Key Takeaways:

- What are Pre-IPO Discounts?

A pre-IPO discount is the price difference between private shares sold in secondary markets and their expected IPO price. These discounts exist due to the lack of liquidity in private shares, known as the Discount for Lack of Marketability (DLOM). - Typical Discount Ranges:

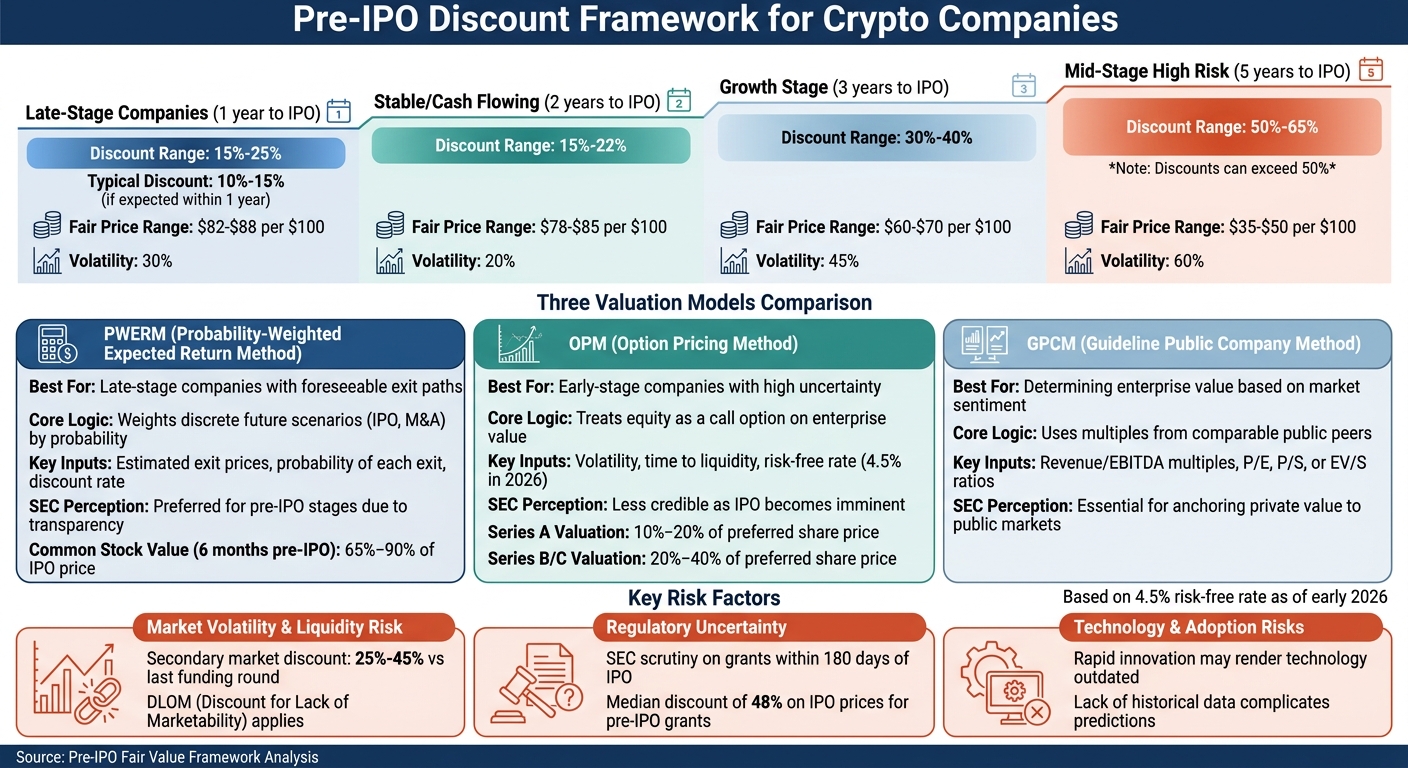

- Late-stage companies (1 year to IPO): 15%-25% discount.

- Mid-stage companies (5 years to IPO): Discounts can exceed 50%.

- Valuation Models for Pre-IPO Pricing:

- PWERM (Probability-Weighted Expected Return Method): Best for late-stage companies close to IPOs.

- OPM (Option Pricing Method): Suitable for early-stage, high-uncertainty ventures.

