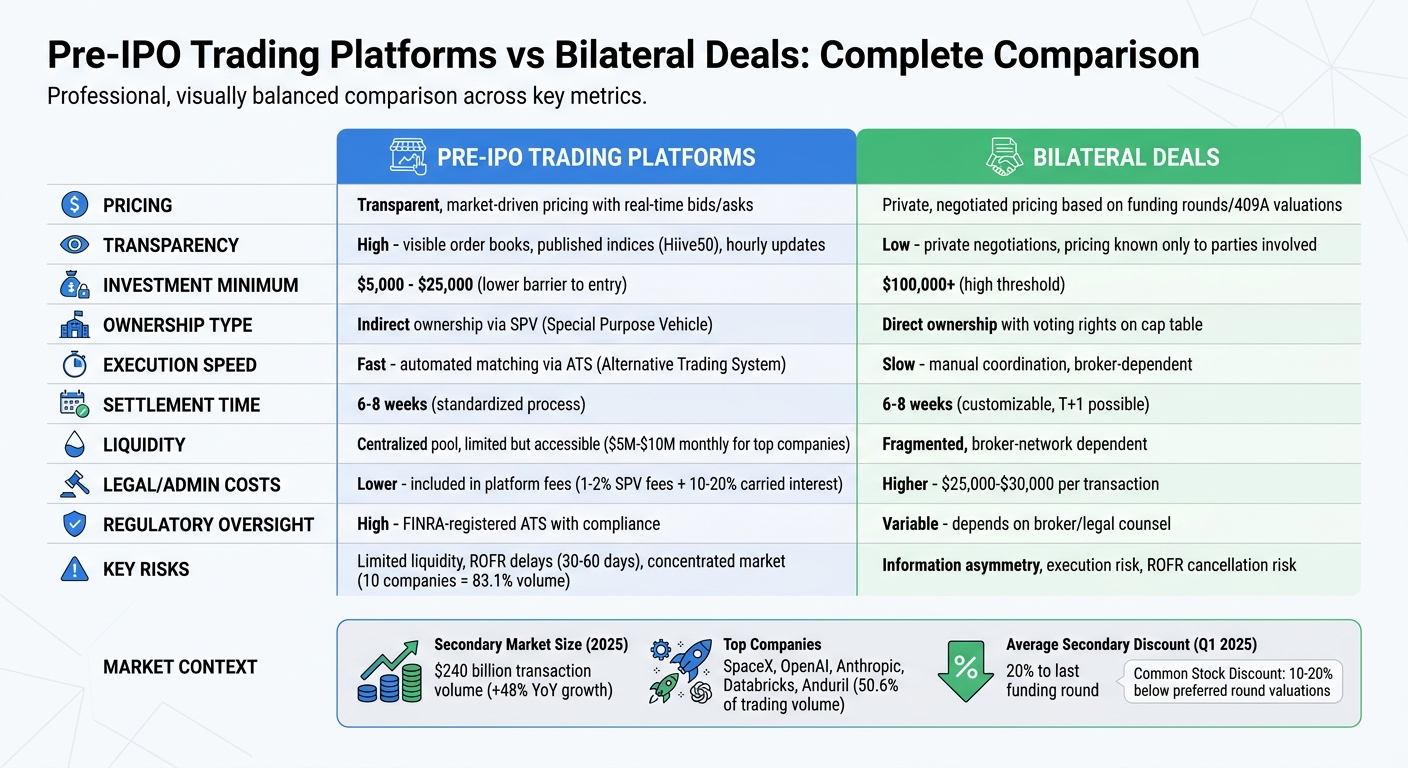

When trading pre-IPO shares, you have two main options: pre-IPO trading platforms or bilateral deals. Both methods allow access to private company shares but differ in pricing, transparency, and liquidity. Here’s a quick breakdown:

- Pre-IPO Platforms: These are digital marketplaces offering real-time pricing, lower investment minimums ($10,000–$25,000), and automated processes. However, liquidity is limited, with top companies like SpaceX and OpenAI dominating trading volumes. Pricing can vary widely between platforms due to different calculation methods and fees.

- Bilateral Deals: These are private, negotiated transactions often facilitated by brokers. They offer direct ownership but require higher investments (typically $100,000+) and come with higher legal costs. Pricing is less transparent and depends on negotiation, often influenced by factors like urgency or share type (common or preferred).

Both methods face challenges like Right of First Refusal (ROFR), long settlement timelines (6–8 weeks), and valuation uncertainties. While platforms provide easier access for smaller investors, bilateral deals cater to larger, private transactions.

