In recent years, companies like SpaceX, Stripe, and Databricks have delayed going public, staying private for over a decade – far longer than the 7-year average seen a decade ago. Why? The rise of private funding, market volatility, and the ability to avoid public market pressures are key factors. Here’s a quick breakdown:

- Private Funding Access: By 2024, $2.6 trillion in private equity and venture capital allowed startups to secure massive funding without IPOs.

- Market Volatility: Public markets demand profitability and steady growth, which can stifle bold, long-term projects.

- Operational Freedom: Staying private shields companies from quarterly earnings pressure and regulatory burdens, enabling ambitious goals.

For example:

- SpaceX: Valued at $400 billion, it uses private funding and stock buybacks to fund Starlink and Mars projects.

- Stripe: Profitable since 2024, it raised $140 billion via secondary offers to expand into AI and stablecoins.

- Databricks: With $5.4 billion in revenue, it raised $10 billion in private funding to compete with Snowflake and Oracle.

While private markets empower companies to grow on their terms, retail investors often miss out on early-stage growth, gaining access only after valuations mature. For those seeking early opportunities, private market platforms or venture funds can offer alternatives.

1. SpaceX

Market Volatility

SpaceX has chosen to steer clear of the ups and downs of public markets, a decision Elon Musk has openly supported:

"Being public is definitely an invitation to pain".

The company’s valuation history highlights why staying private aligns with its strategy. In just a few years, SpaceX’s valuation skyrocketed – from $180 billion in early 2024 to $350 billion by late 2024, and even reached $400 billion during share sale discussions in 2025. To put that into perspective, a $400 billion valuation places SpaceX above the combined worth of McDonald’s and Boeing. Such rapid growth could attract the intense scrutiny often faced by public companies, where the focus tends to shift toward consistent profitability rather than bold, speculative ventures. By staying private, SpaceX avoids these pressures and maintains its focus on long-term goals.

Private Funding Access

SpaceX has mastered the art of raising capital without entering public markets. Using Regulation D exemptions, the company secures investments from accredited investors, effectively treating private markets as its own version of a public market. To provide liquidity for employees and early backers, SpaceX also conducts stock buybacks twice a year. Its financial health is robust, with projections indicating revenue between $22 billion and $24 billion by 2026.

A key driver of this growth is its Starlink division, which has already deployed nearly 5,000 satellites and serves over 1.5 million subscribers across more than 50 countries. This combination of private investment and operational success allows SpaceX to fund its ambitious projects without the constraints of public market expectations.

Operational Flexibility

Remaining private gives SpaceX the freedom to take risks and pursue its ambitious vision. The company embraces a "fail fast" philosophy, treating early prototype failures as essential learning steps. This approach is a stark contrast to the cautious strategies often seen in public corporations or government programs. For example, a Falcon Heavy launch costs $90 million, a fraction of NASA’s $4 billion Space Launch System flight.

SpaceX’s ability to innovate quickly is evident in the development of the Raptor engine, which took just four years, and its frequent testing of Starship prototypes. Revenue from Starlink, estimated at $10 billion annually, is reinvested into high-stakes projects like Mars colonization. This operational flexibility, coupled with its financial independence, positions SpaceX to continue pushing the boundaries of space exploration.

sbb-itb-7e716c2

Why One Company’s Expected IPO Would Be a Disaster

2. Stripe

Stripe stands out as a prime example of how top pre-IPO companies leverage privacy to fuel growth while staying adaptable.

Regulatory Considerations

Founders Patrick and John Collison believe that staying private allows Stripe to remain in its "expand stage", prioritizing long-term infrastructure development over short-term profit goals. This approach shields the company from the quarterly scrutiny, activist demands, and trade secret exposure that come with going public.

And the results speak for themselves. Stripe achieved full-year profitability for the first time in 2024, processing an impressive $1.4 trillion in payment volume and generating an estimated $5.84 billion in revenue by 2025. When asked about their IPO plans, John Collison summed it up simply:

"Still not in any rush".

This level of control is rare. As Greg Martin, Partner at Liquid Stock, noted:

"Stripe has an unusual amount of control in the hands of their founders, who have shown no particular interest in being a public company".

This regulatory freedom aligns seamlessly with Stripe’s financial strategy.

