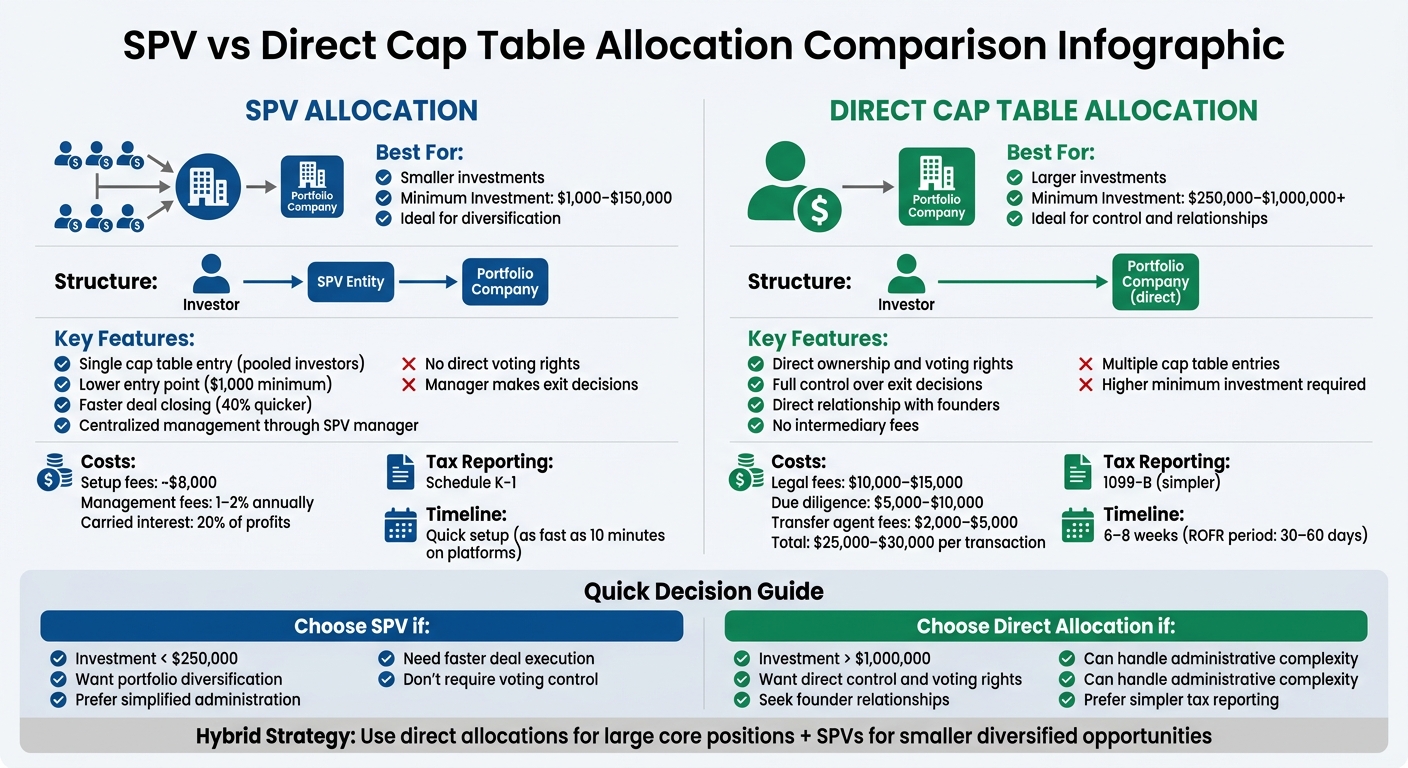

Choosing between SPVs and direct cap table allocations for pre-IPO investments depends on factors like investment size, control preferences, and administrative needs. Here’s a quick breakdown:

- SPVs (Special Purpose Vehicles): Ideal for smaller investments (e.g., $1,000–$150,000) or when minimizing cap table clutter is important. SPVs pool funds from multiple investors into a single entity, simplifying governance and reducing administrative complexity. However, they come with setup costs, management fees (1–2% annually), and carried interest (typically 20% of profits).

- Direct Cap Table Allocations: Best for larger investments ($250,000–$1 million+), offering direct ownership, voting rights, and control over exit decisions. While avoiding SPV fees, direct investments often involve higher upfront costs, legal fees, and potential delays due to corporate approvals.

