Late-stage pre-IPO rounds often deliver better returns than early secondary sales. Here’s why:

- Lower Risk: Late-stage companies have proven business models, institutional backing, and audited financials. Early secondary sales involve higher uncertainty, as many startups fail early.

- Faster Liquidity: Late-stage investments typically offer liquidity within 12–18 months through IPOs, while early secondary sales may require holding periods of 5–10+ years.

- Pricing Trends: Late-stage deals are priced closer to public market benchmarks, whereas early secondary sales often involve steep discounts (40–70%) due to higher risks.

- Return Potential: Late-stage investors benefit from "equity rerating" as private valuations align with public market standards, while early secondary buyers face dilution and longer timelines.

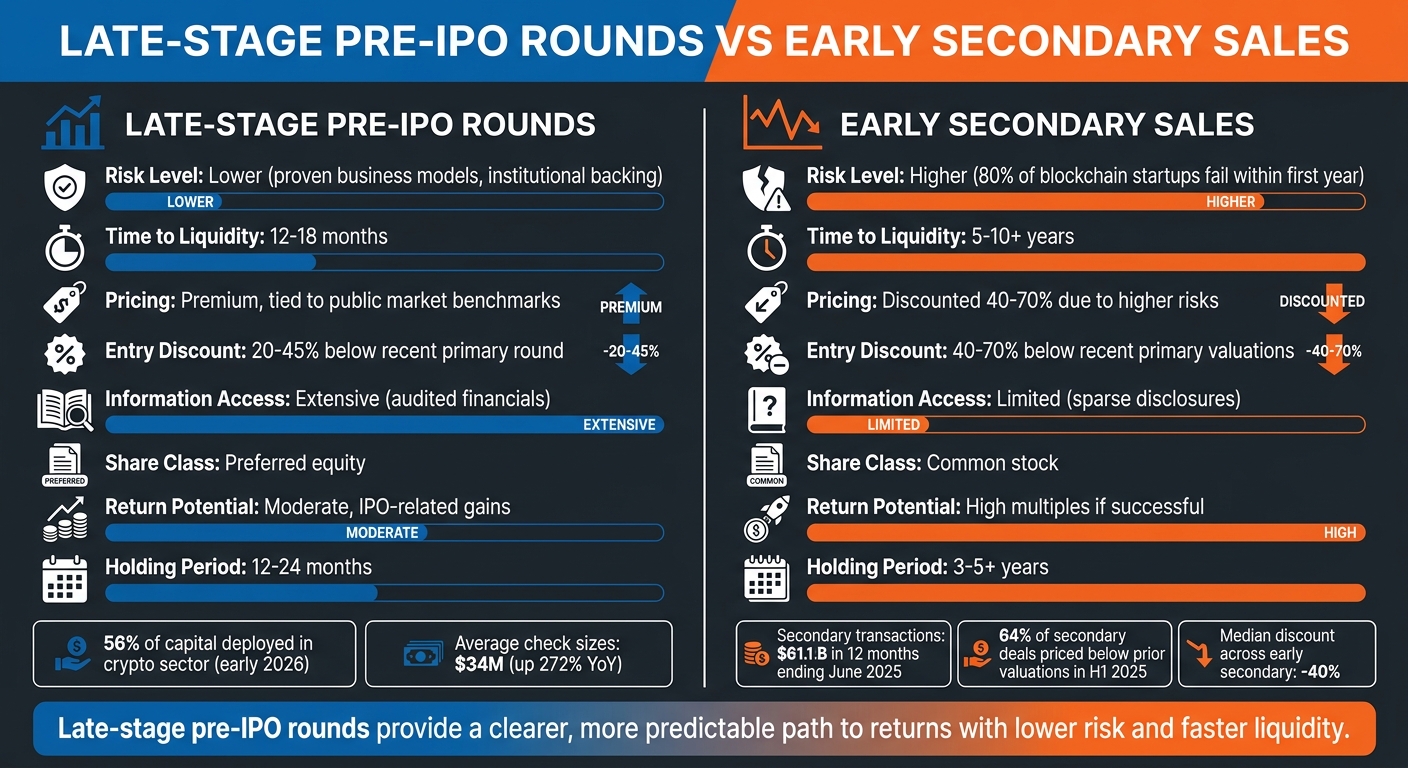

Quick Comparison

| Factor | Late-Stage Pre-IPO Rounds | Early Secondary Sales |

|---|---|---|

| Risk Level | Lower | Higher |

| Time to Liquidity | 12–18 months | 5–10+ years |

| Pricing | Premium, tied to public benchmarks | Discounted 40–70% |

| Information Access | Extensive | Limited |

| Share Class | Preferred equity | Common stock |

| Return Potential | Moderate, IPO-related gains | High multiples if successful |

Late-stage pre-IPO rounds provide a clearer, more predictable path to returns, making them a preferred choice for many investors.

Late-Stage Pre-IPO vs Early Secondary Sales Investment Comparison

Pre-IPO Investing: Risks, Rewards, and Strategy

sbb-itb-7e716c2

What Drives the Performance Gap

Four key factors shape the performance gap: market dynamics, pricing, risk, and profit potential. Let’s break down how these elements contribute to the differences in outcomes.

Market conditions currently favor late-stage equity investments. By early 2026, later-stage deals accounted for 56% of all capital deployed in the crypto sector, with average check sizes surging 272% year-over-year to $34 million. This trend reflects what many call the "barbell economy", where capital flows heavily toward established infrastructure companies with proven revenue streams. Meanwhile, early-stage speculative deals face what some analysts describe as a "brutal extinction event". Regulatory advancements, such as the Clarity Act and Europe’s MiCA, have further reinforced this shift, making it easier for institutional investors to back equity structures with clear paths to public listings.

