Pre-IPO investments can offer high returns, but they come with risks like illiquidity and over-concentration. For high-net-worth individuals (HNWIs), setting clear concentration limits is essential to manage these risks while optimizing portfolio performance. Here’s what you need to know:

- Pre-IPO Risks: Illiquidity (5–10 years), company-specific risks, and tax inefficiencies.

- Concentration Limits: Limit single asset exposure to 10–20% of your portfolio to reduce risk.

- Allocation Strategies:

- Diversify across 10–15 companies in different sectors and regions.

- Use cash-flow modeling and stress tests to determine how much you can lock away.

- Adjust allocations based on liquidity needs and long-term goals.

- Portfolio Trends: HNWIs allocate 28–46% of their portfolios to private and alternative assets. Pre-IPO investments should align with your overall equity strategy.

- Risk Management Tools: Use financial models, scenario analysis, and stress testing to evaluate potential outcomes and avoid overexposure.

Unlocking the Secrets of Pre-IPO Investing | How the Wealthy Invest Before the IPO #financiallyfree

sbb-itb-7e716c2

What Are Concentration Limits in Pre-IPO Investments

Concentration limits set the maximum percentage of your portfolio that can be allocated to a single asset or asset class. Financial advisors often consider a position "concentrated" when a single asset exceeds 10%–20% of your total portfolio. In pre-IPO investing, these limits play a key role in managing how much capital is committed to illiquid assets, reducing the risk of overexposure.

The main goal of these limits is to mitigate idiosyncratic risk, which includes company-specific challenges like leadership changes, product failures, or regulatory issues. For instance, over a 40-year span, nearly 42% of individual stocks in the Russell 3000 experienced an absolute negative return, and concentrated positions underperformed the diversified Russell 3000 index 66% of the time.

"A concentrated stock position can be a sign of past success, but if left unmanaged, it can expose you to unnecessary risk."

– New England Private Wealth Advisors

In the pre-IPO world, concentration limits are equally important for managing illiquidity risks. Since pre-IPO assets often remain locked up for 5–10 years or longer, these limits ensure you retain enough liquid capital to handle unforeseen expenses, estate taxes, or other financial needs. They also guard against the denominator effect, where declining public market holdings make your illiquid private investments unintentionally dominate your portfolio.

How to Define Concentration Limits

Defining concentration limits starts with determining your maximum tolerance for illiquidity and setting minimum return expectations. Your illiquidity threshold reflects how much capital you can afford to lock away without jeopardizing cash flow for daily expenses, business obligations, or emergencies. Additionally, the minimum premium requirement ensures that private investments deliver the 2%–3% illiquidity premium typically associated with these assets.

To start, conduct cash-flow modeling and stress tests. For example, simulate scenarios like a 30% drop in revenue from a core holding or a freeze in capital markets. This helps you decide how much of your portfolio needs to stay liquid versus how much can be allocated to pre-IPO opportunities.

For diversification, experts recommend spreading your investments across 10–15 companies in different sectors, business models, and investment timelines. This approach reduces the risk of your strategy being derailed by a single stalled deal, such as one blocked by a Right of First Refusal (ROFR) or board restrictions.

"Private assets are characterised by illiquidity and have historically commanded a premium (excess return) that asset owners can capture if their portfolios can tolerate that illiquidity."

– Supriya Menon, Multi-Asset Strategist, Wellington Management

A formal Investment Policy Statement (IPS) is another key tool. It outlines your target concentration thresholds, liquidity reserves, and rebalancing strategies, helping you make rational decisions during market volatility. This is especially important for high-net-worth individuals (HNWIs), who may fall prey to overconfidence or familiarity bias in certain sectors. By sticking to these measures, you can better balance pre-IPO opportunities with overall portfolio stability.

Risks of Exceeding Concentration Limits

Exceeding concentration limits introduces several risks, particularly in the context of pre-IPO investments. These include greater exposure to company-specific risks, liquidity shortages, and tax inefficiencies.

If too much of your wealth is tied to a single company, events like lawsuits, product failures, or leadership changes could wipe out years of gains. Liquidity risk becomes critical with pre-IPO assets, as they remain locked for extended periods, leaving you unable to access funds for unexpected expenses or opportunities. This might force you to sell other assets at unfavorable prices.

| Risk Type | Description in Pre-IPO Context | Impact of Over-Concentration |

|---|---|---|

| Idiosyncratic Risk | Company-specific events (lawsuits, product failure) | Can erase years of gains overnight if the position is too large |

| Liquidity Risk | Inability to sell shares for 5–10+ years | Reduces access to capital for liabilities or other opportunities |

| Market Risk | General economic downturns | A downturn in one company can disproportionately affect total net worth |

| Tax Exposure | Capital gains triggered by selling large positions | High tax burden when rebalancing a concentrated portfolio |

The denominator effect is another issue. When public market holdings lose value, your illiquid pre-IPO investments could unintentionally take up a larger share of your portfolio, even if their actual value hasn’t changed.

