choice depends on your budget, timeline, and network. Secondary markets suit those with smaller capital and shorter horizons, while direct pre-IPO investments are better for high-net-worth individuals seeking early-stage exposure.

Secondary Market vs Direct Pre-IPO Investment Comparison Chart

Secondary Market: Pricing and Access

How Secondary Market Pricing Works

In the secondary market, prices are shaped by supply and demand rather than being set by the company. Early employees or founders looking to sell their shares negotiate directly with buyers who want pre-IPO exposure. This creates a market-driven price that often differs from the company’s most recent funding round.

Typically, secondary transactions involve common stock, which is sold at a discount compared to preferred stock. For instance, in Q1 2025, shares traded at a 20% discount to the latest funding round. Prices generally fall within two key benchmarks: the 409A valuation (the IRS-approved fair market value for common stock) and the preferred stock price from the most recent funding round. Founders often sell common shares for 70% to 100% of the preferred stock price. However, the lack of detailed financial disclosures for private companies often leads to an "illiquidity discount", as buyers face information gaps.

"The narrative has shifted recently because fundraising, dealmaking, and exit activity aren’t as robust as they were during the zero interest rate policy era. Now, the secondary market is a way for sellers to access much-needed liquidity."

– Emily Zheng, Senior Analyst, PitchBook

Another key aspect of secondary market transactions is the need for company approval. Most deals require the company’s consent and are subject to a Right of First Refusal (ROFR). This gives the company or its existing investors the right to match the negotiated price, potentially blocking external buyers. This approval process can take 30–60 days, meaning even after a price is agreed upon, the deal might still fall through.

These pricing and approval dynamics underline why stringent accreditation and documentation are essential for investors entering secondary markets.

Requirements for Secondary Market Access

To participate in secondary markets, investors must first meet strict accreditation requirements. Platforms verify accreditation through documentation such as tax returns, bank statements, or brokerage records. They also conduct Know Your Customer (KYC) and Anti-Money Laundering (AML) screenings.

| Accreditation Category | Individual Requirements | Verification Documents |

|---|---|---|

| Net Worth Test | $1 million+ (excluding primary residence) | Bank/brokerage statements, appraisals |

| Income Test | $200,000+ individually ($300,000 jointly) for the past two years | Tax returns (W-2, K-1, 1099) |

| Professional | Series 7, 65, or 82 license holders | FINRA verification |

Minimum investment amounts differ across platforms. For example, EquityZen requires investments between $10,000 and $25,000, typically through Special Purpose Vehicles (SPVs). On the other hand, Forge Global often sets minimums at $100,000 or more. Some newer platforms now allow fractional ownership, with investments starting as low as $1. Transaction fees generally range from 3% to 5%, with SPVs also charging annual management fees of 1% to 2% and carried interest of 10% to 20%.

Investors should complete all verification steps before exploring specific deals, as high-demand opportunities tend to close quickly. Even then, be prepared for a high rate of transaction failures due to company-level restrictions such as ROFR.

sbb-itb-7e716c2

Direct Pre-IPO: Pricing and Access

How Direct Pre-IPO Pricing Works

When you invest in a direct pre-IPO, you’re buying newly issued shares during a funding round – like Series A, B, or C. The money you invest goes straight to the company’s balance sheet, not to existing shareholders.

The pricing for these shares is worked out through negotiations between the company and lead institutional investors. Venture capital firms play a big role here, conducting in-depth due diligence and competing for allocations. Once terms are agreed upon, the price for preferred stock is set. Preferred shares often come with perks like liquidation preferences, anti-dilution clauses, and even board seats. Companies may price these shares using either a "Fixed Price" approach, where the price is predetermined, or a "Book Building" method, where a price range is set and investors place bids within it.

One key detail? The price gap between preferred and common stock can be huge. Take SpaceX as an example: its Series J preferred shares were priced at $110, while its 409A common stock valuation was just $45 – a 59% difference. Even secondary market transactions for SpaceX cleared at $85, which still represented a 23% discount compared to preferred shares. This difference, known as the "409A delta", highlights the structural advantages of preferred shares. They’re first in line to get paid during an exit, while common stockholders are further down the ladder.