Private Funding Access

Stripe has found ways to raise capital and provide liquidity without the need for an IPO. In February 2026, the company completed a secondary tender offer, valuing it at approximately $140 billion. This move allowed employees and early investors to cash out without the regulatory complexities of going public. Analyst Kyle Stanford from PitchBook highlighted this unique position:

"Stripe could delay an IPO more than most… [they] continue to raise from unlimited capital to stay private, though they are using that money to reduce the pressure staying private causes".

Stripe’s growth trajectory further underscores its independence from public markets. With an annual growth rate of 38% – nearly six times faster than PayPal‘s 10% – Stripe reinvests a significant portion of its earnings into research and development. These efforts focus on emerging technologies like AI and stablecoins. By 2025, these investments were already paying off: Hertz saw a 4% increase in authorization rates, and Forbes reported a 23% boost in subscription revenue.

This ability to secure private funding drives Stripe’s capacity for innovation.

Operational Flexibility

Remaining private gives Stripe the freedom to make bold moves without the pressure of meeting public shareholder expectations. For example, in late 2024, Stripe acquired Bridge, a stablecoin startup, and in February 2026, it launched "Open Issuance", a platform enabling businesses to create their own stablecoins. These ventures into the unpredictable world of crypto infrastructure might have faced heavy scrutiny from public market analysts focused solely on short-term returns.

The Collison brothers have made it clear why this flexibility is crucial:

"This ability [to reinvest in R&D] will prove particularly important in the coming years, as stablecoins, AI, and other forces reshape the landscape".

Stripe’s private status continues to be a key factor in its ability to innovate and adapt to a rapidly changing financial landscape.

3. Databricks

Databricks has emerged as a major force in the tech world, achieving massive growth while staying entirely in private markets. Its ability to navigate market fluctuations has been a key part of its strategy.

Market Volatility

CEO Ali Ghodsi highlighted several reasons for postponing a public offering, including concerns about election-year uncertainties, rising interest rates, and inflation:

"This year was an election year. We wanted to get some stability – people are worried about interest rates, inflation. … So we said look, it’s dumb to IPO this year, so we’re definitely going to wait."

By February 2026, Databricks reached a staggering $134 billion valuation and $5.4 billion in annualized revenue, reflecting a 65% year-over-year growth. Meanwhile, public competitors like Snowflake and Oracle saw their valuations drop by about 13%, largely due to concerns surrounding AI. Ghodsi suggested that if the market continues its current trajectory, Databricks might remain private indefinitely.

This cautious approach to market conditions underscores the importance of maintaining strong private funding to support its ambitious growth plans.

Private Funding Access

Databricks has successfully raised large amounts of capital while staying private. A $10 billion Series J funding round in late 2024 pushed its valuation to $62 billion. By early 2026, the company secured another $5 billion in equity funding and $2 billion in debt capacity. Notably, investor demand for the Series J round reached $19 billion, nearly double the amount Databricks ultimately accepted.

This influx of capital has enabled aggressive expansion. For instance, in July 2023, Databricks acquired MosaicML for $1.3 billion to strengthen its generative AI capabilities. A year later, in June 2024, it spent $2 billion to acquire Tabular, a data management startup generating approximately $1 million in annual recurring revenue.

Operational Flexibility

Remaining private allows Databricks to focus on long-term goals rather than short-term market pressures. As Ghodsi explained:

"I’m optimizing for the success of Databricks over the next decade or two, not optimizing for an IPO."

With steady funding in place, Databricks has been able to pursue bold strategies. For example, its internal "SnowMelt" initiative aimed to capture market share from Snowflake during times of stock price weakness. Similarly, the launch of the Lakebase database in 2026 was a direct challenge to established players like Oracle and SAP.

The company’s AI-focused products now bring in $1.4 billion in annualized revenue, and it has over 650 customers paying more than $1 million annually. These milestones highlight how staying private has given Databricks the freedom to innovate and grow without the constraints of public market expectations.

Benefits and Drawbacks of Staying Private

SpaceX vs Stripe vs Databricks: Private Company Comparison

For companies like SpaceX, Stripe, and Databricks, staying private comes with some clear advantages. One of the biggest perks is avoiding the rollercoaster of public markets. Private firms aren’t subject to the kind of short-term financial pressure that can send stock prices tumbling after a bad quarter. Luke Ward, Investment Manager at Baillie Gifford, put it this way:

"There’s an argument that some of these pioneering companies wouldn’t have been able to do what they have done if they had been on public markets and had those short-term pressures".