- GPCM (Guideline Public Company Method): Uses comparable public company metrics to estimate value.

- Key Risks Affecting Discounts:

- Market Volatility: Crypto startups face significant token price fluctuations and liquidity risks.

- Regulatory Challenges: Compliance with evolving laws can impact valuations.

- Technology Risks: Rapid innovation may render a startup’s core technology outdated before IPO.

- Investor Considerations:

- Use multiple valuation models (PWERM, OPM, GPCM) for accurate pricing.

- Request a “waterfall analysis” to understand liquidation preferences.

- Be cautious of information asymmetry – large buyers may have access to disclosures unavailable to smaller investors.

Quick Summary:

Pre-IPO discounts reflect the risks of investing in private companies before they go public. In crypto, these risks are amplified by market volatility, regulatory scrutiny, and technology uncertainty. Valuation models like PWERM, OPM, and GPCM help investors estimate fair prices for private shares, but careful attention to risks and timelines is essential.

Pre-IPO Discount Ranges by Company Stage and Years to IPO

Lesson 4 PreIPO Valuation Techniques | PreIPO® Corporation

sbb-itb-7e716c2

Valuation Models for Pre-IPO Pricing

Figuring out the fair value of pre-IPO shares in cryptocurrency ventures is no simple task. It calls for valuation models that blend traditional financial principles with the unique volatility of the crypto market. These models are applied differently depending on where the company stands on its journey toward going public. Picking the right model – and knowing how to use it – can make or break a valuation, especially under the watchful eyes of the SEC and the market. Let’s break down the key models used for pre-IPO valuations in the crypto space.

Probability-Weighted Expected Return Method (PWERM)

PWERM is all about assigning probabilities to specific exit scenarios, such as an IPO, acquisition, or staying private.

"The PWERM is the dominant methodology for pre-IPO companies precisely because it can incorporate IPO probability and anticipated offering price as explicit inputs." – 409A-valuation.com

As the IPO date gets closer, PWERM valuations tend to align with the expected offering price. In the six months leading up to an IPO, the value of common stock usually reaches 65% to 90% of the anticipated IPO price. This reflects reduced uncertainty and a smaller Discount for Lack of Marketability. However, there’s a catch: companies might game the system by assigning overly low probabilities to favorable outcomes. This tactic can artificially lower valuations, allowing insiders to grab low-priced options.

Option Pricing Method (OPM) in Pre-IPO Valuation

OPM takes a different approach, treating equity classes as call options on the company’s enterprise value. It factors in liquidation preferences and participation rights to assess value. This method is particularly suited to early-stage ventures where uncertainty is high. Key inputs include:

- Current enterprise value

- Volatility

- Time to liquidity

- Risk-free interest rate (around 4.5% in early 2026)

At the Series A stage, OPM typically values common stock at just 10% to 20% of the preferred share price, reflecting the impact of liquidation preferences. As companies progress to Series B and C rounds, this ratio rises to 20% to 40%. However, as the IPO nears, OPM becomes less effective because the range of possible outcomes narrows. At this stage, the SEC and auditors often prefer PWERM for its transparency and reliability.

Guideline Public Company Method (GPCM)

GPCM, also called Comparable Company Analysis, calculates enterprise value by applying financial multiples – like revenue, EBITDA, or EV/Sales – from similar public companies to the target company’s metrics. For example, a crypto exchange preparing for an IPO would identify comparable publicly traded peers, calculate their trading multiples, and adjust them to fit its financials. This method ties private valuations to public market trends, which is critical in the volatile crypto sector.

The challenge? Finding truly comparable companies. Many blockchain ventures have distinct business models or operate in emerging niches with no direct public peers. GPCM works best when paired with PWERM or OPM. For instance, GPCM can establish enterprise value under various scenarios, while PWERM weights those scenarios or OPM allocates value among share classes.