"Concentration built the wealth. Discipline preserves it."

– Lumicre

Over-concentration also increases tax exposure. For example, selling a large pre-IPO position after a successful exit could trigger significant capital gains taxes. By spreading sales over multiple tax years, you could potentially reduce this burden. For HNWIs, failing to manage this efficiently could significantly cut into the proceeds available for reinvestment or spending.

How to Determine Optimal Pre-IPO Allocation Size

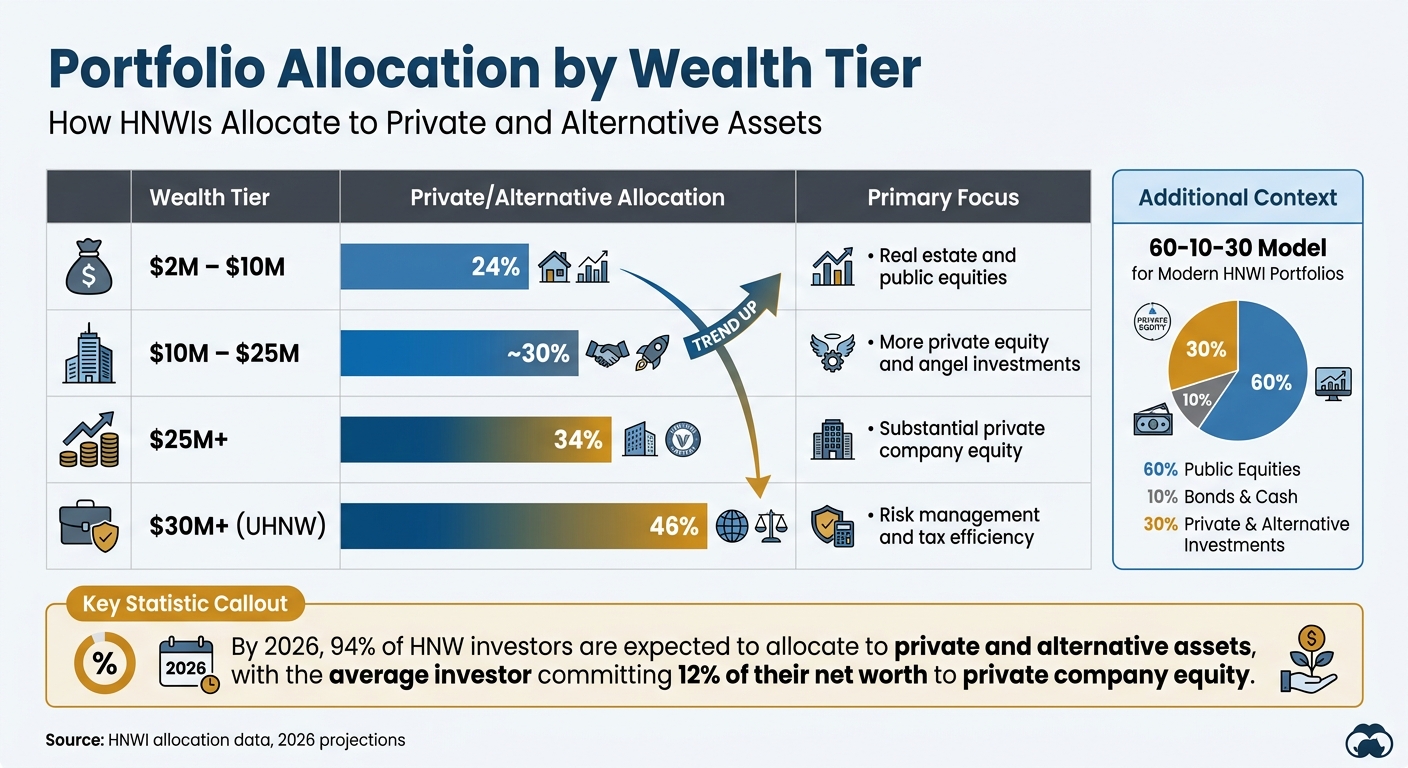

HNWI Portfolio Allocation to Private and Alternative Assets by Wealth Tier

Finding the right allocation size for pre-IPO investments is all about striking a balance between two limits: your upper bound (how much illiquidity you can handle) and your lower bound (the minimum return premium needed to meet your long-term goals). This builds on earlier ideas about concentration limits and liquidity needs. The upper bound represents the amount of money you can set aside for 5–10 years without risking your ability to handle expenses, emergencies, or business obligations. The lower bound ensures that your pre-IPO investments generate the 2%–3% illiquidity premium historically linked to private equity.