Pricing trends highlight a stark divide between strategies. During the first half of 2025, 64% of secondary deals were priced below their previous valuations – up 10% from the prior year – with median discounts ranging from -40% to -55% in less popular sectors like GameFi. On the flip side, the most sought-after late-stage deals commanded premiums exceeding 200% of prior valuations, driven by institutional demand for pre-IPO opportunities. This disparity stems from what SecondLane refers to as "lingering high valuations" left over from the previous bull market in early-stage assets. In contrast, late-stage valuations are increasingly tied to public market benchmarks, such as Coinbase.

The risk profiles of the two approaches couldn’t be more different. Early secondary sales come with significantly higher risk, as 80% of blockchain startups fail within their first year. Late-stage investments, however, benefit from proven business models, detailed disclosures, and institutional-grade operations, which reduce uncertainty. Additionally, late-stage deals often offer liquidity within 12–18 months through IPOs, compared to the longer and less predictable 6–24 month token unlock periods typical of early secondary sales. As Sahil Agrawal from Investor Insights puts it, "Late-stage investments are not just about stability; they are also about timing".

Profit potential is closely tied to the timing of value creation. While much of a company’s growth now occurs in private markets before going public, late-stage investors can still capture significant upside through "equity rerating." For example, Kraken’s secondary valuation jumped from $6.82 billion to over $7.7 billion following its IPO filing, fueled by $750 million in trades over just 90 days. The combination of reduced risk, shorter exit timelines, and rerating opportunities explains why late-stage pre-IPO rounds are often preferred over early secondary sales.

1. Late-Stage Pre-IPO Rounds

Market Dynamics

Late-stage pre-IPO funding rounds have become a major focus in crypto venture capital as companies gear up for public listings. Regulatory changes, like the Clarity Act and the Genius Bill, have made it easier for institutional investors to engage, fueling a wave of crypto IPO preparations. Companies such as Circle, Kraken, and Gemini are actively moving toward traditional public offerings, creating a surge of late-stage investment opportunities with clear exit strategies. In the 12 months ending June 2025, venture secondary transactions hit $61.1 billion, exceeding the $58.8 billion generated by VC-backed IPOs during the same timeframe. These trends are setting the stage for stronger valuations and reduced risks, which are explored further below.