Here’s a quick comparison of the three methods:

| Feature | Option Pricing Method (OPM) | Probability-Weighted Expected Return Method (PWERM) | Guideline Public Company Method (GPCM) |

|---|---|---|---|

| Primary Use Case | Early-stage companies with high uncertainty | Late-stage companies with foreseeable exit paths | Determining enterprise value based on market sentiment |

| Core Logic | Treats equity as a call option on enterprise value | Weights discrete future scenarios (IPO, M&A) by probability | Uses multiples from comparable public peers |

| Key Inputs | Volatility, time to liquidity, risk-free rate | Estimated exit prices, probability of each exit, discount rate | Revenue/EBITDA multiples, P/E, P/S, or EV/S ratios |

| SEC Perception | Less credible as an IPO becomes imminent | Preferred for pre-IPO stages due to transparency | Essential for anchoring private value to public markets |

Risk Factors Affecting Pre-IPO Discounts

Pre-IPO discounts are a reflection of the risks tied to investing in private companies before they go public. In the crypto and blockchain industry, these risks are amplified by the sector’s inherent volatility, evolving regulations, and rapid technological changes. Grasping these factors is crucial for accurately valuing pre-IPO shares.

Market Volatility and Liquidity Risk

Crypto startups present a unique challenge with their volatility. First, there’s token price volatility – the fluctuating value of tokens can directly impact a company’s assets, revenue, and demand. Second, there’s the liquidity issue, as pre-IPO shares can’t be traded on public exchanges. This lack of marketability often leads to a Discount for Lack of Marketability (DLOM).

In 2026, private shares in the secondary market typically trade at discounts ranging from 25% to 45% compared to their last preferred funding round valuation. However, if a company is expected to go public within a year, the discount narrows to 10% to 15%. Conversely, companies with IPOs projected five years out may see discounts exceeding 50%. Each year of delay compounds the risk – your capital remains tied up without earning returns and is exposed to potential total loss.

Rising interest rates further deepen these discounts, as they increase the opportunity cost of holding illiquid assets. Additionally, high volatility in comparable public companies makes buyers hesitant, leading them to demand larger discounts as a buffer against unforeseen market downturns.

Another layer of complexity comes from information asymmetry. Institutional buyers in the secondary market often have access to key financial details or "side letters" that individual sellers lack. This imbalance can result in unfair pricing, especially if sellers are unaware of an upcoming IPO filing. Before selling, investors should request a "waterfall" analysis to understand how liquidation preferences may impact their returns, particularly in less-than-ideal exit scenarios.

This market volatility sets the stage for additional uncertainties, particularly those driven by regulatory challenges.

Regulatory Uncertainty in the Crypto Sector

Regulatory hurdles are more than just background noise – they directly affect costs and valuations. Crypto startups often grapple with compliance issues tied to anti-money laundering (AML) laws, securities regulations, tax policies, and data protection standards. These challenges can limit their market scope and growth potential, which in turn impacts pre-IPO pricing.

"Crypto startups face various regulatory hurdles and compliance issues that can affect their growth potential and market access." – FasterCapital

Valuation models like PWERM are designed to address this uncertainty by assigning probabilities to various regulatory scenarios. Hostile regulations might lower the chances of a successful IPO or widespread adoption, while supportive policies can enhance legitimacy and stability.

The SEC plays a significant role here, scrutinizing every option grant made within three to five years before an IPO to ensure fair market value (FMV) wasn’t artificially suppressed. Grants issued within 180 days of an IPO filing receive heightened scrutiny, as the IPO is deemed a foreseeable event during this window. A study of 121 companies revealed that option holders enjoyed median discounts of 48% on IPO prices for grants made during IPO preparations.

Proactive engagement with regulators is essential. Investors should work with policymakers early to build trust and gain clarity on compliance requirements. Diversifying revenue streams is another way to mitigate risks, ensuring companies aren’t overly reliant on a single token or platform that might face regulatory targeting. Maintaining detailed documentation of valuation assumptions and key events is also crucial to defend against SEC "cheap stock" investigations.

Beyond regulatory and market risks, technological advancements and adoption rates further complicate pre-IPO valuations.

Technology and Adoption Risks

Innovation in the crypto sector moves at breakneck speed, which can be both an asset and a liability. A startup’s core technology or protocol could become outdated before it even reaches its IPO. This technological obsolescence risk is compounded by concerns over product defensibility – how unique and protected is the company’s intellectual property, such as patents for new consensus mechanisms or cryptographic solutions?

The lack of historical data and untested business models in this sector makes it challenging to predict user engagement, churn rates, and overall readiness for public markets.