"409A valuations systematically understate true common stock value because the methodology aims to withstand IRS scrutiny rather than reflect economic reality." – AltStreet

Here’s a hypothetical example to illustrate this: In a $400 million acquisition, if there’s a $170 million preference stack, common shareholders might only walk away with $1.84 per share, even though the headline valuation suggests $4.00 per share. That’s a 54% haircut. Modeling scenarios like this helps investors figure out the true value their shares might capture. Once pricing is clear, the next challenge is gaining access to these opportunities.

Requirements for Direct Pre-IPO Access

Direct pre-IPO deals aren’t for everyone – they come with strict requirements. To start, investors must meet SEC accreditation standards, with minimum investments typically set at over $1 million.

But money alone isn’t enough. Gaining access often hinges on having the right connections. Lead investors in these rounds are usually top-tier venture capital firms with established reputations. For individual investors, being a well-connected angel investor or part of a family office with ties to the company or its board is often the only way in.

There are also added costs to consider. Direct purchases can come with legal and administrative fees ranging from $25,000 to $30,000. However, these investments do offer some perks, like direct inclusion on the company’s cap table, bypassing Right of First Refusal (ROFR) constraints, and enhanced access to company information.

Finally, these investments require patience. Primary investors often face a timeline of 10 years or more before seeing a liquidity event, compared to the 2–7 years typical for secondary market participants. And there’s always risk. For example, Stripe’s valuation dropped from $95 billion in 2021 to $50 billion by 2023. Investors who bought in at the peak price saw a 47% unrealized loss. Long-term commitment is key, but so is timing your entry point wisely.

Pre-IPO Investing: Risks, Rewards, and Strategy

Pricing Comparison: Secondary Market vs Direct Pre-IPO

When companies raise funds through direct pre-IPO rounds, the pricing is predetermined. This happens during structured funding stages, like Series B or C, where the company and its lead investors agree on a fixed issue price. This method contrasts sharply with the secondary market, where prices shift based on market conditions.

In the secondary market, pricing is entirely driven by supply and demand. Shareholders negotiate directly with buyers, and the price reflects the current market appetite. Typically, private shares trade at a discount of 25%–45% below the last preferred round price. These discounts vary depending on how close the company is to an IPO. For example, late-stage companies within a year of going public may see discounts narrow to 12%–18%. On the other hand, mid-stage companies, often five years away from an IPO, might face steeper discounts between 50% and 65%.

"Secondary transactions provide valuable market-based price indications, offering more transparency on a company’s worth between primary funding rounds." – EquityZen

Direct pre-IPO pricing reflects the company’s valuation at the time of the funding round. While this valuation is clear during the deal, it may not align with current market realities. In contrast, prices in the secondary market – although somewhat opaque due to variability – offer a real-time snapshot of investor sentiment and willingness to pay. Factors like higher required returns in early 2026 further influence these discounts, especially for companies at earlier stages.

Another key difference lies in the minimum investment requirements. Direct pre-IPO deals often demand commitments exceeding $1 million, restricting participation to institutional investors and ultra-high-net-worth individuals. Secondary markets, however, have significantly lowered this barrier. Some platforms allow accredited investors to participate with as little as $5,000. These differences in pricing and access shape investment strategies and risk profiles for participants.

Here’s a quick breakdown of the pricing dynamics in each market:

| Feature | Direct Pre-IPO (Primary) | Secondary Market |

|---|---|---|

| Price Determination | Fixed issue price set by the company and lead investors | Determined by ongoing bid/ask negotiations |

| Valuation Basis | Last preferred funding round or 409A valuation | Discounted 25%–45% relative to the last round |

| Transparency | High at the time of the round; becomes stale between rounds | Reflective of real-time market sentiment, but less transparent |

| Minimum Investment | Generally over $1M | Significantly lower thresholds |

| Share Class | Preferred stock with liquidation preferences | Usually common stock (subordinated) |

| Capital Flow | Proceeds go to the company treasury | Proceeds go to the selling shareholder |

Next, we’ll explore how access requirements differ between these two markets.