Valuation Trends

Valuations in late-stage rounds are increasingly tied to public market benchmarks, moving away from speculative private-sector metrics. The secondary market now looks to companies like Coinbase for guidance, using metrics such as EV/Revenue multiples to establish more grounded valuations. For example, Circle’s shares were valued between $5.0 billion and $5.25 billion before its IPO, which ultimately priced at $6.8 billion. This demonstrates how late-stage investors can benefit when private valuations align with public market standards, leading to equity rerating.

Risk Profiles

Late-stage investments generally carry lower risks compared to earlier-stage opportunities. These companies often have established business models, institutional-grade operations, and more transparent disclosures. On average, tech companies now spend over 12 years developing before going public. While macroeconomic factors can sometimes delay IPOs, late-stage rounds typically offer a more predictable path to liquidity. That said, information asymmetry remains a challenge, as private companies disclose less than their public counterparts.

Return Potential

The combination of favorable market conditions and reduced risks creates opportunities for late-stage investors to achieve "Synthetic Alpha" – premium returns generated by buying shares at a discount. Investors in these rounds often acquire shares at a 20% to 45% discount compared to the most recent primary funding round. This discount provides a safety margin; for instance, purchasing at a 30% discount on a $5 billion valuation can help cushion against potential value drops. A case in point is Uber Technologies: while early seed investors achieved astronomical theoretical returns of 2,000,000%, late-stage Series D investors still secured a solid 4× return by the IPO – far outperforming public investors, who only saw annualized returns of about 8–9%.

"The IPO has fundamentally inverted from a primary growth-funding mechanism into a later-stage liquidity event, with much of the value creation now happening in private markets".

This shift underscores how late-stage investors are uniquely positioned to capture the final wave of private market value creation before a company transitions to the public stage.

2. Early Secondary Sales

Market Dynamics

Early secondary sales operate in a very different environment compared to the stability of late-stage rounds. While traditional secondary markets often focus on companies nearing IPOs, the crypto private market skews heavily toward seed and pre-seed stages, which made up 82% of all secondary offers in the first half of 2025. This creates a market defined by early-stage risk and significant volatility.

The emergence of organized trading platforms has sped up deal closures. Secondary deal activity jumped 73% year-over-year, climbing from 131 deals in H1 2024 to 413 in H1 2025. However, this rapid growth brought pricing challenges. A combination of lingering high valuations from the 2024 bull market and large token unlocks created an oversupply, forcing many venture capitalists and project teams to sell at steep discounts to generate liquidity.

The buyer landscape has also shifted, with three distinct groups now dominating the space:

- Long-term strategic buyers looking for portfolio additions.

- Mid-term opportunistic buyers targeting specific exit windows.

- Short-term tactical buyers employing strategies like perpetual hedging to secure "Synthetic Alpha".

Interestingly, 56% of digital asset secondary deals in 2025 closed in under a month, largely driven by these tactical buyers.

Valuation Trends

Valuations in early secondary sales face a tough reality: the longer the wait for a liquidity event, the deeper the discount buyers demand. In H1 2025, 64% of secondary deals were priced below their prior primary valuations – a 10% increase from the previous year – with the median discount across all early secondary transactions reaching about -40%.

Information asymmetry adds another layer of difficulty. Buyers often lack access to robust financial data, relying instead on outdated pitch decks or media reports. This lack of transparency pushes buyers to demand steep discounts, often between 40% and 70%, particularly for smaller players. For projects outside the top 100 by market cap, discounts could reach as high as 70% with one-year lock-ups.