Quick Comparison:

| Factor | SPV Allocation | Direct Cap Table Allocation |

|---|---|---|

| Minimum Investment | $1,000–$150,000 | $250,000–$1,000,000+ |

| Cap Table Impact | Single entry (pooled investors) | Multiple individual entries |

| Control | Decisions made by SPV manager | Full control over shares |

| Costs | Setup fees, management fees, carry | Higher legal and administrative fees |

| Tax Reporting | Schedule K-1 | 1099-B |

SPVs suit those seeking lower entry points and streamlined processes, while direct allocations work for investors prioritizing control and larger stakes. Pick the approach that aligns with your goals, budget, and administrative capacity.

SPV vs Direct Cap Table Allocation: Investment Structure Comparison

SPV sponsors & liquidity options on Fireside with a VC

sbb-itb-7e716c2

What is a Special Purpose Vehicle (SPV)?

A Special Purpose Vehicle (SPV) is a separate legal entity, often established as a Delaware LLC or Limited Partnership, created specifically to invest in a single company. It brings together funds from multiple investors to make one large, unified investment in a target startup. Instead of purchasing shares directly in a pre-IPO company, investors buy units in the SPV. The SPV then pools the capital and invests it as a single entity, making it appear as one shareholder on the startup’s cap table.

"SPVs went from an edge case to a core strategy. That is not a cosmetic change. It says something meaningful about how venture capital is now structured."

- Alon Kapen, Corporate Attorney, Farrell Fritz, P.C.

This structure has become a staple in late-stage venture capital. For example, platforms like Carta reported that the median SPV managed $2.17 million in assets in 2023, a significant jump from $1.18 million in 2016. Additionally, late-stage technology growth rounds accounted for over 60% of all U.S. venture capital by value in 2024.

Key Features of SPVs

- Pooled Capital: SPVs allow investors to combine their funds, enabling participation with smaller contributions – sometimes as low as $1,000 – in deals that usually require much larger minimum investments.

- Single Cap Table Entry: Instead of listing numerous individual investors, the startup records the SPV as a single shareholder. This simplifies cap table management and makes due diligence easier for institutional investors and IPO underwriters.

- Centralized Management: A "Syndicate Lead" or manager (often referred to as the General Partner) oversees negotiations, signs agreements, and acts as the primary point of contact with the startup, reducing administrative complexity.

- Liability Protection: The SPV acts as a legal buffer, shielding investors’ personal assets and other investments from potential risks tied to the SPV.

- Tax Treatment: As a pass-through entity, the SPV itself doesn’t pay corporate income tax. Instead, profits and losses are distributed to investors, who report them on their individual tax returns using Schedule K-1 forms.

These features make SPVs an efficient way to handle pre-IPO investments, offering streamlined processes for both investors and startups.

How SPVs Work in Pre-IPO Investments

Creating an SPV involves several steps. First, the manager defines the investment strategy and drafts an Operating Agreement that outlines the terms, including capital goals, fees, and profit-sharing arrangements. Many SPVs in the U.S. are formed in Delaware due to its favorable corporate laws and specialized Court of Chancery.

Once the SPV is legally established, the manager obtains an EIN and opens a dedicated bank account. Investors are then provided with a Private Placement Memorandum (PPM), which details the investment’s risks and terms. Each investor must also complete KYC/AML checks and verify their accreditation status to meet Regulation D requirements.

After collecting the funds, the SPV signs a subscription agreement, appearing as a single entity on the startup’s cap table. During the investment’s lifecycle, the manager monitors progress, shares updates, and handles tax filings. Upon exit – whether through an IPO or acquisition – proceeds are distributed according to a waterfall structure, with the manager typically earning 20% carried interest after investors recover their initial capital.

For example, in October 2024, OpenAI raised $6.6 billion at a $157 billion valuation using SPVs. This approach allowed it to consolidate participation from institutional investors, sovereign wealth funds, and corporate backers, significantly simplifying its cap table.

What is Direct Cap Table Allocation?

Direct cap table allocation is a method where investors hold shares in their own name directly on the company’s cap table, as opposed to pooling funds through an SPV (Special Purpose Vehicle). This setup gives investors direct control over their shares, including voting rights, exit decisions, and access to corporate communications. Essentially, there’s no intermediary entity – your shares are listed alongside those of founders and institutional investors like venture capital firms.