Your allocation size will also depend on how well you can source quality deals, identify promising companies, and invest capital wisely. Instead of treating pre-IPO investments as their own category within your Strategic Asset Allocation (SAA), think of them as an extension of your existing portfolio. This means evaluating the opportunity cost of funding these investments by reallocating from liquid assets like stocks or bonds.

"Asset owners should first decide what mix of broad market exposures is best aligned with their return objectives and risk constraints and then size public and private allocations within classifications such as equities, credit and real assets."

– Supriya Menon, Multi-Asset Portfolio Manager, Wellington Management

To make informed decisions, use cash-flow modeling and stress testing. Simulate scenarios like a 30% revenue drop or a capital markets freeze to figure out how much liquidity you need to hold versus how much you can commit to pre-IPO opportunities. Don’t forget to account for costs like management fees (2%) and carried interest (20%), which can reduce net returns by about 33% over four years.

Portfolio Allocation Breakdown by Asset Class

When deciding how pre-IPO investments fit into your portfolio, consider how they align with your broader asset allocation. Traditional 60/40 portfolios are shifting, especially for high-net-worth individuals (HNWIs). Many now follow a "60-10-30" model: 60% public equities, 10% bonds and cash, and 30% in private and alternative investments. By 2026, 94% of HNW investors are expected to allocate to private and alternative assets, with the average investor committing 12% of their net worth to private company equity, including pre-IPO positions.

Allocation percentages vary with wealth levels. For instance:

- Investors with $2–$10 million allocate around 24% to alternatives.

- Those with $25 million or more allocate 34%.

- Ultra-high-net-worth individuals ($30 million+) allocate 46% to alternatives, with the rest divided among public equities (29%), fixed income (15%), and cash (10%).

| Wealth Tier | Private/Alternative Allocation | Primary Focus |

|---|---|---|

| $2M – $10M | 24% | Real estate and public equities |

| $10M – $25M | ~30% | More private equity and angel investments |

| $25M+ | 34% | Substantial private company equity |

| $30M+ (UHNW) | 46% | Risk management and tax efficiency |

Pre-IPO investments should be part of your overall equity allocation. Keep in mind the denominator effect, where a drop in public market holdings can make illiquid pre-IPO positions take up a larger share of your portfolio – even if their value hasn’t changed. If market conditions shift, reassess your liquidity needs with additional stress tests.

Factors That Affect Allocation Decisions

Four main factors influence how much you should invest in pre-IPO opportunities: investment objectives, risk capacity, liquidity requirements, and investment timeline.

- Investment objectives: Your goals – whether growth, income, or capital preservation – shape your strategy. Growth-focused investors, like those in the FIRE movement, often lean toward public equities and private company equity for higher upside potential. Income-focused investors may prioritize real estate or private credit over high-growth pre-IPO positions. Ultra-high-net-worth individuals often focus on risk management, tax efficiency, and capital preservation, using alternative investments to hedge against volatility.

- Risk capacity: This reflects your ability to handle losses from pre-IPO investments, which are typically tied up for 5–10 years. You’ll need enough liquid reserves to cover unexpected expenses or market downturns. Stress testing can help you prepare for scenarios like a 30% drop in a core holding or a complete freeze in capital markets.

- Liquidity requirements: Liquidity is critical, especially since even after an IPO, shares often face a 90–180 day lock-up period. Consider upcoming expenses like estate taxes, business investments, or large purchases when deciding how much capital you can afford to lock away.

- Investment timeline: Your timeline matters. If you’ll need the money within three years, pre-IPO investments may not be a good fit. But if you’re investing for a decade or more, the 3% return premium historically tied to private equity can significantly enhance long-term performance – assuming you can handle the illiquidity and risks.

