If you’re issuing stock options, you need a 409A valuation to determine the fair market value (FMV) of your company’s common stock. This valuation ensures compliance with tax laws, sets the strike price for options, and protects your company from IRS penalties. For companies planning an IPO, accurate valuations are even more critical, as the SEC scrutinizes stock grants issued 12-18 months before the IPO to prevent "cheap stock" issues.

Here’s what you need to know:

- What is a 409A valuation? It’s an independent appraisal required under IRS rules to set a defensible FMV for stock options.

- Why is it important? Incorrect valuations can lead to tax penalties, regulatory issues, and delays in your IPO.

- Methods used: Early-stage companies often use the Option Pricing Method (OPM), while late-stage businesses nearing IPOs rely on the Probability-Weighted Expected Return Method (PWERM) or hybrids.

- Costs: Fees range from $2,000 for startups to $25,000+ for pre-IPO companies, depending on complexity.

- How to prepare: Gather financial records, cap tables, and projections, and work with qualified, independent appraisers.

Accurate valuations protect employees, satisfy regulators, and align your stock’s FMV with your IPO price. Investing in the right valuation process now can save you from costly mistakes later.

What Are 409A Valuations?

Definition and Purpose

A 409A valuation is an independent assessment used to determine the fair market value (FMV) of a private company’s common stock. This valuation is a legal requirement under IRC Section 409A and plays a key role in how companies compensate employees, advisors, and contractors through stock options.

The main purpose of the valuation is to establish a defensible strike price for stock options. For stock options to comply with the law, their exercise price must be set at or above the FMV of the company’s common stock on the grant date. Failing to get this right can lead to significant tax consequences for those holding the options.

By relying on a qualified independent appraiser – such as a CPA or an accredited valuation professional – the company gains protection. The IRS then carries the burden of proving that the valuation is "grossly unreasonable" if challenged. This offers a layer of safe harbor protection.

Since common stock lacks the protections and privileges of preferred shares, it typically trades at a 60% to 80% discount compared to preferred stock. These discounts reflect the absence of features like liquidation preferences, voting rights, and the ability to easily sell shares in private companies.

Grasping these basics is essential before diving into the compliance requirements outlined under IRC Section 409A.

IRC Section 409A Compliance Requirements

IRC Section 409A, introduced in 2004 after corporate accounting scandals, regulates nonqualified deferred compensation, including stock options. The law mandates that stock option exercise prices must match or exceed the FMV of the underlying common stock on the grant date.

Certain material events can invalidate an existing valuation, requiring an immediate update. This is especially critical for companies approaching an IPO. Examples of such events include closing a priced equity round, reaching major revenue milestones, launching significant products, or undergoing mergers and acquisitions. Recent IRS guidance has expanded this list to include events like substantial customer wins or losses, major contract signings, or significant operational changes. If any of these occur, refreshing the valuation is non-negotiable.

Non-compliance comes with harsh penalties for option holders. Employees could face a 20% federal penalty tax on the difference between the FMV and the strike price, in addition to ordinary income tax and interest. In California, an extra 5% state penalty tax applies. Combined, these taxes can exceed 45% of the discount value. Furthermore, stock options initially structured as Incentive Stock Options (ISOs) may be reclassified as Non-Qualified Stock Options (NSOs), stripping away their long-term capital gains benefits.

To avoid these risks, over 90% of US startups rely on the safe harbor method to guard against IRS audits. For this method to hold up, appraisers must have at least five years of relevant experience. Additionally, the company’s Board of Directors must formally review and approve the 409A valuation through a board resolution, ensuring its legal defensibility.

sbb-itb-7e716c2

What’s a 409A valuation, and why does it matter?