"Most alts were over-valued by at least 5x, with further downside upon introduction of new floating supply." – Taran, Founder, STIX

There’s also a noticeable split across sectors. Infrastructure-heavy areas like Layer 1 protocols and AI-compute narratives saw median discounts of -25%, while consumer-facing sectors like GameFi suffered median discounts of -55%, as 93% of GameFi projects remained inactive.

Risk Profiles

Early secondary sales come with unique risks that set them apart from late-stage investments. Operational hurdles, such as Right of First Refusal (ROFR) clauses and complex vesting schedules, add layers of complexity. ROFR clauses allow companies to block sales and repurchase shares after a 30–45 day review period, potentially cutting secondary buyers out of deals. Investors must also contend with multi-jurisdictional regulations and the risk of "zombie unicorns" – companies with high valuations but no clear path to liquidity.

The fragmented nature of this market means the same shares can trade at significantly different prices due to the lack of centralized price discovery.

Another risk lies in share class differences. Common shares, often sold by employees in early secondary transactions, are particularly vulnerable in a "down exit" scenario. Preferred shares, on the other hand, come with liquidation preferences that protect capital. This dynamic can leave common shareholders with nothing if preferred shareholders absorb all available exit proceeds. To mitigate this, investors should request a waterfall analysis to assess the impact of liquidation preferences.

Return Potential

Despite the risks, early secondary sales can still offer strong returns. The key lies in acquiring shares at steep discounts – typically 40% to 70% below recent primary valuations. However, the return profile is very different from late-stage investments. Early secondary buyers often face holding periods of 3–5 years, compared to 12–24 months for late-stage deals, which increases risk and reduces annualized returns. Additionally, future funding rounds can dilute returns, so investors usually model a 10–15% buffer in their exit projections.

Taxes also take a bite out of returns. Private share sales trigger immediate tax liabilities of 20–35%, cutting into liquidity. Combined with longer holding periods and higher failure rates, early secondary investments need significantly higher gross returns to achieve the same net Internal Rate of Return (IRR) as late-stage deals. For example, a Growth Stage investment with a 3-year horizon and 45% volatility requires a 30–40% discount to account for time and risk, compared to just 12–18% for a late-stage Pre-IPO deal with a 1-year horizon.

These challenges set the stage for comparing the pros and cons of early secondary sales versus late-stage pre-IPO rounds.

Advantages and Drawbacks

When considering investment strategies, it’s crucial to weigh the pros and cons of late-stage pre-IPO rounds versus early secondary sales. Each approach comes with its own risks, rewards, and timelines. Late-stage pre-IPO rounds offer lower risk and quicker liquidity, while early secondary sales provide deeper discounts but carry higher uncertainty.

Late-stage pre-IPO rounds allow investors to tap into companies that are more established, often with audited financials and backing from institutional investors. This reduces much of the guesswork typically involved in earlier-stage investments. However, the trade-off here is that most of the growth potential has already been realized, which can limit the potential for high returns compared to early-stage opportunities.

On the other hand, early secondary sales present the chance to purchase shares at significant discounts – sometimes 40–50% below recent primary valuations. This creates the potential for substantial returns if the company eventually succeeds. But with this opportunity comes notable challenges: holding periods can stretch over 5 to 10 years or more, and buyers often have to make decisions with very limited financial information. Additionally, common shares, which are typical in these transactions, come with risks tied to liquidation preferences that could impact final returns.

Here’s a side-by-side look at the key differences between these strategies:

| Factor | Late-Stage Pre-IPO Rounds | Early Secondary Sales |

|---|---|---|

| Risk Level | Lower; proven business model | Higher; more uncertainty |

| Time to Liquidity | 12–24 months | 5–10+ years |

| Pricing | Premium; tied to public comparisons | Discounted 40–50% below last round |

| Information Access | Extensive; audited financials | Limited; sparse disclosures |

| Share Class | Preferred equity | Common stock |

| Return Potential | Moderate; IPO-related gains | High multiples if successful |

For example, as seen with Circle’s IPO, late-stage rounds can provide meaningful post-IPO gains. Meanwhile, early secondary buyers often face longer timelines, as companies now take a median of 13 years to go public – far longer than the 4-year median seen in the 1990s. This extended wait underscores the patience required for early secondary investments but also highlights the potential for outsized rewards in the right scenarios.