Diversification Strategies for Pre-IPO Allocations

When it comes to managing pre-IPO risks while aiming for growth, diversification plays a central role. Once you’ve determined the right allocation size, the next step is to spread your investments across a variety of opportunities. This helps reduce risk while maximizing potential returns. If you’re investing through venture capital or growth funds, achieving a broad mix of sectors and geographies is relatively straightforward. These funds inherently offer diversification by pooling investments. However, for those building a direct pre-IPO portfolio, careful planning is needed to avoid over-concentration while still spreading risk effectively. These strategies build on earlier allocation principles, offering added protection for your portfolio.

Diversifying Across Sectors and Industries

Investing across multiple sectors is a practical way to reduce concentration risk. With companies staying private longer, the kinds of opportunities that once existed in small-cap public markets have increasingly shifted into pre-IPO and late-stage venture capital spaces. This shift makes sector diversification even more important for investors.

"With companies staying private longer and the number of public companies shrinking, part of the opportunity set previously available in the small-cap listed market is now likely to be found in the pre-IPO or late-stage VC market."

– Supriya Menon, Multi-Asset Portfolio Manager, Wellington Management

One approach to sector diversification is using a systematic indexing strategy. This involves tracking a broad basket of late-stage private companies, ensuring that investments are selected transparently and not overly reliant on individual picks. Employing equal weighting and regular rebalancing can also prevent any single high-growth company from dominating your portfolio.

Another tactic is time diversification – spreading investments over several years. This reduces exposure to the risks of any single economic cycle or market peak, offering a more balanced approach to pre-IPO investing.

Diversifying Across Geographic Regions

Geographic diversification is another layer of protection for your investments. By spreading pre-IPO allocations across multiple regions, you can mitigate risks tied to specific countries or markets while tapping into global growth potential. While the U.S. remains a dominant player in the late-stage private market – with companies preparing for public listings collectively valued at over $3 trillion as of early 2026 – other regions also present valuable opportunities.

Regional risks often stem from differing regulatory environments. For example, U.S. investor eligibility is determined by income and net worth thresholds, which differ significantly from international standards. As of 2026, around 18.5% of U.S. households qualified under these criteria, compared to just 2% in the early 1980s. Such variations highlight the importance of thorough research before committing to regional investments.

When evaluating international opportunities, pay attention to a company’s Right of First Refusal (ROFR) history. This is crucial because many pre-IPO transactions are blocked by the company or existing investors. The likelihood of such restrictions varies depending on jurisdiction and company culture, making due diligence a must. Additionally, consider differences in local discounts and liquidity, as these factors can significantly affect the value and accessibility of your investments.

Risk Assessment Tools for Pre-IPO Investments

Once you’ve diversified your pre-IPO portfolio, the next step is to assess risks using structured financial models. These tools provide a quantitative foundation, complementing earlier strategies like setting concentration limits and managing liquidity. They help take the guesswork out of decision-making, enabling you to allocate capital with confidence and precision.

Using Financial Models for Risk Analysis

One essential tool is liquidation preference waterfall modeling, which outlines how exit proceeds are distributed across the capital structure – from preferred shareholders (often venture capitalists) to common shareholders (typically secondary buyers like you). Before committing funds, request a waterfall analysis to uncover any "toxic" liquidation preferences that could leave common shareholders empty-handed in moderate exit scenarios. Sensitivity analysis at various exit thresholds – say $300M, $500M, and $1B – can help you pinpoint when common stock offers meaningful returns.

For pricing, institutional investors often turn to models like Black-Scholes and Chaffe to calculate fair discounts, factoring in lock-up periods and potential value fluctuations. For example, with a risk-free rate around 4.5% in early 2026, late-stage companies nearing IPOs typically justify discounts of 12% to 18%. Meanwhile, growth-stage companies three years away may warrant steeper discounts of 30% to 40%. Be sure to adjust valuations from older funding rounds – anything over 18 months – by referencing the performance of comparable public market indices.

The synthetic alpha strategy is another approach, focusing on the gap between your purchase price (the secondary discount) and the last primary valuation. For instance, buying at a 30% discount creates a margin of safety, allowing for gains even if the next funding round’s valuation remains flat. When forecasting exits, factor in a 10% to 15% dilution buffer for shares issued to future investors or employees. Also, calculate your net internal rate of return (IRR) after accounting for typical fees (2% management fee, 20% carried interest) and potential tax impacts ranging from 20% to 35%.

These models provide a strong foundation for scenario planning, enabling a deeper understanding of potential outcomes.