Valuation Methods for 409A and Pre-IPO Pricing

409A Valuation Methods Comparison by Company Stage

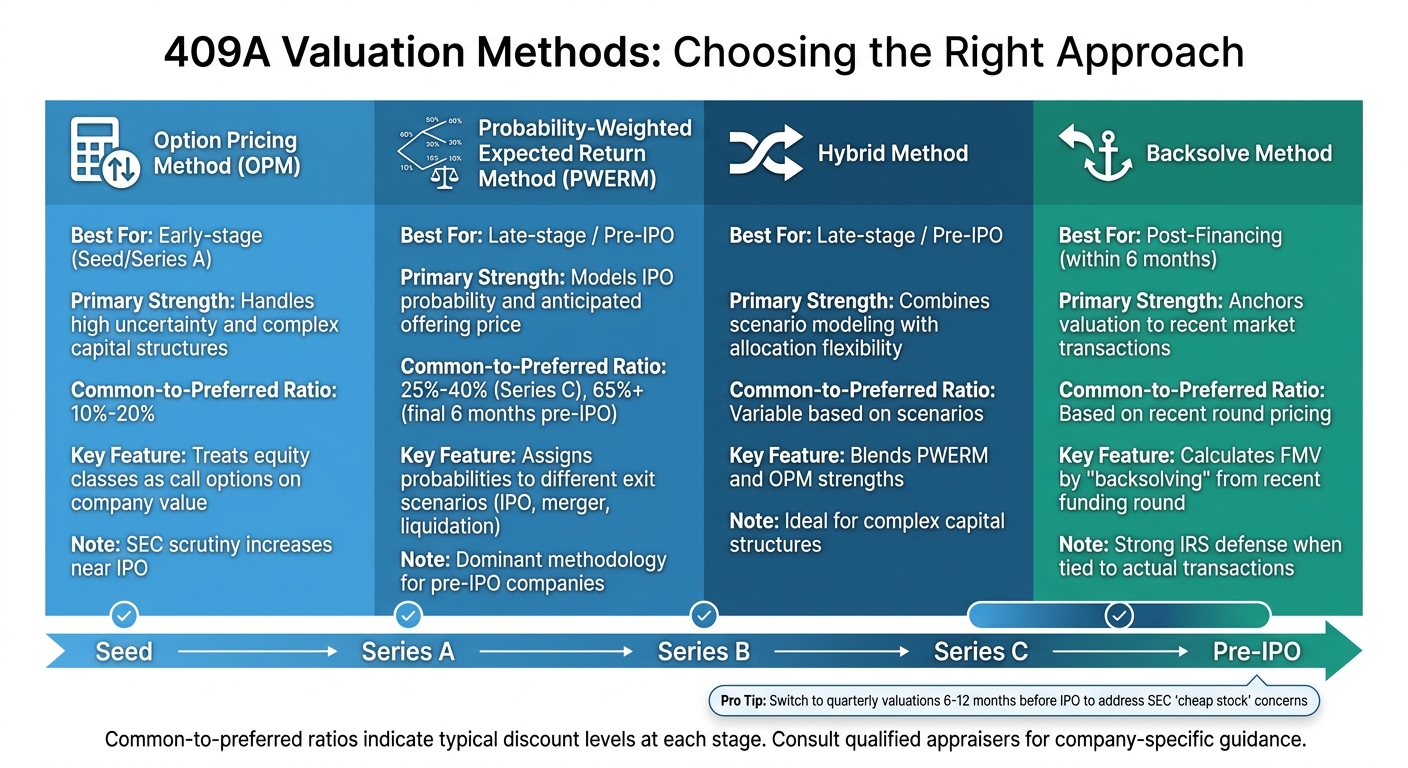

Getting a valuation right is a big deal when setting strike prices and staying compliant with regulations as your company gears up for an IPO. The method you choose depends on where your company stands in its journey and how clear the exit path is. Each approach handles uncertainty differently and is tailored to specific stages of growth.

Option Pricing Method (OPM) treats each equity class like a call option on the company’s total value. This method works best for early-stage startups, usually those in the Seed or Series A phase, when the future is still pretty unpredictable. At this point, common stock often trades at just 10% to 20% of the price of preferred shares. But keep in mind, as your company gets closer to an IPO, the SEC may take a closer look at OPM usage.