In 2026, investors are prioritizing quality. Companies with a clear, near-term path to liquidity (within 18 months) see their shares trade at a premium compared to those with uncertain three-to-five-year timelines.

| Scenario | Years to IPO | Volatility | Expected Discount | Estimated Fair Price (per $100) |

|---|---|---|---|---|

| Late Stage (Pre-IPO) | 1 Year | 30% | 12% – 18% | $82 – $88 |

| Growth Stage | 3 Years | 45% | 30% – 40% | $60 – $70 |

| Mid Stage (High Risk) | 5 Years | 60% | 50% – 65% | $35 – $50 |

| Stable/Cash Flowing | 2 Years | 20% | 15% – 22% | $78 – $85 |

Note: Figures are based on a 4.5% risk-free rate as of early 2026.

Adjusting for these risks is crucial when applying models like PWERM. Investors should map out potential future exit scenarios, assigning probability weights to less favorable outcomes like technological failure or slow adoption. Additionally, DLOM should be adjusted based on the time to exit – longer lock-up periods warrant deeper discounts. If similar public crypto stocks exhibit significant daily swings (e.g., 5%), it’s wise to increase pre-IPO discounts to account for potential market crashes.

Framework for Assessing Pre-IPO Discounts

Once the key risk factors are identified, the next step is to apply a structured method for pricing pre-IPO shares. This process combines various valuation models, adjusts for crypto-specific risks, and evolves as the company progresses toward its public debut. This framework helps crypto investors and advisors turn complex market data into actionable insights.

Combining PWERM, OPM, and GPCM

To capture different valuation angles, integrate PWERM, OPM, and GPCM:

- PWERM outlines potential exit scenarios, such as an IPO, acquisition, or remaining private, and assigns probability weights to each.

- GPCM determines the enterprise value in an IPO scenario by using revenue or EBITDA multiples from comparable public companies.

- OPM allocates value across equity classes, factoring in liquidation preferences and participation rights.

This blended approach works well for crypto ventures with intricate capital structures. Early-stage companies often rely on OPM due to high uncertainty. As an IPO nears, PWERM gains prominence, aligning the common stock value with the expected IPO price.

"The pre-IPO period is characterized by rapid and sometimes discontinuous value increases." – 409A-valuation.com

For GPCM, it’s essential to reconcile public market multiples with recent private transaction multiples. For instance, if public crypto infrastructure companies trade at 8× revenue and the target recently raised funds at 12× revenue, the premium must be justified by factors like better technology, stronger network effects, or clearer profitability.

Applying the Framework to Actual Scenarios

Take May 2026 pre-market data for Gensyn, a decentralized compute network for AI workloads, as an example. Its pre-market price of $0.032 and Fully Diluted Valuation (FDV) of $329 million reflect strong demand in AI and DePIN projects.

To evaluate this pricing:

- Start with GPCM: Compare Gensyn’s FDV to public companies in the AI infrastructure space. If Gensyn’s revenue projections (e.g., $20 million in annual recurring revenue) align with public multiples, the implied enterprise value – around $300 million to $400 million – supports the $329 million FDV.

- Use PWERM: Assign probabilities to different exit scenarios, favoring a near-term token generation event over delayed outcomes or failure. After blending these values, apply a Discount for Lack of Marketability (DLOM) of 12% to 18%, reflecting typical discounts for a one-year lock-up period.

- Apply OPM: If there are multiple token classes or vesting schedules, allocate value based on liquidation preferences.

Maintaining a consistent valuation cadence is critical, especially with regulatory scrutiny on grants made within 180 days of an IPO filing. The table below outlines a recommended schedule:

| Time Before IPO Filing | Recommended Valuation Cadence | Key Triggers | SEC Risk Level |

|---|---|---|---|

| 18–24 months | Semi-annual | New funding rounds, M&A activity | Moderate |

| 12–18 months | Quarterly | Banker engagement, IPO discussions | Elevated |

| 6–12 months | Quarterly | S-1 drafting, price range talks | High |

| 0–6 months | Per-grant | Active S-1 prep, underwriter selection | Very High |

This structured method ensures valuations remain accurate and defensible.

Custom Solutions for BeyondOTC Clients

BeyondOTC applies this framework to provide tailored valuation and advisory services for pre-IPO investments in the crypto sector.