"Direct investment means you own shares directly, with no additional legal entity between you and the company. This directness simplifies everything from understanding your position to managing tax reporting to executing exit transactions." – Allied Venture Partners

This arrangement establishes a direct relationship between the investor and the company. Investors receive updates and financial statements straight from the company’s management rather than through an SPV manager.

However, this approach comes with a hurdle: accessibility. Many high-demand private companies set steep minimum investment amounts – typically between $250,000 and $1 million – to avoid overcrowding their cap tables. For this reason, direct investments are often considered practical only for commitments above $100,000, as transaction costs can be substantial.

Key Features of Direct Allocations

Here are some of the main aspects of direct cap table allocations:

- Individual Ownership: Investors sign their own legal agreements, such as Stock Purchase Agreements (SPA), Investor Rights Agreements, and Right of First Refusal (ROFR) waivers.

- Direct Information Rights: Shareholders often receive the same updates and financial reports as institutional investors, though the specifics depend on the class of shares purchased. Common stock buyers typically have fewer rights compared to those holding preferred stock.

- Simplified Tax Reporting: Direct ownership simplifies tax filings, as gains are reported using 1099-B forms.

- Control Over Exits: Investors decide when to sell their shares, whether after an IPO or during tender offers, without needing approval from third parties.

- Relationship Building: Direct ownership can open doors to follow-on investment opportunities, access to the founders’ network, and a better understanding of the company’s growth.

- High Closing Costs: Legal fees for negotiating agreements typically range from $10,000 to $15,000, while due diligence costs add another $5,000 to $10,000. Transfer agent fees can cost $2,000 to $5,000, bringing total transaction costs to $25,000–$30,000.

How Direct Allocations Work in Pre-IPO Investments

The process of direct allocation in pre-IPO investments follows a structured timeline, typically taking six to eight weeks, with ROFR requirements often extending this period.

- Negotiation: The buyer and seller agree on price and share quantity. The seller then submits a Stock Transfer Notice (STN) to the company’s general counsel to kick off the process.

- ROFR Period: A 30–60 day Right of First Refusal (ROFR) period begins, during which the company can repurchase the shares at the agreed price. If the company declines, existing investors can exercise their pro-rata rights to purchase the shares.

- Board Approval: The company’s board reviews the buyer’s qualifications and reasons for the purchase to ensure alignment with strategic goals and to avoid potential complications in future fundraising or corporate actions.

- Transfer Completion: Once the ROFR and board approval steps are complete, funds held in escrow are transferred to the seller. The company’s transfer agent then updates the cap table, finalizing the transaction. Using a neutral third-party escrow agent ensures security until the cap table update is confirmed.

It’s important for buyers of common stock to note that secondary market prices typically fall between the company’s 409A valuation and the pricing of preferred shares. This price difference reflects the varying rights and liquidation preferences associated with each class of shares. Direct cap table allocation offers clarity and control, standing in contrast to the pooled nature of SPV investments.

SPV vs Direct Cap Table: Key Differences

Understanding the practical differences between SPVs and direct cap table allocations is essential, especially when dealing with pre-IPO investments. These structural variations significantly impact how ownership is organized, administrative tasks are handled, and decisions are made.

With direct investment, the ownership structure is straightforward: Investor → Portfolio Company. SPVs, however, add an extra layer: Investor → SPV Entity → Portfolio Company. This additional layer affects everything from recording investor details to decision-making authority.

On a cap table, direct allocations list each investor individually, which can clutter the table. SPVs, on the other hand, consolidate all investors into a single entry. The AIN Editorial Team highlights this benefit:

"SPVs collapse multiple investors into a single line item on the cap table. This makes subsequent fundraising easier (VCs dislike messy cap tables), simplifies corporate governance, and reduces the company’s administrative overhead."

This streamlined approach reduces operational complexity. For example, direct allocations require companies to engage with each investor for corporate actions. SPVs simplify this by centralizing communication and decision-making through a single manager.

Control and flexibility also differ. Direct investors retain the right to vote and decide on exits independently. In contrast, SPV investors delegate these decisions to the SPV manager.