Probability-Weighted Expected Return Method (PWERM) assigns probabilities to different future scenarios – like an IPO, merger, or even liquidation. This method shines for companies nearing an IPO because it can directly factor in the expected offering price. According to 409A-Valuation.com:

"The PWERM is the dominant methodology for pre-IPO companies precisely because it can incorporate IPO probability and anticipated offering price as explicit inputs."

This ability to model specific outcomes makes PWERM a go-to for late-stage companies. By Series C, the common-to-preferred share ratio often climbs to 25%-40%, and in the final six months before an IPO, it can jump to 65% or even higher as liquidity becomes more predictable.

Hybrid Method blends the strengths of PWERM and OPM. It models specific exit scenarios while also accounting for uncertainty, making it a great choice for late-stage companies with complex capital structures. By combining OPM’s flexibility with PWERM’s scenario-based modeling, it offers a balanced and regulator-friendly approach. On the other hand, the Backsolve Method uses recent financing data to anchor valuations.

Backsolve Method calculates the fair market value of common stock by “backsolving” from the price paid by investors in a recent funding round. It’s particularly useful within six months of a priced round, as it ties the valuation to actual market transactions, providing a strong defense against IRS scrutiny.

Here’s a quick breakdown of when each method works best and what it brings to the table:

| Method | Best Company Stage | Primary Strength |

|---|---|---|

| OPM | Early-stage (Seed/Series A) | Handles high uncertainty and complex capital structures |

| PWERM | Late-stage / Pre-IPO | Models IPO probability and anticipated offering price |

| Hybrid | Late-stage / Pre-IPO | Combines scenario modeling with allocation flexibility |

| Backsolve | Post-Financing (within 6 months) | Anchors valuation to recent market transactions |

For companies planning an IPO within 6 to 12 months, it’s smart to switch to more frequent valuations – quarterly or even per-grant. This can help address SEC concerns about "cheap stock", as the SEC closely monitors valuation trends in the 12 to 18 months leading up to an IPO filing.

Factors That Affect Pre-IPO Pricing

Pre-IPO pricing is influenced by a mix of external market dynamics and a company’s internal performance. Together, these elements shape the perceived value of your shares. Grasping these factors can help you better predict how your valuation might shift as you move closer to an IPO.

Market conditions play a foundational role in setting valuation baselines. Public market comparables are key here, especially with early 2026’s risk-free rate hovering around 4.5%. This higher rate pushes investors to seek larger returns on less liquid private shares, leading to increased stock discounts. Volatile public markets can further widen the Discount for Lack of Marketability (DLOM), as buyers demand greater protection against potential market downturns before the IPO. These external forces establish the environment in which internal company performance impacts valuation.

Financial performance is one of the most direct factors you can control. Revenue growth is a major driver of enterprise value, particularly in high-growth industries like SaaS, where forward ARR multiples are often used to assess worth. As your company approaches profitability, reduced uncertainty tends to lift your fair market value. This alignment is crucial for avoiding regulatory scrutiny. Additionally, investor interest plays a role in narrowing the gap between private valuations and the expected IPO price.

Investor demand adds a liquidity premium that helps bridge private valuations and IPO pricing. Feedback from investment bankers and underwriters offers valuable, market-backed insights into your enterprise value. As institutional interest grows and an IPO becomes imminent, the fair market value (FMV) of common stock begins aligning more closely with the anticipated IPO price. One expert appraisal explains:

"As the IPO probability approaches 100% and the price range becomes defined through underwriter conversations, the common stock FMV in the 409A should approach – but not necessarily equal – the anticipated IPO price."

In 2026, a clear "flight to quality" trend has emerged. Companies with a well-defined 18-month path to liquidity and strong revenue – typically in the $100M to $200M ARR range – tend to command a premium over peers with less certain exit strategies. On the secondary market, businesses nearing an IPO often trade at 1.5x to 2.0x their 409A valuation, while others average closer to 1.0x to 1.2x. Over time, the gap between private valuations and the expected IPO price narrows significantly – from about 40%-65% at 18 months out to 65%-90% or more in the final six months.

