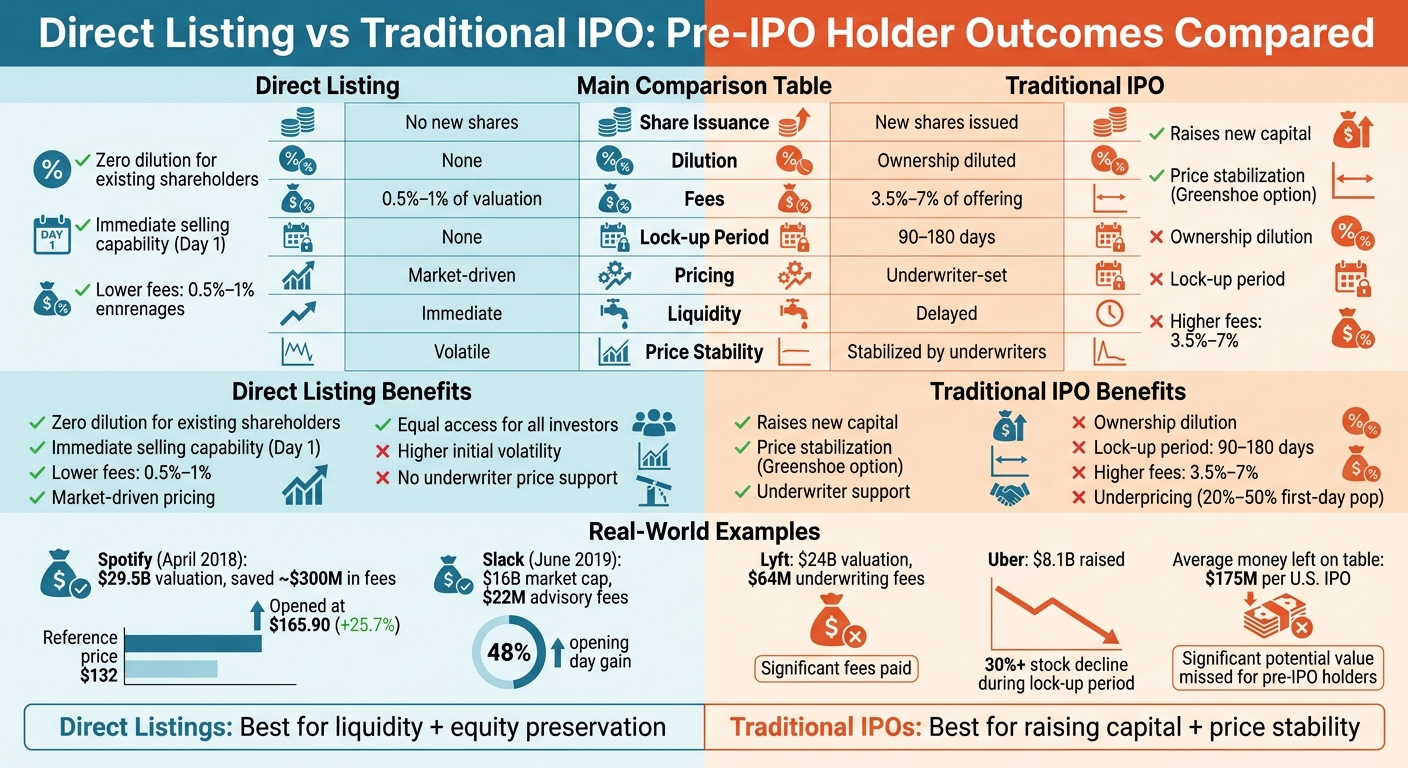

If you’re wondering which method benefits pre-IPO shareholders more, here’s the quick takeaway:

- Direct Listings: No new shares are issued, meaning no dilution for existing shareholders. Pre-IPO holders can sell their shares immediately without lock-up periods, and fees are much lower (0.5%–1%). However, there’s no underwriter support, so stock prices can be more volatile early on.

- Traditional IPOs: Companies issue new shares to raise capital, which dilutes existing ownership. Pre-IPO shareholders usually face a 90–180 day lock-up period before selling. Underwriters ensure price stability but charge higher fees (3.5%–7%) and often underprice shares, leading to missed value for early investors.

Key Points to Consider:

- Equity Value: Direct listings avoid dilution, while IPOs reduce ownership percentages due to new share issuance.

- Liquidity: Direct listings offer immediate liquidity; IPOs delay selling with lock-up agreements.