Access Comparison: Secondary Market vs Direct Pre-IPO

Gaining direct access to pre-IPO investments is no small feat – it hinges on having strong industry connections. These opportunities are typically reserved for institutional investors, venture capital firms, and a select group of well-connected individuals within the startup ecosystem. For most accredited investors, unless they have direct ties to company founders or lead investors, it’s nearly impossible to secure a spot in these highly competitive funding rounds.

On the other hand, secondary markets simplify access by acting as intermediaries between existing shareholders and potential buyers. This setup allows accredited investors to purchase shares in late-stage companies without needing insider connections in Silicon Valley. As of June 2025, only 12.6% of Americans qualified as accredited investors – defined by an annual income of $200,000 ($300,000 for joint filers) or a net worth of over $1 million, excluding their primary residence. Within this group, secondary platforms have expanded opportunities, though the liquidity timelines for these investments differ significantly from those in direct pre-IPO deals.

Liquidity timelines are a major differentiator. Direct pre-IPO investments often require a long-term commitment, ranging from 10 to 16 years, as companies remain private for extended periods. In contrast, secondary market investments focus on later-stage companies, typically Series C or beyond, which shortens the expected holding period to around 2 to 7 years. However, secondary transactions aren’t instantaneous – they involve a 60–90-day process for due diligence and Right of First Refusal (ROFR) procedures.

Another key distinction lies in the network requirements. Direct primary investments demand extensive industry relationships, particularly with venture capitalists and founders. Secondary platforms, however, remove much of this barrier by handling the intermediation themselves. The appeal of this accessibility is evident – during the first half of 2025, the private equity secondary market saw transaction volumes exceed $100 billion, marking a 42% increase from the previous year.

Here’s a quick breakdown of how the two options compare:

| Factor | Direct Pre-IPO (Primary) | Secondary Market |

|---|---|---|

| Network Requirement | High – requires deep VC/founder relationships | Low – platforms act as intermediaries |

| Accreditation | Required (institutional/ultra-high-net-worth) | Required (accredited investors) |

| Minimum Investment | Typically over $1M | Ranges from $5,000–$25,000 |

| Liquidity Timeline | Long-term (10–16 years) | Shorter (2–7 years) |

| Time to Completion | Immediate upon round close | 60–90 days (including ROFR) |

| Information Access | High (board seats, detailed rights) | Limited (minimal disclosures) |

This comparison highlights the trade-offs between the exclusivity and long-term nature of direct pre-IPO investments and the broader accessibility and shorter timelines offered by secondary markets. Each path comes with its own set of considerations, depending on the investor’s goals and resources.

Risks, Rewards, and How to Choose

When deciding between direct pre-IPO investments and secondary market opportunities, it’s crucial to weigh the risks and rewards of each approach to see which aligns with your investment strategy.

Each path carries its own set of risks. Direct pre-IPO investments are tied to early-stage companies, which often face a high risk of failure. While the potential returns can be substantial – especially when investing from Series A or B onward – you’re locking up your capital for over a decade, with limited liquidity options and no guarantee the company will survive or eventually go public.

On the other hand, secondary market investments focus on later-stage companies with more established business models, but they come with unique challenges. One major issue is information asymmetry: sellers, such as employees or early investors, might have insights into internal problems – like unfavorable liquidation preferences or imminent IPO filings – that you don’t. Additionally, the Right of First Refusal (ROFR) can disrupt transactions, even after you’ve completed extensive due diligence. Another drawback is that secondary market purchases often involve common stock, which places you lower in the liquidation hierarchy. In cases of modest exits, preferred shareholders may claim most of the proceeds, leaving little for common stockholders.

The potential rewards also differ. For secondary market investors in late-stage companies, median returns have been reported at +35% over three years (with a 10% IRR), while top performers achieved returns of +150% (35% IRR). A striking example is SpaceX: secondary shares purchased in 2019 at a $46 billion valuation reportedly grew to an estimated $180 billion by 2024, resulting in a +291% paper gain. However, the risks are evident in cases like WeWork, where investors who bought in at a $47 billion valuation in 2019 saw the company’s value plummet to $2.9 billion by 2020, representing a staggering -94% loss. Direct pre-IPO investments, while riskier due to earlier-stage involvement, can offer even greater rewards if the company succeeds.