409A Valuation Costs by Company Stage

Planning for 409A valuation costs is crucial for accurate budgeting. As your business grows, these fees tend to rise, influenced by factors like company stage, revenue, and the complexity of your cap table. Early-stage startups with simpler operations usually face much lower costs compared to later-stage companies approaching an IPO.

Valuations need to be updated annually or when significant events occur, such as funding rounds or major revenue changes. Understanding this cost structure can help you choose the right valuation provider and adjust the frequency of valuations as your company evolves.

Cost Breakdown by Stage

The cost of a 409A valuation depends heavily on where your company is in its lifecycle. For instance, pre-seed companies with limited financial history and straightforward cap tables generally spend between $2,000 and $5,000. At this stage, valuation firms often use simpler methods like asset-based approaches or basic Option Pricing Method (OPM) calculations, which require less effort.

For Series A companies, fees typically range from $4,000 to $6,000. By the time a company reaches Series B, costs increase to $6,000–$8,000, reflecting added complexity like multiple share classes, liquidation preferences, and instruments such as convertible notes or SAFEs.

| Company Stage | Revenue / Funding | Typical Cost Range |

|---|---|---|

| Pre-seed / Seed | $0 – $2M ARR | $2,000 – $5,000 |

| Series A | $2M – $10M ARR | $4,000 – $6,000 |

| Series B | $10M – $50M ARR | $6,000 – $8,000 |

| Series C+ | $50M+ ARR | $8,000 – $12,000 |

| Pre-IPO | N/A | $15,000 – $25,000+ |

For pre-IPO companies, costs reach their peak. As these businesses prepare for an IPO, valuation complexity grows, often requiring the expertise of Big 4 accounting firms to ensure audit defensibility. Fees at this stage typically range from $15,000 to over $50,000, especially in highly complex scenarios. These firms employ a mix of income, market, and asset-based valuation methods to meet stringent audit standards.

"While it used to be that these 409As are extremely expensive and complicated, there are cap table providers and firms now that have simpler and much more affordable solutions."

- Jason Atkins, Co-Founder of Cake Equity

Additionally, keeping financial records clean and maintaining an organized cap table can reduce costs by $500 to $2,000. Annual valuation updates usually cost 30%–60% less than the initial valuation, and proactive planning can help you avoid rush fees, which can add 25%–50% to the base cost.

How to Obtain a 409A Valuation

Once you’ve explored valuation methods and regulatory guidelines, the next step is obtaining a 409A valuation. This process typically unfolds in four stages – Discovery, Research & Analysis, Diligence, and Delivery – to meet IRS safe harbor standards. Below, we’ll walk through how to prepare the necessary documentation and choose the right provider to make the process smoother.

Preparing for a 409A Valuation

Start by gathering all your financial and legal documents before contacting a valuation provider. Having your records in order can save time and prevent unnecessary delays. Ideally, begin this process 2–3 months before issuing stock options or before your existing 12-month safe harbor period expires.

Here’s a checklist of essential documents you’ll need:

- Business formation documents, including your certificate of incorporation and any amendments.

- A fully diluted cap table showing all equity instruments – common stock, preferred shares, options, warrants, SAFEs, and convertible notes.

- Historical financial statements covering the past 2–3 years, along with current year-to-date figures.

- Board-approved financial projections for the next 3–5 years.

- Information on recent funding rounds, secondary sales, or term sheets from the last 12–18 months.

- Your business plan, investor pitch deck, and any prior 409A valuation reports.

"Maintaining accurate financial statements and having strong financial controls gives valuation providers a clearer view of the company’s development and forecasted growth." – Steve Liu, Executive Director and Head of Valuation Services, Morgan Stanley at Work

Accuracy is key. Make sure to review company descriptions, share counts, and financial metrics during the draft phase to catch any errors early. Once the valuation is finalized, your board must formally approve the fair market value to use it for setting stock option exercise prices.

Selecting a Valuation Provider

Choosing the right valuation provider is critical for maintaining safe harbor status. The provider must be independent and have no financial ties to your company. Avoid relying on internal staff like your CFO, founders, or investors, as this could compromise safe harbor protection.