- Control: Direct listings rely on market pricing, giving shareholders more flexibility. IPOs involve underwriters, who set prices and allocate shares.

Quick Comparison:

| Feature | Direct Listing | Traditional IPO |

|---|---|---|

| Share Issuance | No new shares | New shares issued |

| Dilution | None | Ownership diluted |

| Fees | 0.5%–1% of valuation | 3.5%–7% of offering |

| Lock-up Period | None | 90–180 days |

| Pricing | Market-driven | Underwriter-set |

| Liquidity | Immediate | Delayed |

| Price Stability | Volatile | Stabilized by underwriters |

Conclusion: Direct listings are ideal for companies prioritizing liquidity and preserving shareholder equity, while IPOs suit those needing to raise significant funds with added price stability.

Direct Listing vs Traditional IPO: Complete Comparison for Pre-IPO Shareholders

Corporate Finance Explained | IPOs, Direct Listings, and SPACs: How Companies Go Public

sbb-itb-7e716c2

Pre-IPO Holder Equity Value Comparison

The financial outcomes for pre-IPO shareholders can vary significantly depending on the public listing method chosen. A major factor here is dilution.

Equity Value in Direct Listings

Direct listings allow existing shareholders to sell their shares without issuing new ones, meaning there’s no dilution for pre-IPO holders. This approach also comes with much lower fees. Instead of hefty underwriting fees of 3.5%–7.0%, direct listings typically involve advisory fees of only 0.5%–1%.

Take Spotify’s direct listing in April 2018 as an example. The company hit a $29.5 billion valuation without issuing new shares. By skipping underwriters, Spotify saved an estimated $300 million in fees compared to a traditional IPO of the same size. The market set Spotify’s opening price at $165.90, well above the $132.00 reference price, ensuring that all value went to existing shareholders.

"For companies with enough capital and just seeking to get listed, the direct listing route avoids the issuance of new shares (and dilution to existing shareholders)." – Wall Street Prep

Now, let’s look at how traditional IPOs impact pre-IPO equity value.

Equity Value in Traditional IPOs

In a traditional IPO, companies raise capital by creating and selling new shares, which reduces the ownership percentage of pre-IPO shareholders. On top of that, underwriting fees – ranging from 3.5% to 7.0% – further cut into the value retained by the company and its investors.

Underwriters also set the offer price through roadshows and book-building. This often leads to underpricing, creating a "pop" in the stock price on the first trading day. Historically, IPO pops averaged around 20%, but for high-growth tech companies, they’ve recently climbed to about 50%. While this first-day surge may seem appealing, it often means pre-IPO shareholders miss out on potential gains.

For a clear comparison, consider Slack’s direct listing versus Lyft’s traditional IPO. Slack went public in June 2019 with a $16 billion market cap and paid only $22 million in advisory fees. Around the same time, Lyft used a traditional IPO, reached a $24 billion valuation, and incurred $64 million in underwriting fees.

The table below highlights these key differences.

Equity Value Comparison Table

| Feature | Traditional IPO | Direct Listing |

|---|---|---|

| Share Issuance | New shares created and sold | Only existing shares sold |

| Dilution Impact | High – ownership percentage reduced | Zero – no new shares issued |

| Underwriting Fees | 3.5% – 7.0% of offering | Minimal advisory fees (0.5% – 1%) |

| Pricing Method | Set by underwriters via roadshows | Market-driven via opening auction |

| Typical Underpricing | 20% – 50% first-day pop | Market determines the true value |

The choice between these two methods has a direct and substantial impact on the financial outcomes for pre-IPO investors.

Liquidity Outcomes for Pre-IPO Holders

When it comes to liquidity, the timing and structure of access differ significantly between direct listings and traditional IPOs. Direct listings allow for immediate trading, while traditional IPOs typically enforce lock-up periods that delay selling.

Liquidity in Direct Listings

Direct listings stand out because they provide immediate liquidity. From the very first day of trading, founders, employees, and early investors can sell their shares without restrictions, as there are no lock-up periods in place.

Take Slack’s direct listing in June 2019 as an example. Shareholders were free to sell their shares immediately, and the stock opened 48% higher than its reference price.

"In a direct listing, company insiders are not constrained from selling or distributing their pre-IPO shares by a lock-up agreement. They are free to sell their shares whenever and for whatever amount they want." – Ran Ben-Tzur and James Evans, Partners, Fenwick

However, this freedom can lead to potential downsides. The absence of lock-up agreements sometimes results in a rush of selling, which may cause heightened volatility, particularly during the first 20 trading days.