Quick Comparison

| Feature | Pre-IPO Platforms | Bilateral Deals |

|---|---|---|

| Pricing | Transparent, market-driven | Private, negotiated |

| Liquidity | Limited but centralized | Fragmented, broker-dependent |

| Investment Minimum | $10,000–$25,000 | $100,000+ |

| Ownership | Indirect (via SPV) | Direct |

| Execution Speed | Faster, automated | Slower, manual coordination |

| Settlement | 6–8 weeks | 6–8 weeks |

Which approach suits you depends on your investment size, need for transparency, and preference for ownership rights.

Pre-IPO Trading Platforms vs Bilateral Deals: Complete Comparison Guide

Episode 1191: The Insider’s Guide to Pre-IPO Trading

sbb-itb-7e716c2

Pre-IPO Trading Platforms: Pricing and Liquidity

Pre-IPO trading platforms serve as digital hubs for buying and selling shares of private companies. But pricing and liquidity on these platforms come with unique challenges. Unlike the centralized pricing seen on public exchanges, pre-IPO platforms often deal with fragmented pricing. Take Cerebras Systems on February 17, 2025, as an example: Forge listed shares at $36.72, EquityZen showed a range of $39.00 to $57.00, Hiive reported an average of $39.16, Notice.co quoted $30.45, and Augment displayed institutional bids between $13.00 and $34.00.

How Pricing Works on Pre-IPO Trading Platforms

Pricing on these platforms varies widely, depending on their methods. Some rely on live order books, while others use proprietary calculations or preset markups. For instance:

- Hiive and Augment: Use live order books, allowing real-time bids and asks similar to public exchanges.

- Forge: Employs its "Forge Price", an indicative daily value derived from secondary trades, funding events, and interest levels.

- Linqto: Pre-purchases shares and resells them at fixed prices, adding a markup.

"Trend lines are determined by calculating a weighted average of accepted bids, bids, and listings at a point in time, with the highest weight on accepted bids, followed by bids, and then listings." – Hiive

Other factors also influence pricing, including premiums for specific share classes, discounts for large block sizes (ranging from 5% to 30%), and additional fees like SPV charges (1–2% annually plus 10–20% carried interest). These pricing models directly impact how liquid pre-IPO shares can be.

Liquidity Availability on Pre-IPO Trading Platforms

Liquidity on pre-IPO platforms is far more limited than in public markets. For high-demand companies, monthly trading volumes typically range between $5 million and $10 million – nowhere near the billions traded daily in public exchanges. Moreover, this market is heavily concentrated. Just 10 companies account for 83.1% of total secondary trading, with major players like SpaceX, Anduril, Anthropic, OpenAI, and Databricks making up 50.6% of the volume.

Several factors further restrict liquidity:

- Right of First Refusal (ROFR): Companies can block or claim trades within 30 to 60 days, adding uncertainty to transactions.

- Settlement Timelines: Transactions often take 6 to 8 weeks to settle, compared to the T+1 standard in public markets.

Despite these hurdles, the secondary market is growing. By 2025, it reached $240 billion in transaction volume, marking a 48% increase from the previous year. Platforms like EquityZen have played a significant role, completing over 51,000 transactions for nearly 500 private companies as of February 2026.

Bilateral Deals: Pricing and Liquidity

Bilateral deals operate through private, direct negotiations between buyers and sellers, often facilitated by brokers rather than digital order books. Each deal is custom-made, negotiated from scratch, making every transaction distinct.

Pricing in Bilateral Deals

Pricing in bilateral deals happens behind closed doors, without the transparency of a centralized exchange. This lack of a public bid-ask spread or last sale prices means the same company’s shares could sell for $110 in one negotiation and $95 in another – at the exact same time. This illustrates the significant information gaps in these transactions.

"The private secondary market operates as a fragmented, opaque network of bilateral negotiations. There is no centralized exchange publishing bid-ask spreads or last sale prices." – AltStreet Briefing

Several factors drive these pricing disparities. For instance, a seller’s personal circumstances – like tax deadlines or an urgent need for cash – can push prices lower, even if the broader market remains unaffected. Additionally, common stock, often held by employees, typically trades at a 10–20% discount compared to the most recent preferred round valuation. This is because common stock lacks the liquidation preferences and governance rights that preferred shares offer. Buyers also frequently request discounts to account for delays caused by the Right of First Refusal (ROFR) process.

Beyond pricing challenges, the difficulty of finding a matching counterparty further limits the market’s liquidity.

Liquidity in Bilateral Deals

Liquidity in bilateral deals is much thinner than on digital platforms, as transactions rely entirely on manually locating a willing buyer or seller. Without an automated marketplace, participants must navigate this process on their own.

The ROFR process not only affects pricing but also introduces binary execution risk. This means a company can step in and cancel an agreed-upon deal, wasting time and resources. Even when a deal proceeds, completing the transaction – including board approvals and share transfers – can take 6 to 8 weeks.