Look for professionals with certifications such as Accredited Senior Appraiser (ASA), Certified Valuation Analyst (CVA), Accredited in Business Valuation (ABV), or Chartered Financial Analyst (CFA). Ensure the appraiser has at least five years of experience, particularly with companies at your stage and in your industry. For instance, life sciences companies may need specialized methodologies like the Probability-Weighted Expected Return Method (PWERM).

If your company is approaching an IPO, your provider should be capable of defending the valuation under SEC and auditor scrutiny, especially regarding ASC 718 compliance. It’s also a good idea to consult your financial statement auditor for referrals to ensure the chosen provider’s methods align with audit requirements.

Here’s how to match a provider to your company’s stage:

- Software-led providers: Ideal for early-stage startups (pre-seed to Series A), offering quick turnarounds (1–2 weeks) and lower costs, typically $1,500–$2,500.

- Traditional boutique firms: Suited for mid-stage companies that need more detailed analysis or industry-specific expertise. Costs usually start at around $5,000.

- Big 4 or large accounting firms: Best for late-stage or pre-IPO companies due to their audit credibility. However, these providers are more expensive (often $15,000+) and take longer (4–8 weeks).

Before committing, request sample reports to evaluate the provider’s communication style. The reports should be clear and straightforward, avoiding unnecessary jargon. Be cautious of "opinion shopping" – seeking multiple valuations to find the lowest price – as this can raise IRS red flags and jeopardize safe harbor protection.

Conclusion

Accurate 409A valuations play a crucial role in protecting employees, maintaining investor trust, and ensuring a smoother path to a successful IPO. The stakes are high – failing to meet valuation standards can result in severe tax penalties and SEC scrutiny over potential "cheap stock" issues, which could derail your IPO timeline entirely.

As your company grows, it’s important to adapt your valuation methods. While early-stage companies might rely on annual Option Pricing Method valuations, transitioning to quarterly or per-grant PWERM assessments as you approach an IPO ensures a more consistent alignment with your offering price. Keep in mind that the SEC typically reviews option grants issued 3 to 5 years before an IPO, making a defensible and consistent valuation history essential.

Investing in a reliable valuation process is a smart move to reduce future risks. While a pre-IPO valuation from a Big 4 firm might cost $15,000 or more, this expense is minor compared to the potential financial and regulatory consequences of valuation errors. Choosing qualified, independent appraisers also provides safe harbor protection, shifting the burden of proof to the IRS in case of disputes.

To stay on track, work with experienced valuation professionals and involve your auditors early in the process. Keep detailed records of business milestones and the assumptions underlying your valuations. By investing in accurate and defensible valuations now, you’ll protect your team, build stronger relationships with investors, and set the stage for a successful IPO.

FAQs

How often should we refresh our 409A as we get close to an IPO?

As your IPO draws near, it’s a good idea to update your 409A valuation at least every six months or whenever significant events occur. This helps ensure compliance and provides an accurate reflection of your fair market value, especially since the pre-IPO stage often comes with increased scrutiny and fluctuating valuations.

What does the SEC consider “cheap stock,” and how can we avoid it?

The SEC describes “cheap stock” as shares issued or granted at exercise prices much lower than the public offering price shortly before an IPO. This situation can create issues around compliance and valuation. To steer clear of these problems, it’s important to ensure stock valuations are thoroughly documented, match the exercise price, and are supported by a clear rationale at the time of issuance.

Which valuation method should we use if an IPO isn’t certain yet?

If an IPO isn’t guaranteed, it’s smart to pick a valuation method that doesn’t hinge entirely on future public market value. Here are some common 409A valuation approaches:

- Market approach: Looks at comparable companies or transactions to gauge value.

- Income approach: Estimates projected cash flows, though it can be less dependable if earnings are uncertain.

- Asset approach: Centers on net asset value, making it a better fit for businesses with significant physical assets.

Qualified appraisers often blend these methods to ensure both accuracy and regulatory compliance.