Comparison Table: SPV vs Direct Cap Table

| Factor | Direct Cap Table Allocation | SPV Allocation |

|---|---|---|

| Cap Table Impact | Multiple entries; can fragment ownership | Single entry; keeps records clean |

| Ownership Structure | Direct legal title to shares | Indirect; ownership of SPV interests |

| Investor Minimums | High (e.g., $25,000–$250,000) | Lower (e.g., $1,000–$10,000) |

| Governance Rights | Investors vote their own shares | Manager votes on behalf of all |

| Information Flow | Direct from company to investor | Mediated through SPV manager |

| Exit Decisions | Individual discretion | Manager-led; requires coordination |

| Additional Costs | Standard legal costs only | Setup fees, management fees (1–2% annually), and 20% carried interest |

| Tax Reporting | Simple 1099-B forms | Schedule K-1 for each vehicle |

Another key distinction is the speed of execution. SPV-backed deals tend to close faster – up to 40% quicker than direct investments in competitive markets. This speed was crucial in high-profile cases like OpenAI’s $6.6 billion raise in October 2024, where SPVs streamlined contributions from diverse investors into a single cap table entry.

These differences not only shape administrative processes but also influence how efficiently deals are executed and managed.

Advantages and Risks of SPVs

SPV Advantages

SPVs make managing cap tables and investor participation much easier. One standout advantage is cap table consolidation – instead of listing dozens of individual angel investors, the company records just one SPV entry. As Timothy Carter explains:

"A cap table showing twenty individuals from the seed round spooks [acquirers]; a cap table showing one SPV for that same block of equity looks tidy and predictable."

This streamlined structure appeals to institutional investors, especially during future funding rounds or acquisitions, where organized ownership is a priority.

SPVs also make investing more accessible by pooling smaller contributions. Instead of requiring the usual $25,000–$250,000 minimum for direct investments, SPVs allow participation with checks as small as $1,000–$10,000.

Another benefit is liability protection. By isolating investment risk within the SPV, any issues tied to one investment won’t affect the investor’s broader portfolio. Additionally, pooling capital often enables the SPV to negotiate better terms, like improved valuation caps or enhanced information rights.

SPVs can also speed up the investment process. In competitive markets, SPV-backed seed rounds can close up to 40% faster than traditional direct investments. This efficiency, combined with a clean ownership structure, simplifies governance and future fundraising.

While these advantages are compelling, SPVs aren’t without their challenges.

SPV Risks

On the downside, SPVs come with costs that can eat into returns. Setting one up typically costs around $8,000, with ongoing management fees of 1% to 2% annually, plus a carried interest fee of 20% on profits.

SPVs also shift governance dynamics. The SPV manager holds voting power and makes decisions about exits, which can feel limiting for investors who prefer direct control. Tax reporting becomes more complicated too – investors receive a Schedule K-1 for each SPV instead of the simpler 1099-B. This can make annual filings more cumbersome, especially for tax-exempt institutions dealing with Unrelated Business Taxable Income (UBTI) or international investors facing foreign tax obligations.

Another drawback is concentration risk. Unlike diversified venture funds, SPVs typically focus on a single asset. If that company fails, the entire investment is lost. Liquidity is another issue – SPV interests are generally locked up until a major exit event, like an IPO or acquisition.

Finally, regulatory compliance adds complexity. SPVs must follow SEC Regulation D, file Form D, and comply with state-level "Blue Sky" laws. Keeping the investor count below certain thresholds (often 99 participants) is essential to avoid triggering additional regulatory requirements. Poor administration or missed filings can lead to legal trouble and financial penalties.

Advantages and Risks of Direct Cap Table Allocations

Direct Allocation Advantages

Direct cap table allocations allow investors to hold shares directly in their name, giving them immediate ownership and control. This means they can sell shares, exercise voting rights, and stay updated on company developments without any intermediaries. Unlike investments made through SPVs (Special Purpose Vehicles), direct allocations remove intermediary fees and grant instant shareholder rights.

"Direct investment means you own shares directly, with no additional legal entity between you and the company. This directness simplifies everything from understanding your position to managing tax reporting." – John Malone, JD, Co-CEO of Anomaly CPA

One of the biggest perks? You sidestep the hefty fees associated with SPVs, such as the 1–2% annual management fees and the 20% carried interest. Tax reporting also becomes more straightforward.