Legal and administrative costs are another hurdle, averaging $25,000 to $30,000 per deal. These high costs generally limit bilateral transactions to deals worth over $100,000. However, buyers benefit from direct voting and shareholder rights since they appear on the company’s cap table – unlike platform-based deals, where such rights are often retained by an SPV manager.

This direct negotiation model stands in sharp contrast to pre-IPO platforms, paving the way for a more detailed comparison in the next section.

Pricing and Liquidity: A Direct Comparison

When you dive into pre-IPO trading platforms versus bilateral deals, the differences are striking. Pre-IPO platforms function like mini-stock exchanges, using centralized order books that update prices in real time based on active bids and asks. On the flip side, bilateral deals rely on private negotiations. Here, the starting point often comes from the latest funding round or 409A valuation, but the final price remains behind closed doors, inaccessible to the broader market.

Platforms like Hiive add another layer of transparency by publishing indices such as the Hiive50, which tracks the share prices of the 50 most liquid securities and updates hourly. In contrast, bilateral deals are opaque – pricing details are known only to the buyer, seller, and the company’s transfer agent. This secrecy can lead to the same company’s shares trading at different prices simultaneously, a scenario almost unheard of on platforms with visible market depth. These differences extend beyond pricing into execution speed and investment thresholds.

When it comes to execution, platforms using an Alternative Trading System (ATS) can match and execute orders almost instantly. Bilateral deals, however, require time-consuming manual coordination by brokers, extended negotiations, and company approvals. Settlement can stretch to 6–8 weeks, and there’s always the risk that the company’s Right of First Refusal could cancel the deal after weeks of effort.

Investment minimums also set these two approaches apart. Platforms often allow smaller investments, starting as low as $5,000 to $10,000, made possible through SPV structures. Bilateral deals, however, typically demand much higher investments – often $100,000 or more – to cover legal and administrative costs. For smaller investors, platforms open doors that bilateral processes simply can’t.

Comparison Table: Pricing and Liquidity

| Feature | Pre-IPO Trading Platforms | Bilateral Deals |

|---|---|---|

| Price Discovery | Market-driven; real-time bids/asks | Negotiated; reference-based |

| Transparency | High; visible order books and indices | Low; private negotiations |

| Execution Speed | Fast; automated matching (ATS) | Slow; manual coordination and approval |

| Minimum Investment | Lower (often $5,000–$10,000) | Higher (often $100,000+) |

| Liquidity Depth | Centralized pool of verified participants | Fragmented; dependent on broker network |

| Regulatory Oversight | High; often via FINRA-registered ATS [1,22] | Variable; depends on broker/legal counsel |

Market Dynamics and Risks

Private pre-IPO trading operates differently from public markets, largely due to information asymmetry. Private companies disclose minimal data, which creates a unique dynamic. On trading platforms, prices are based on publicly available information. However, in bilateral deals, sellers – often employees or early investors – usually have deeper knowledge of the company’s inner workings. As the Calcix Research Team explains:

"In the secondary market, the buyer often knows more than the seller. Institutional buyers often have access to ‘side letters’ or updated financial disclosures that you… might not".

The forces of supply and demand in these markets also diverge from those in traditional markets. On the supply side, pricing is influenced by factors like company-imposed lock-up provisions, employee vesting schedules, and the pressures faced by venture funds nearing the end of their lifecycle. For instance, venture funds close to term may offer steep discounts to return capital to their limited partners. On the demand side, institutional interest in "hectocorns" (companies valued at $100 billion or more) and sector-specific momentum – especially in areas like AI – can push prices higher, particularly as IPOs draw near. These dynamics, however, come with increased regulatory and counterparty concerns.

Adding to these complexities are regulatory risks. Registered broker-dealers or Alternative Trading Systems (ATS) provide a regulated framework that helps manage settlement and counterparty risks. Bilateral deals, on the other hand, often occur through unregulated brokers or informal channels, leaving them exposed to legal uncertainties, ownership disputes, and settlement failures. For example, the SEC recently took action in a $528 million fraud case against Late Stage Asset Management, which had charged hidden fees while falsely advertising "no-fee" access.

Counterparty risk is another challenge, especially in bilateral deals. While trading platforms verify share ownership and seller identity upfront to reduce risks, bilateral transactions are prone to delays due to Right of First Refusal (ROFR) processes and settlement issues. These delays can stretch to 6–8 weeks, far exceeding the T+1 settlement standard in public markets.