Conclusion

The benefits of late-stage pre-IPO investments stand out when compared to early secondary sales. These rounds offer advantages in terms of risk, liquidity, and returns. With entry discounts ranging from 20% to 45% below the most recent primary round prices and holding periods typically between 12 and 18 months, they provide a level of safety that earlier-stage investments often lack.

When investing, entry price and share class are critical considerations. A 30% difference in entry discount can nearly double net profits after fees. It’s also essential to confirm whether you’re purchasing Preferred shares, which include liquidation preferences, or Common stock, which carries more risk in a downturn. Building connections with company CFOs can help manage risks like the Right of First Refusal (ROFR), where companies may reclaim shares at your negotiated price.

This trend toward late-stage equity is gaining momentum, as evidenced by recent high-profile IPO filings from companies like Kraken and Gemini. Capital is increasingly flowing toward businesses with established models, with late-stage rounds taking a larger share of the investment pie.

To maximize returns, calculate outcomes using Net IRR to account for fees and dilution. Extend holding period estimates by at least six months to accommodate post-IPO lock-ups, and factor in a 10% to 15% dilution buffer. Additionally, ensure that any capital deployed isn’t needed for at least 24 months, as individual exits can face delays, even for companies nearing public listing.

"The entry discount is the single most powerful variable in your control. A 30% difference in entry price leads to nearly double the net profit after all fees are settled." – Calcix Research Team

In today’s market, the IPO represents the finish line, not the starting point. Late-stage private rounds offer the opportunity to capture what some call the "Innovation Premium" – the value created before companies transition into slower-growth public entities. Focus on firms with regulatory clarity in areas like stablecoins, payments infrastructure, and compliance tools. Always evaluate investments using three exit scenarios – Base, Bull, and Bear – before committing capital. Late-stage pre-IPO rounds remain a compelling way to harness the final surge in private market value before these companies go public.

FAQs

How do I confirm I’m buying preferred shares, not common?

To make sure you’re buying preferred shares, take a close look at the offering documents or directly ask the seller about the type of stock being sold. Preferred shares usually come with perks like priority for dividends and liquidation rights. You can also double-check with the broker or platform you’re using. For added clarity, review the company’s cap table or investment agreement to confirm the shares’ classification. This way, you’ll have a clear understanding of the rights attached to the shares.

What due diligence matters most in a pre-IPO round?

When evaluating a company in a pre-IPO round, there are several critical factors to consider. First, take a close look at the company’s business model. Is it reliable and well-established? Next, assess its revenue growth and whether it demonstrates consistent upward momentum. The company’s market position is another vital aspect – how strong is its standing compared to competitors?

Understanding valuation trends is equally important. Are valuations reasonable, or do they seem inflated? Additionally, pay attention to the terms of preferred shares and liquidation preferences, as these can significantly impact your returns. Finally, evaluate the company’s path to liquidity – how and when will you be able to exit your investment?

By carefully analyzing these elements, you can better gauge the potential risks and rewards of investing in a pre-IPO opportunity.

How should I model net IRR with dilution and lock-ups?

To calculate net IRR while factoring in dilution and lock-up periods, start by adjusting your cash flow projections. This means accounting for dilution from future funding rounds, which will reduce ownership stakes, and delays in liquidity caused by lock-up periods. Additionally, apply valuation discounts – typically ranging from 25% to 45% – to your purchase price estimates to reflect these factors.

Once you’ve made these adjustments, include all relevant elements in your IRR calculation: the initial investment, the impact of dilution, the timing delays from lock-ups, and the eventual exit proceeds. By inputting these modified cash flows into an IRR calculator, you can derive a more accurate net IRR that reflects these real-world considerations.