Another benefit is the chance to build meaningful relationships. By engaging directly with founders and management teams, investors can open doors to future opportunities and strengthen industry connections.

While these advantages offer greater control and reduced costs, direct allocations aren’t without their challenges.

Direct Allocation Risks

One major hurdle for direct investments is the high cost of entry. Minimum investments typically start at $100,000 and can climb to $250,000, $500,000, or even $1 million. Add to that the closing costs, which can range from $25,000 to $30,000 per transaction, and the expenses quickly add up. These financial barriers explain why some investors shy away from direct allocations in favor of alternative options.

Cap table overcrowding is another significant issue. Under the JOBS Act, private companies must keep their "holders of record" below 2,000 to avoid mandatory SEC registration.

"A messy or inaccurate cap table can derail fundraising, erode investor confidence, and quietly chip away at founder ownership and control." – Yin Wu from Pulley

To avoid these complications, many late-stage companies encourage smaller investors to join SPVs, ensuring a cleaner and more manageable cap table.

The Right of First Refusal (ROFR) is another potential snag. It can delay deals by 30–90 days, as the company or existing investors may claim the deal after you’ve completed your due diligence. Additionally, secondary buyers often end up with common stock, which ranks below preferred shares in the liquidation waterfall. In moderate exit scenarios, these preferences can eat up more than 75% of the proceeds.

Direct allocations may offer control and reduced fees, but they come with costs, complexities, and risks that require careful consideration.

When to Choose SPV Over Direct Cap Table

Key Decision Factors

Deciding between an SPV (Special Purpose Vehicle) and a direct cap table allocation boils down to three main factors: investment size, number of investors, and administrative complexity.

A direct allocation is typically the better choice for investments of $1 million or more, where the cost of SPV management fees may outweigh the benefits. At this level, the ability to directly engage with company founders often becomes more valuable. On the flip side, SPVs are ideal for smaller investments, usually ranging from $1,000 to $150,000, especially when these amounts fall below a company’s minimum direct investment threshold. Many high-profile private companies set minimum investments between $250,000 and $1 million, making SPVs a practical way for smaller investors to pool resources and gain access.

SPVs also offer a practical solution for managing cap tables. By consolidating multiple investors into a single entity, SPVs help maintain a clean and manageable cap table. This is particularly beneficial for companies that want to avoid the administrative hassle of dealing with numerous individual investors.

Another advantage of SPVs is speed. Deals can close up to 40% faster with SPVs, as they streamline administrative processes by requiring only one SPV manager’s signature rather than multiple individual ones. However, family offices or investors with dedicated teams might lean toward direct allocations, as they provide greater control and oversight.

For a balanced approach, some investors use a combination strategy: direct allocations for large, core investments that secure stronger relationships and potential board observer rights, and SPVs for smaller, diversified positions across 15 to 20 additional opportunities. This hybrid model allows investors to maximize both control and diversification.

Considerations for Crypto Pre-IPO Allocations

Crypto-Specific Factors

Investing in crypto pre-IPO opportunities brings unique regulatory challenges that differ from traditional tech deals. For instance, crypto pre-IPO SPV (Special Purpose Vehicle) raises often rely on SEC Regulation D – specifically Rule 506(b) or 506(c), which requires accredited investor verification. Under Rule 506(c), compliance demands obtaining CPA letters or tax documents before funds are transferred.

SPVs must also comply with the Investment Company Act by limiting the number of beneficial owners to 100 under Section 3(c)(1), or by restricting participation to qualified purchasers. Additionally, all SPV participants are subject to KYC (Know Your Customer) and AML (Anti-Money Laundering) checks. Unlike direct allocations, where these checks are handled individually, SPVs must manage this process collectively.

Tokenization has added a new dimension to crypto pre-IPO allocations. A tokenized LP (Limited Partnership) structure digitizes investor allocations, offering potential secondary liquidity without changing the underlying cap table. A notable example is the EMpower Fund, launched in late 2025 by Web3 infrastructure company Lisk. This $15 million fund uses a tokenized LP structure to enable secondary trading, breaking away from the traditional venture capital model of decade-long lockups.