Your choice between these strategies depends on factors like available capital, connections, and your investment timeline. If you have over $1 million to invest, strong industry ties, and a willingness to commit for 10+ years, direct pre-IPO rounds may appeal to you. These investments often include preferred shares with protective rights. Conversely, if your investment range is between $5,000 and $25,000, you lack direct VC relationships, and you prefer a shorter 2–7 year timeline with clearer liquidity options, secondary markets might be a better fit. It’s important to model exit scenarios and consider how factors like liquidation preferences, ROFR history, and taxes (20–35%) could impact your returns.

This is where BeyondOTC comes into play. BeyondOTC simplifies access to both markets by connecting accredited investors with curated opportunities in secondary markets and direct pre-IPO allocations. The platform handles due diligence, navigates ROFR complications, and provides escrow services during the 6–8 week settlement process. Whether your goal is early-stage exposure or late-stage liquidity, BeyondOTC’s network helps remove barriers and streamlines the entire transaction process from start to finish.

Conclusion

Deciding between secondary market opportunities and direct pre-IPO investments comes down to understanding how their pricing and access requirements align with your financial goals and circumstances.

Pricing structures differ greatly between the two options. In direct pre-IPO rounds, institutional lead investors set the price during funding rounds, offering preferred shares with added protective rights. On the other hand, secondary market prices are negotiated between buyers and existing shareholders, often involving common stock, which ranks lower in the liquidation hierarchy and may trade at a discount compared to the latest funding round. Additionally, secondary purchases through SPVs often come with extra fees that can impact your net returns.

Access requirements also contrast sharply. Direct pre-IPO investments usually demand a commitment of over $1 million and lock your capital for 10 or more years. Meanwhile, secondary markets offer a more accessible entry point, with minimum investments ranging from $5,000 to $25,000 and liquidity timelines typically between 2 and 7 years. While both options require accredited investor status, direct investments often necessitate strong industry connections, extensive due diligence, and significant administrative work. In contrast, secondary markets simplify the process through digital platforms that pool investor capital and handle operational details.

Ultimately, your choice should align with your available resources, risk appetite, and investment horizon. If you’re looking for early-stage exposure with voting rights and are ready to commit a substantial amount of capital for a decade or more, direct pre-IPO investments might be the way to go. However, if you’d prefer lower minimums, later-stage companies with proven business models, and a shorter liquidity timeline, secondary markets could be a more practical fit.

Platforms like BeyondOTC simplify these processes by managing due diligence and ROFR challenges, as discussed earlier. They connect accredited investors with tailored opportunities in both markets, helping you make well-informed investment decisions that suit your financial objectives.

FAQs

How do I estimate what common shares are really worth after liquidation preferences?

When evaluating the value of common shares after accounting for liquidation preferences, it’s important to consider the typical discounts seen in secondary markets. These discounts often range between 25% and 45% below the valuation of the last funding round. Additionally, liquidation preferences – designed to prioritize payouts to specific shareholders – can significantly reduce the remaining value available to common shareholders. Understanding these factors is key to gauging the realistic value of your shares in such situations.

What can cause a secondary deal to fail even after I agree on a price?

A secondary deal might fall through even after the price is agreed upon because of legal, regulatory, or due diligence problems. Typical issues include incomplete rights of first refusal (ROFR) procedures, mismatches in valuation, or unresolved legal disputes. These challenges can derail the transaction before it reaches completion.

What fees and taxes should I factor in before buying pre-IPO shares?

Before buying pre-IPO shares, it’s important to think about the potential tax implications. Federal and state income taxes can significantly affect your net proceeds, particularly with some tax provisions set to expire in 2026. Additionally, don’t overlook fees tied to secondary market transactions or platform usage. These costs can differ widely, so getting a clear picture of them in advance is crucial for effective financial planning.