Another advantage is the access to an enormous pool of private capital – $2.6 trillion in uncommitted funds, to be exact. This cushion allows companies to delay going public. For example, Databricks raised $10 billion in December 2024, with investor demand nearly doubling what was available. With such strong funding options, private companies can focus on growth, keep control over their operations, and sidestep the influence of activist investors, quarterly earnings stress, and heavy regulatory scrutiny.

However, staying private isn’t without its challenges. Liquidity is a major issue. Employees and early investors often struggle to cash out, forcing companies to rely on secondary tender offers to provide some liquidity and help manage tax obligations tied to restricted stock units. On top of that, private valuations can lack transparency, and some experts warn they may not always reflect broader market trends.

Another downside is that retail investors are often left out. While institutional investors can ride the wave of early growth – as seen with SpaceX, now valued at around $400 billion – retail investors usually have to wait for the IPO. Even then, they might need to rely on complicated options like Special Purpose Vehicles (SPVs), which come with extra fees and hurdles. With the average time to IPO increasing from 7 years in 2015 to 11 years in 2025, retail investors miss out on a significant chunk of a company’s growth phase.

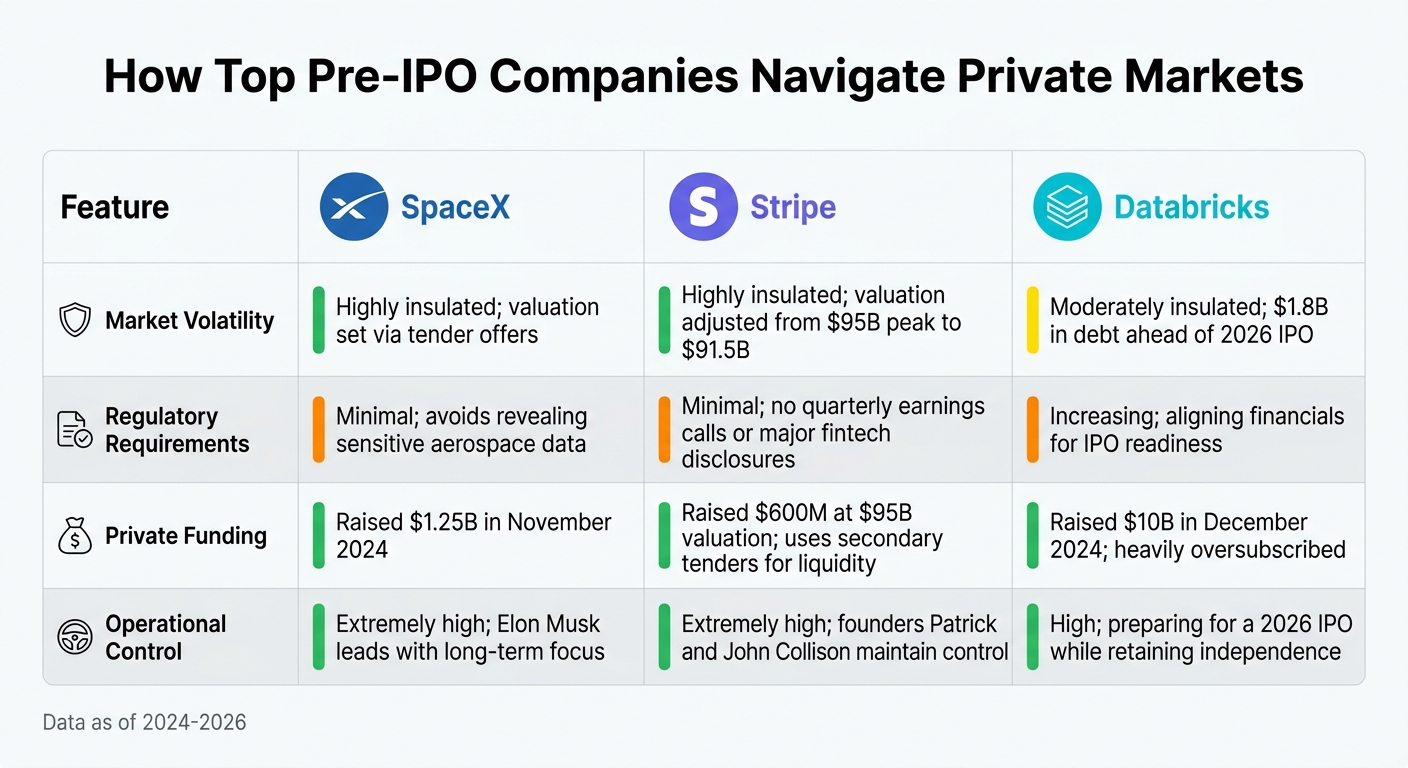

Here’s a breakdown of how these benefits and challenges play out for SpaceX, Stripe, and Databricks:

| Feature | SpaceX | Stripe | Databricks |

|---|---|---|---|

| Market Volatility | Highly insulated; valuation set via tender offers | Highly insulated; valuation adjusted from $95B peak to $91.5B | Moderately insulated; $1.8B in debt ahead of 2026 IPO |

| Regulatory Requirements | Minimal; avoids revealing sensitive aerospace data | Minimal; no quarterly earnings calls or major fintech disclosures | Increasing; aligning financials for IPO readiness |

| Private Funding | Raised $1.25B in November 2024 | Raised $600M at $95B valuation; uses secondary tenders for liquidity | Raised $10B in December 2024; heavily oversubscribed |

| Operational Control | Extremely high; Elon Musk leads with long-term focus | Extremely high; founders Patrick and John Collison maintain control | High; preparing for a 2026 IPO while retaining independence |

These dynamics highlight how private companies balance growth, control, and market readiness while navigating the trade-offs of staying out of the public eye.

Conclusion

SpaceX, Stripe, and Databricks highlight how staying private empowers companies to pursue bold, long-term strategies. Many top pre-IPO firms are extending their private status to focus on growth and innovation without the distractions of public market pressures. This shift, influenced by market volatility, regulatory advantages, and access to private funding, is reshaping the pre-IPO landscape. These companies can scale aggressively, maintaining control during their most critical growth phases.

For investors, this trend presents challenges. Retail investors often miss out on early-stage growth, as much of the value creation happens before companies go public. Take Databricks, for example – it achieved $4 billion in annual recurring revenue while still private. By the time such companies debut on the public market, their valuations are already mature. As Brian Nichols from Angel Squad put it, investors often find themselves "buying mature companies at mature valuations".

To capture earlier growth opportunities, investors need to look beyond traditional public markets. Options like angel investing, venture funds, or secondary market platforms can provide access to pre-IPO shares. However, these avenues require careful consideration. Special Purpose Vehicles (SPVs), for instance, come with complex fee structures and ownership layers that demand thorough due diligence. Additionally, tracking secondary market valuations can offer a more accurate picture of a company’s worth compared to older venture round estimates.

Private markets have become the epicenter of growth, with companies leveraging ample capital and strategic freedom to delay going public. For investors aiming to tap into these opportunities, understanding and navigating private markets is no longer just an option – it’s a necessity to remain competitive in today’s evolving investment world.

FAQs

What has changed to let companies raise huge funding without an IPO?

The growth of private capital has reshaped how companies secure funding, allowing them to raise billions without the need for public offerings. Companies like SpaceX and Databricks have tapped into this trend, attracting substantial investments through private funding rounds while sidestepping the challenges of IPOs.

At the same time, secondary markets provide a way for early investors and employees to cash out their shares, easing the pressure to go public. This approach gives companies the freedom to prioritize growth, pursue new ideas, and focus on long-term objectives without the constant scrutiny and unpredictability of public markets.

How do private companies give employees and early investors liquidity?

Private companies create liquidity through secondary market transactions, such as secondary sales and tender offers. These transactions give shareholders a chance to sell their shares before an IPO, providing an opportunity to turn potential gains into actual cash. Additionally, some companies run liquidity programs for employees holding RSUs, allowing them to sell shares ahead of a public offering. These methods let early stakeholders convert their equity into cash, often to cover personal expenses, while easing the urgency for the company to pursue a public listing.

How can individual investors get pre-IPO exposure responsibly?

Individual investors have options to responsibly explore pre-IPO opportunities, primarily through private secondary markets or specialized investment funds. While direct access is typically reserved for institutional and accredited investors, some private companies are starting to create pathways for smaller investors to get involved.

It’s crucial to keep a few things in mind: these investments come with higher risks, extended lock-up periods, and limited liquidity. To make informed decisions, take the time to conduct thorough research and stay updated on market trends. This approach can help you weigh potential returns against the inherent challenges of these investments.