Liquidity in Traditional IPOs

In contrast, traditional IPOs come with structured delays. Insiders are typically bound by a lock-up agreement lasting 90 to 180 days, during which they cannot sell their shares.

A notable example is Uber’s IPO in May 2019. While the company raised $8.1 billion, insiders were unable to sell their shares during the lock-up period. By the time they could sell, the stock had dropped by more than 30%, leaving many insiders with less favorable exit opportunities.

Lock-up periods do serve a purpose, though. They help underwriters manage stock prices by using tools like the Greenshoe option. However, they also delay liquidity and expose pre-IPO holders to potential price declines during the waiting period.

Liquidity Comparison Table

| Liquidity Factor | Traditional IPO | Direct Listing |

|---|---|---|

| Lock-up Period | Standard 90–180 days | None |

| Selling Eligibility | Only after lock-up expiration | Immediately upon listing |

| Market Access | Initial shares allocated to institutional investors | Equal access for all buyers and sellers from the start |

| Price Stabilization | Underwriter price support (Greenshoe option) | No price support; subject to market volatility |

| Share Supply | New shares created by the company | Existing shares sold by current holders |

These differences in liquidity play a crucial role in helping pre-IPO holders decide which public listing method aligns best with their goals and needs.

Control and Governance Differences

When it comes to pricing and decision-making, direct listings and traditional IPOs operate in completely different ways. In a direct listing, pre-IPO shareholders retain more control since there are no underwriters setting terms. Instead, the market determines the price through supply and demand on the first trading day, giving existing shareholders the flexibility to decide when and how to sell their shares.

Control in Direct Listings

In a direct listing, pricing is entirely market-driven. Companies may provide a reference price to guide initial trading, but the final opening price depends on buyer and seller activity. For instance, Spotify set a reference price of $132 per share during its April 2018 direct listing, but the stock opened at $165.90 – a 25.7% jump. Similarly, Coinbase‘s direct listing in April 2021 featured a reference price of $250 per share, yet it opened at $381, reflecting a 52% increase.

Without underwriters involved, there’s no preferential treatment for institutional investors. Everyone gets equal access from the start, and pre-IPO shareholders can decide independently when to sell. However, this freedom comes with a trade-off: there are no stabilization tools like the greenshoe option, which means the stock may experience greater price swings in its early trading days.

In comparison, traditional IPOs place much of this control in the hands of underwriters.

Control in Traditional IPOs

Traditional IPOs take a more structured approach, with underwriters playing a central role. These financial intermediaries set the initial offering price based on market research, roadshows, and interest from institutional investors.

"In an IPO, new shares of the company are created and are underwritten by an intermediary. The underwriter works closely with the company throughout the IPO process, including deciding the initial offer price of the shares." – Investopedia

Underwriters also decide how shares are allocated, often prioritizing institutional investors. Additionally, pre-IPO shareholders face mandatory lock-up periods, typically lasting 90 to 180 days, during which they cannot sell their shares. While underwriters may offer price support through tools like the greenshoe option, these benefits come at a cost – underwriting fees typically range from 3.5% to 7.0%. Moreover, issuing new shares to raise capital dilutes existing shareholders’ ownership and voting power.

Control Comparison Table

| Control Factor | Traditional IPO | Direct Listing |

|---|---|---|

| Pricing Mechanism | Set by underwriters based on institutional demand | Determined by market supply and demand |

| Share Allocation | Managed by underwriters, favoring institutional investors | Open market allocation with no preferential access |

| Underwriter Involvement | Central role in marketing and risk management | Limited involvement; companies may use financial advisors |

| Lock-up Restrictions | Mandatory 90–180 day lock-up period for insiders | Generally no lock-up period for immediate liquidity |

| Shareholder Dilution | New shares are issued, diluting existing ownership | No new shares are issued, preserving ownership |

| Price Stabilization | Greenshoe option available for price support | Lacks stabilization, leading to higher initial volatility |

| Transaction Costs | Underwriting fees of 3.5%–7.0% | Lower costs, typically around 0.5%–1.0% |

Case Studies: Direct Listings vs Traditional IPOs

The examples below highlight how direct listings and traditional IPOs impact pre-IPO shareholders, focusing on equity value, liquidity, and control.

Direct Listing Examples: Spotify and Slack

Spotify Technology S.A. made history in April 2018 as the first major company to choose a direct listing on the NYSE. On its first trading day, Spotify reached a market capitalization of $26.5 billion, closing at $149.01 per share. The NYSE had set a reference price of $132.00, but strong market demand drove the opening price up to $165.90 – a 25.7% jump that directly benefited existing shareholders.