For sellers, BeyondOTC conducts waterfall analyses to clarify how liquidation preferences impact common shareholders. This prevents predatory offers that arise from information asymmetry, such as institutional buyers having access to "side letters" or extra disclosures unavailable to individual sellers.

For buyers, BeyondOTC calculates the net liquidity premium – accounting for a 20% to 35% tax impact – to provide clarity on actual proceeds unless shares qualify for Section 1202 QSBS treatment. BeyondOTC also collaborates with external auditors to ensure valuation methods – whether OPM, PWERM, or a hybrid – are defensible in S-1 filings. This reduces the risk of financial restatements that could delay an IPO.

In the 2026 market, where the risk-free rate hovers around 4.5% and companies typically need $100 million to $200 million in annual recurring revenue to go public, BeyondOTC helps clients benchmark investments against these thresholds. With a focus on companies that have a clear 18-month path to liquidity, BeyondOTC leverages its network of centralized and decentralized exchange connections, market makers, and legal consultants to ensure clients can act decisively in this high-stakes environment.

Case Studies in Crypto and Blockchain Pre-IPOs

Successful Pre-IPO Valuations in Crypto

In April 2026, BitGo made headlines by pricing its IPO above the initial range, securing a $2 billion valuation. This crypto custody firm showed that having a clear path to profitability and strong institutional relationships can lead to premium pricing, even in unpredictable markets.

Another standout example is Filecoin, which set a record in September 2017 by raising $257 million through a two-step process. First, it conducted a $52 million private presale, selling tokens at $0.75 per coin to major venture capital firms like Sequoia Capital, Andreessen Horowitz, and Union Square Ventures. Then, it followed up with a $205.8 million public ICO, where tokens reached $5.15 per coin. Filecoin’s use of the Simple Agreement for Future Tokens (SAFT) framework, combined with limiting participation to accredited investors, helped bolster its reputation in a market often marred by scams. According to Jack Leung:

"Being viewed as a legitimate project is an incredibly important decision… providing extra investor confidence is absolutely paramount to a successful project".

In another example, the SpaceX SPCX Mirror Note offering in April 2026 showcased how tokenization can make pre-IPO investments more accessible. Gate.com issued digital certificates priced at 590 USDT per SPCX, representing a $1.4 trillion valuation. The minimum investment was just 100 USDT, a stark contrast to the millions typically required for traditional pre-IPO equity. This offering raised approximately $20 million from retail investors in just three days.

Lessons from Challenging Valuations

While these successes highlight potential, they also reveal some of the challenges tied to pre-IPO pricing. Take Filecoin, for instance: its pricing disparity – $0.75 per coin for VCs compared to a 586% higher public price – exposed significant information gaps. Venture capitalists valued the market at $25 billion to $500 billion, while public investors assumed a market size exceeding $2 trillion.

Another issue arises from the manipulation of valuation methods like the Probability-Weighted Expected Return Method (PWERM). Companies often present overly pessimistic projections to justify low valuations. Research into 121 biotechnology firms revealed that pre-IPO companies granted options with a median discount of 48% compared to the eventual IPO price. About 50% of these discounted options were issued within 45 days of the IPO, creating potential windfalls averaging $2.6 million per CEO. Sven Riethmueller, Clinical Associate Professor of Law at Yale Law School, explained:

"Pre-IPO firms exploit a seemingly quantitative stock valuation technique, the Probability-Weighted Expected Return Method. They conjure up exceedingly pessimistic prognostications as to IPO outcome which allow them to set option exercise prices well below the price at which they sell shares to investors in their upcoming IPO".

The SEC v. ZM Quant Investment Ltd. case from October 2024 further highlights the risks of manipulated pricing. The SEC accused market makers of engaging in "wash trading" schemes to create artificial trading volume, misleading retail investors into purchasing crypto assets at inflated prices. This case underscores the importance of verifying that valuation inputs come from an "orderly market", especially when digital exchanges lack robust oversight.

These challenges emphasize the importance of using rigorous valuation models, such as combining PWERM, OPM, and GPCM, to mitigate risks and ensure more reliable pre-IPO assessments.