Scenario Analysis and Stress Testing

Three-tier scenario planning is a must for evaluating risk exposure. Always consider a Base Case (exit at the last primary valuation), a Bull Case (valuation doubles), and a Bear Case (valuation drops by 30%). Plan for an average holding period of 3.2 years, plus an additional 0.5 years for the post-IPO lock-up period.

It’s also critical to differentiate between IPO and M&A outcomes in your models. M&A events in 2026 often result in lower multiples, and common stock proceeds from acquisitions may be discounted by as much as 54% due to the preference stack. When considering hedging strategies, calculate the "break-even drop" – the percentage decrease in stock value required to justify the hedge cost, which typically ranges from 5% to 12% in 2026.

"Never invest money in the secondary market that you might need within the next 24 months. While the ‘average’ exit is 3 years, individual companies can stall for a decade."

– Calcix Research Team

Finally, treat Right of First Refusal (ROFR) as a binary risk. This mechanism can block transactions entirely, so it’s crucial to account for it when planning your investments.

Accessing Pre-IPO Deals Through BeyondOTC

Once you’ve built your risk models and tested various scenarios, the next step is finding high-quality pre-IPO opportunities. The BeyondOTC platform offers a secure way to execute deals, connecting accredited investors with secondary market transactions that might otherwise be out of reach. This connection serves as the foundation for a compliant and secure investment process.

The process begins with validation and onboarding, which includes an interview to confirm your status as an accredited investor and to verify your investable assets. This step ensures adherence to securities regulations while protecting the integrity of the investment community. You’ll need to provide documentation of your net worth and investment experience during this stage.

After validation, it’s important to choose platforms that offer full transparency in underwriting. Many platforms provide access to critical data, such as detailed company financials, cap table structures, and ROFR (Right of First Refusal) history. This information is essential for making informed investment decisions.

Once you’re confident in the platform’s diligence, plan your investment allocation carefully. Decide how much of your portfolio to allocate to pre-IPO investments before committing any capital. For those new to private markets, starting with an allocation of 2% to 5% of net worth is common. This strategy helps maintain portfolio balance while still allowing room for potential growth. Keep in mind that direct purchases often come with minimum investment requirements, typically ranging from $25,000 to $30,000, so plan your commitments accordingly.

Secondary market transactions often clear at a 23% discount to preferred shares, which can create a strong opportunity for returns. However, it’s important to remember that common stock ranks below all preferred share classes in the liquidation waterfall. This makes thorough due diligence and careful discount modeling essential before proceeding with any transaction. A disciplined approach to evaluation and allocation can help protect your portfolio from the inherent risks of pre-IPO investments.

Case Studies: HNWI Pre-IPO Allocation Examples

Tech Sector Pre-IPO Investment Example

Northland Wealth Management’s investment in SpaceX highlights how institutional access and a disciplined, long-term approach can deliver impressive returns. In 2020, the firm facilitated a SpaceX investment for a client family at a $36 billion valuation through an institutional vehicle. They held this position for five years, capitalizing on SpaceX’s rapid growth. By the summer of 2025, they exited via the institutional secondary market, achieving a private valuation of roughly $800 billion.

This case brings several important lessons to light. First, access is critical. SpaceX doesn’t allow investments through retail platforms, making connections with venture capital networks or multi-family offices essential. Second, the five-year holding period emphasizes the need to account for illiquidity when determining position sizes. Lastly, the decision to exit before SpaceX’s anticipated 2026 IPO (projected at a $1.5 trillion valuation) demonstrates how secondary markets can offer liquidity opportunities ahead of a public listing.

"The SpaceX case illustrates several realities… First, access is everything. SpaceX does not accept investment from retail platforms."

– Arthur C. Salzer, CEO, Northland Wealth Management

This example highlights the importance of balancing concentrated investments with a diversified strategy to mitigate risk.

Diversified Pre-IPO Portfolio Example

Unlike concentrated strategies, diversified allocations can help manage both potential gains and losses. For example, D1 Capital Partners maintained a 45% concentration in SpaceX, far exceeding the typical 10–20% cap. This decision boosted their portfolio’s return to 39% in 2025. Without SpaceX, however, returns would have dropped to 18%.

But such concentration comes with notable risks. In 2022, the same strategy resulted in a 30% portfolio loss during a tech market downturn. This illustrates the "reverse denominator effect", a concept coined by The Maverick Club, which refers to how illiquidity in private markets prevents regular rebalancing, allowing successful investments to dominate portfolio composition unchecked.

"Private market concentration is a feature, not a bug – but only if your governance can withstand both the upside and the downside."