Lastly, valuation uncertainty amplifies discount volatility in secondary markets. Common shares often trade at discounts compared to the most recent preferred funding round because they lack protections like liquidation preferences and anti-dilution clauses. In Q1 2025, secondary shares traded at an average 20% discount to the last funding round valuations. Companies nearing an IPO (within one year) typically see discounts of 12–18%, while those five years away face steeper discounts of 50–65%. This reflects the growing valuation uncertainty over time, compounded by a 4.5% risk-free rate in early 2026, which further pressures these discounts.

Choosing the Right Approach for Crypto OTC Trading

Factors to Consider When Choosing an Approach

When deciding between pre-IPO platforms and bilateral OTC deals, several factors come into play: deal size, privacy needs, and settlement preferences. Pre-IPO platforms typically have investment minimums ranging from $1,000 to $100,000, making them accessible to accredited investors and smaller institutions. On the other hand, OTC desks often cater to high-net-worth individuals and institutional players, with minimum transaction sizes starting at $50,000 for block trades.

Privacy is another key factor. Bilateral OTC transactions occur entirely off public order books, ensuring that sensitive trade details remain private and protected from market speculation. In contrast, pre-IPO platforms provide greater transparency by offering real-time indices like Hiive50 and Forge Private Market Index. However, this visibility can unintentionally expose trading intentions to a wider audience.

Slippage risk also varies between these approaches. For instance, attempting to buy $10 million worth of Bitcoin on a public exchange could move the market against you. OTC desks mitigate this by locking in a single "all-in" price for the entire trade volume, reducing slippage risk. While pre-IPO platforms offer faster execution with automated matching, they may face liquidity challenges for certain private shares. Settlement terms also differ: bilateral deals often allow for customized options like same-day or T+1 settlement, whereas platforms typically rely on standardized clearing processes. These distinctions highlight the importance of tailoring the trading approach to specific needs, something BeyondOTC excels at.

How BeyondOTC Enhances the Trading Experience

BeyondOTC serves as a strategic partner, connecting clients to both pre-IPO opportunities and secure bilateral deals through a robust network of institutional investors, OTC desks, and liquidity providers. Instead of locking clients into a single method, BeyondOTC assesses the unique requirements of each transaction to ensure the most suitable approach is used – whether the priority is privacy, liquidity, or diversified access.

The platform offers a white-glove service that includes direct engagement with top-tier buyers and sellers, personalized settlement options, and thorough KYC/AML compliance. For clients interested in late-stage private companies like SpaceX or OpenAI, BeyondOTC utilizes its network to provide access through regulated Alternative Trading Systems or discreet bilateral deals. This tailored strategy ensures clients achieve optimal pricing, liquidity, and risk management while meeting their specific trading goals and regulatory needs.

Conclusion

When choosing an investment approach, consider factors like pricing transparency, liquidity, and market dynamics. Pre-IPO platforms offer real-time price discovery through standardized digital order books, with entry points starting as low as $1,000. On the other hand, bilateral deals provide negotiated pricing and direct ownership but come with higher thresholds – typically requiring at least $100,000 – and additional legal costs ranging from $25,000 to $30,000.

Both methods come with execution risks. Pre-IPO platforms often involve longer administrative processes, while bilateral deals may provide quicker settlement options, though both depend on company approval and varying timelines. Investors should also be prepared for potential discounts and valuation differences that reflect the inherent uncertainties of the secondary market.

The secondary market’s growth is undeniable, with transaction volumes hitting $240 billion in 2025 – a 48% year-over-year increase – highlighting its increasing appeal among institutional investors. Carefully weighing these trade-offs is essential for making informed decisions and achieving favorable outcomes.

FAQs

Why do the same pre-IPO shares show different prices across platforms?

Pre-IPO shares often come with different price tags across platforms because private markets lack a centralized exchange. Several factors contribute to these differences, including the deal structure, type of shares being sold, block size of the shares, and the urgency of the seller. Additionally, each platform has its own negotiation process and supply-demand dynamics, which play a big role in shaping the final price for the same company’s shares.

How does ROFR affect whether a pre-IPO trade actually closes?

The Right of First Refusal (ROFR) allows a company to step in and purchase shares before they are sold to a third party. In pre-IPO trades, this means the issuing company has the option to buy back the shares, effectively stopping the transaction from moving forward. For anyone involved in pre-IPO deals, grasping how this process works is crucial.

When is an SPV platform trade better than direct ownership in a bilateral deal?

SPV platforms shine when investors are looking for diversification, greater liquidity, and shared access to pre-IPO shares. These vehicles bring multiple investors together, making it easier to invest collectively. They also support secondary market transactions and offer flexibility in terms and conditions.

On the other hand, bilateral deals involve one-on-one negotiations, which can limit liquidity and scalability. SPVs are a better choice for those aiming to tap into wider markets or handle large, less liquid holdings more effectively.