Conclusion: Key Takeaways for Crypto Pre-IPO Valuations

Summary of Fair Value Frameworks

Valuing crypto pre-IPO shares requires a flexible approach that evolves as a company approaches its public debut. Early on, traditional equity models like the Option Pricing Method (OPM) are effective in handling uncertainty. However, as the IPO timeline narrows to 12–18 months, the Probability-Weighted Expected Return Method (PWERM) becomes crucial. This method accounts for specific exit scenarios, such as an IPO, acquisition, or remaining private, offering a more tailored valuation approach. For companies with intricate capital structures, combining OPM and PWERM provides a more precise allocation of value across different stock classes.

For crypto-focused firms, additional factors like token economics, network effects, and protocol utility must be considered. While the Guideline Public Company Method (GPCM) can provide benchmarks, analysts must validate data from the "principal market" – the exchange with the highest activity – to avoid distortions from wash trading or fragmented pricing. Liquidity constraints and exit timing risks also play a significant role in shaping valuation discounts. As the Calcix Research Team aptly noted:

"Time is the single most aggressive ‘tax’ on your private share value." – Calcix Research Team

This framework lays the groundwork for actionable valuation strategies.

Final Guidance for Investors and Advisors

To establish a reliable valuation range, use multiple methods – VC, Comparables, and DCF – and cross-check results. If there are major discrepancies, focus on analyzing the assumptions rather than defaulting to the most favorable outcome. By incorporating early-stage risk assessments, investors can better protect themselves from information gaps and unfavorable exit scenarios. Adjust discount ranges based on IPO timing; late-stage companies nearing an IPO typically trade at smaller discounts, while mid-stage firms face larger cuts.

Waterfall analysis is essential before any transactions to identify liquidation preferences that could negatively impact common shareholders’ returns. Additionally, verify whether the investment qualifies under Section 1202’s QSBS rules, which could exempt 100% of gains from federal taxes. For companies experiencing extreme token price volatility, advanced models like the Ghaidarov Average Strike Protective Put Option Model can account for rapid market swings far better than standard Black-Scholes models, especially when volatility exceeds 150%.

Finally, be vigilant about information gaps. Institutional buyers often have access to updated financial disclosures or side agreements that individual sellers may not. In a fragmented crypto market, where wash trading can inflate trading volumes artificially, it’s critical to ensure pricing reflects an orderly market. Firms like BeyondOTC offer institutional-grade due diligence and direct access to top-tier buyers and sellers, helping to create more equitable opportunities in secondary transactions.

FAQs

How do I choose between PWERM, OPM, and GPCM for a specific pre-IPO deal?

Choosing between PWERM, OPM, and GPCM depends on the specific traits of the company and the context of the valuation:

- PWERM (Probability-Weighted Expected Return Method): Works well for assessing multiple potential exit outcomes, like an IPO or acquisition, by assigning probabilities to each scenario.

- GPCM (Guideline Public Company Method): A good fit for businesses with stable capital structures and readily available market comparables.

- OPM (Option Pricing Method): Best suited for early-stage companies, treating equity as a call option based on the company’s future growth potential.

What documents should I ask for before buying or selling pre-IPO shares in a secondary trade?

Before diving into trading pre-IPO shares, it’s essential to gather and review a few key documents to make informed and compliant decisions. Start with shareholder agreements and stock ownership records to confirm ownership and understand any restrictions. Next, examine company financials and valuation reports to get a clearer picture of the company’s performance and the fair value of the shares. Don’t forget to request purchase agreements for details on the terms of the transaction.

Additionally, take a close look at securities law documentation and any company disclosures, such as investor presentations or due diligence materials. These documents provide crucial insights into the company’s operations and legal compliance, helping you verify ownership and assess potential risks before moving forward.

How do liquidation preferences affect the value of my common shares?

When a company has liquidation preferences in place, it can significantly impact the value of common shares. These preferences ensure that preferred shareholders are paid first during a liquidation event, such as a sale or bankruptcy. As a result, common shareholders may find their shares worth less – or even nothing – after preferred shareholders receive their payouts.

This prioritization can mean that common shares often fall below their nominal value, especially when the company’s proceeds are insufficient to cover the preferred payouts. If you hold common shares, it’s essential to understand how these preferences work to get a clearer picture of your shares’ actual value.