"A standout feature of the EMpower Fund is its tokenised LP structure, which digitises investor allocations to potentially enable secondary liquidity – an innovative shift from the traditional decade-long lockups typical in venture capital." – Startup Lagos

However, tokenization isn’t universally supported. For example, in December 2025, Matt Grimm, co-founder of Anduril Industries, clarified that the company’s bylaws prohibit forward contracts. This restriction prevents SPVs from taking possession of shares while the company remains private. Therefore, confirming transfer restrictions is critical before adopting a tokenized SPV structure. These crypto-specific factors require specialized expertise, making platforms like BeyondOTC essential for navigating these complexities.

How BeyondOTC Supports Pre-IPO Allocations

BeyondOTC simplifies the intricate process of crypto pre-IPO investments by connecting investors with carefully vetted opportunities and taking on the burden of regulatory compliance. The platform provides comprehensive support for SPV creation, including overseeing KYC/AML transactions – a key requirement for meeting SEC Regulation D standards.

For those interested in gaining exposure to DeFi protocols or late-stage crypto companies, BeyondOTC also offers services like TVL (Total Value Locked) funding advisory and access to secondary market transactions. By managing the administrative and legal hurdles, BeyondOTC allows investors to focus on evaluating deals rather than getting bogged down in paperwork.

Conclusion: Choosing the Right Allocation Strategy

There’s no one-size-fits-all solution here – your choice depends on factors like the size of your investment, your goals, and how much administrative bandwidth you have. For larger investments, particularly those over $1 million, direct allocation tends to work well. It offers control, flexibility, and avoids the typical 20% carried interest charged by SPV managers. On the other hand, SPVs are a better fit for smaller investments – usually under $250,000 – where diversification is key.

For family offices or institutional investors aiming to build focused, high-conviction positions, direct ownership provides the added benefit of controlling exits during secondary windows. Meanwhile, SPVs simplify the process for those looking to access rounds with high minimum investment thresholds. They consolidate tax reporting, KYC/AML compliance, and cap table management, which is a major plus for investors without the resources to manage multiple direct holdings.

"The goal isn’t choosing between direct investment and SPVs – it’s using both thoughtfully to construct portfolios that reflect your specific objectives, resources, and risk tolerances." – Monty

Timing and operational efficiency are just as important as strategy. By 2026, secondary market fundraising cycles have shrunk dramatically – from months to just weeks. In this fast-paced environment, being capital-ready can mean the difference between securing a deal and missing out. Pre-established SPV platforms, for instance, can be set up in as little as 10 minutes, while direct allocations often involve lengthy negotiations that could cause delays.

In the crypto pre-IPO space, regulatory hurdles add another layer of complexity. SEC Regulation D compliance and KYC/AML verification can make professional SPV management almost indispensable. Platforms like BeyondOTC help streamline these processes, allowing investors to focus on evaluating opportunities rather than getting bogged down by administrative tasks. Whether you go with SPVs, direct allocation, or a mix of both, make sure your strategy matches your capital size, control preferences, and ability to handle compliance requirements.

FAQs

How do I estimate whether SPV fees will outweigh the benefits for my check size?

To determine whether SPV fees are worth it for your investment size, you’ll need to weigh the total costs – like setup, compliance, and administrative fees – against the amount you plan to invest. For smaller investments, these fixed costs can eat into your returns, potentially making SPVs less practical. On the other hand, larger investments might justify the expense because of advantages like risk separation and simplified ownership. Always ensure that the fees won’t significantly reduce your expected returns before moving forward.

What rights do I lose by investing through an SPV instead of owning shares directly?

When you invest through an SPV, you hold membership interests in the SPV, not direct shares in the underlying company. This arrangement often means giving up voting rights and direct involvement in governance, as these responsibilities are handled by the SPV’s management team. Your rights are typically tied to your pro-rata share in the SPV, based on its specific terms. Additionally, this setup may come with limitations on transferability and liquidity, making it less flexible than owning shares directly.

What should I verify about transfer restrictions and ROFR before committing to a pre-IPO deal?

Before diving into a pre-IPO deal, it’s crucial to examine transfer restrictions and Right of First Refusal (ROFR) provisions. For instance, does the company or its shareholders hold a ROFR? If so, this might slow down or limit your ability to transfer shares. Also, take a close look at shareholder or operating agreements to identify any rules about selling or transferring shares. Knowing these details in advance can help you sidestep unexpected hurdles and make liquidity events more straightforward while adhering to the agreed terms.