– The Maverick Club

For HNWIs looking for a more balanced approach, a diversified framework offers an alternative. Take retail investor Priya’s experience in 2025. After a 55% loss on a $150,000 single tech IPO investment, she reorganized her portfolio. She allocated 45% to five core tech leaders, 35% to 10–12 high-conviction satellite investments, 10% to experimental small caps, and kept 10% in cash. This strategy maintained growth potential while significantly reducing volatility, making it more manageable for long-term holding.

Conclusion: Key Takeaways for Pre-IPO Allocation Sizing

Pre-IPO allocation sizing is all about finding the right balance between seizing opportunities and maintaining financial discipline. Your upper limit should account for your ability to manage illiquidity – often requiring capital to be tied up for 5 to 10 years. On the other hand, your lower limit depends on whether you need the illiquidity premium that such investments typically offer. By 2026, the average high-net-worth individual (HNWI) is expected to allocate about 31% of their portfolio to private markets and alternatives, with this percentage increasing as wealth grows.

A practical way to approach this is by considering the opportunity-cost framework. Start by determining your long-term liquid equity exposure, and then use that as a foundation to size your pre-IPO allocations. These allocations are often funded by liquid alternatives that are most relevant to your portfolio. Keep in mind that fees can significantly impact returns, potentially reducing them by up to one-third. This method provides a structured approach to building a diversified pre-IPO strategy.

"Sizing target private asset exposure is a critical decision but is inherently different from determining target weights to stocks, bonds and other measurable asset classes."

– Supriya Menon, Multi-Asset Portfolio Manager, Wellington Management

Diversification is a key pillar of a successful pre-IPO allocation strategy. A well-rounded portfolio typically includes investments in 10 to 15 companies across various industries and vintage years. This approach helps protect against single-company failures and reduces the risk of overexposure during unfavorable IPO market conditions. Additionally, it’s important to stress test for the denominator effect – a scenario where a decline in public markets inadvertently inflates the proportion of illiquid assets in your portfolio.

Be prepared for challenges along the way. For instance, transaction delays are common, with the Right of First Refusal (ROFR) potentially blocking deals after negotiations are complete. This can leave your capital tied up in escrow for 6 to 8 weeks. To avoid surprises, confirm your accredited investor status early, model liquidation waterfalls to understand shareholder outcomes, and select the right investment vehicles. For smaller allocations (typically $10,000 to $50,000), SPVs are often a good fit, while direct purchases are more suitable for commitments over $100,000.

Ultimately, success in pre-IPO investing isn’t about chasing the next unicorn. It’s about sticking to a disciplined, repeatable process that aligns with your financial objectives. By focusing on thoughtful allocation, strategic diversification, and proactive planning, you can build a stable and rewarding pre-IPO investment portfolio.

FAQs

How do I choose a safe pre-IPO allocation if I’m unsure when I’ll need cash?

To make a smart and safe choice when it comes to pre-IPO allocations, start by evaluating your risk tolerance and how much liquidity you might need. It’s crucial to avoid putting too much into illiquid assets, so aim for diversification to spread out risk. At the same time, make sure you maintain enough liquid funds to cover any immediate cash needs.

Planning ahead is key. Align your investments with your financial timeline, striking a balance between the potential for growth and maintaining financial stability. And don’t just set it and forget it – regularly review your situation to ensure your allocation stays adaptable, supporting both your long-term goals and any short-term access to funds you might require.

What should I check in the cap table or liquidation waterfall before buying common shares?

Before buying common shares, take a close look at the liquidation waterfall. This outlines how funds are divided during a liquidity event, helping you gauge whether the risk fits your comfort level. Additionally, review the cap table to understand the ownership breakdown, the possibility of dilution, and the rights tied to different types of securities. These steps are key to making smarter investment choices and understanding how this decision could affect your overall portfolio.

How can I rebalance if the denominator effect makes my private holdings too large?

When private holdings start to take up a disproportionate share of your portfolio due to the denominator effect, it’s time to take action to bring things back into balance. Start by evaluating the value of these holdings compared to your total assets, ensuring they align with your overall risk tolerance.

Set clear thresholds for how much of your portfolio private holdings should represent. Regularly monitor your exposure and run stress tests to see how your portfolio might perform under different scenarios. If your private holdings exceed these limits, you can take steps like:

- Gradually reducing your position in these assets.

- Selling a portion to free up liquidity.

- Reinvesting the proceeds into more liquid investments to diversify and lower concentration risks.

These strategies can help you maintain a balanced portfolio and keep your risk levels in check.