"By forgoing the underwritten offering process, Spotify was able to accomplish its goal of providing liquidity without imposing IPO-style lock-up agreements upon listing." – Marc D. Jaffe, Greg Rodgers, and Horacio Gutierrez

Spotify’s direct listing allowed early investors and employees to sell their shares immediately, with 30,526,500 shares traded out of 178,112,840 outstanding shares on the first day. The company spent about $35 million in advisory fees for its $29 billion listing, a fraction of the cost of traditional underwriting. Importantly, Spotify issued no new shares, avoiding any dilution for existing shareholders.

Slack Technologies followed Spotify’s lead in June 2019, listing directly to provide liquidity for its shareholders. This move brought 118.4 million registered shares and 164.9 million unregistered shares to market simultaneously, bypassing lock-up periods and dilution.

These examples showcase how direct listings provide immediate liquidity and preserve shareholder equity, offering a stark contrast to the traditional IPO process.

Traditional IPO Examples: Uber and Airbnb

Traditional IPOs, on the other hand, come with different priorities and trade-offs. Uber and Airbnb both opted for traditional IPOs to raise large amounts of growth capital. This required issuing new shares, which diluted the ownership stakes of pre-IPO shareholders.

The costs associated with traditional IPOs can be significant. For instance, Snap spent $85 million on underwriting fees, while Lyft paid $64 million. These fees typically range between 3.5% and 7.0% of the capital raised. Additionally, underwriters often price IPO shares below their potential market value to ensure a strong first-day performance for institutional investors. In 2017, the average first-day return for traditional IPOs was 11.8%, and the average "money left on the table" in U.S. IPOs was estimated at $175 million – a loss of value that could have gone to existing shareholders.

While Uber and Airbnb raised billions to fund their expansion, pre-IPO shareholders faced diluted ownership, delayed liquidity, and missed opportunities to benefit from initial price gains, which instead went to new investors.

Conclusion: Which Method Benefits Pre-IPO Holders More?

For pre-IPO holders focused on quick access to liquidity and maintaining equity, direct listings offer clear perks. They skip the standard lock-up periods, provide same-day liquidity, and avoid dilution since no new shares are issued. Plus, the fees are typically lower compared to the higher costs associated with traditional underwriting.

On the other hand, traditional IPOs are better suited for companies that need a large injection of growth capital. Pre-IPO holders choosing this route must weigh the benefit of price stability offered by underwriters against the trade-offs. Tools like "greenshoe" options and stabilization mechanisms help manage volatility during the initial trading period, typically the first 20 days. However, these benefits come at a price: first-day stock surges (or "pops") often average 40%–50%, shifting significant value to new investors.

For those in the crypto and tech sectors, direct listings can be particularly appealing when the company already has strong brand recognition and doesn’t need to raise new funds. Companies like Spotify and Slack showcase how direct listings help retain shareholder value by avoiding underpricing. That said, investors must be ready to handle more price volatility without the safety net of underwriter support.

FAQs

When does a direct listing make more sense than an IPO for early shareholders?

A direct listing works well for companies whose early shareholders want liquidity without the need to raise extra funds or issue new shares. This method allows founders, employees, and early investors to sell their shares directly to the public, skipping underwriters entirely. It’s a popular choice for larger, profitable, and well-funded companies looking to provide liquidity while steering clear of the expenses and intricate process tied to a traditional IPO.

How can pre-IPO holders manage risk if there’s no lock-up in a direct listing?

Pre-IPO shareholders can navigate risk during a direct listing by taking advantage of market-driven price discovery and planning their sales carefully. Since there’s no lock-up period, they have the flexibility to sell shares incrementally, aligning with favorable market conditions and valuation trends.

Another useful approach is conducting secondary sales prior to the listing. This not only helps assess market demand but also establishes a reference price, which can minimize the chance of sharp price declines. At the same time, this strategy benefits from the added transparency and liquidity a direct listing provides.

What should pre-IPO investors watch for during the first few trading days after listing?

Investors planning to engage in pre-IPO opportunities should keep a close eye on stock price volatility and fluctuations in trading volume during the first few days of trading. These elements often highlight how the market is reacting and provide insights into liquidity conditions. In direct listings, these movements tend to be more noticeable than in traditional IPOs. By analyzing these trends, investors can better gauge market sentiment and determine how easily shares can be bought or sold during this crucial phase.