Cap table diligence is critical when buying pre-IPO shares. A poorly managed cap table can signal deeper issues like hidden dilution, undocumented equity promises, or missing legal documents, all of which can erode your returns. Key red flags include:

- Conflicting cap tables: Multiple versions often hide convertible instruments or errors.

- Undocumented equity promises: Verbal agreements can lead to disputes and tax penalties.

- Outdated valuations: Old 409A valuations distort ownership and create tax liabilities.

- Excessive dilution: Founders with low ownership may lack incentives to drive growth.

- Missing legal documents: Discrepancies between the cap table and legal records can invalidate shares.

To protect your investment, always verify the cap table against legal documents, confirm fully diluted share counts, and ensure proper vesting schedules. Use tools like Carta or Pulley for accuracy, and consider professional audits for complex cases.

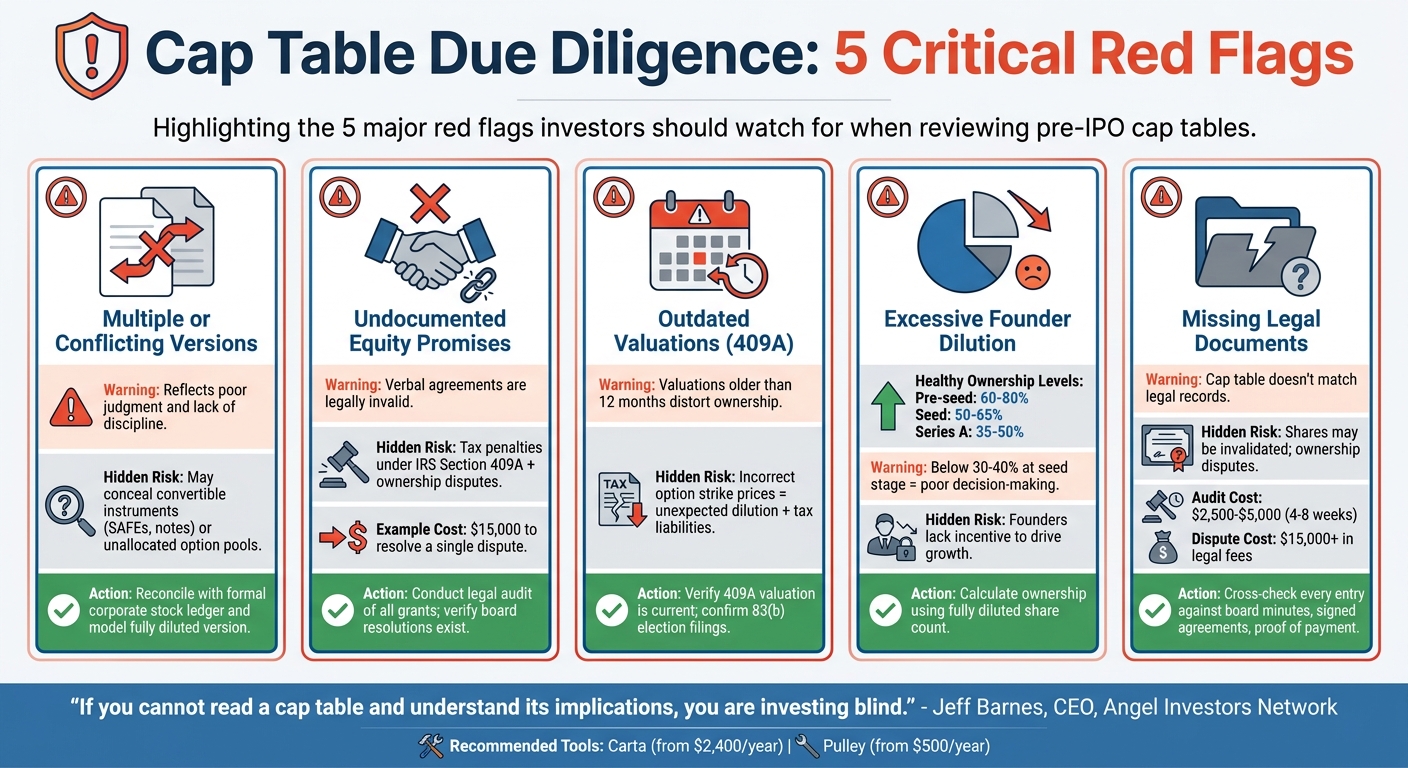

5 Critical Red Flags in Pre-IPO Cap Table Due Diligence

Cap Table Fundamentals Every Founder Must Know Before Raising Money

sbb-itb-7e716c2

Red Flags to Watch for in Cap Tables

When reviewing a cap table before buying pre-IPO shares, there are certain warning signs that should make you pause. These issues often point to deeper problems in how a company handles its equity, which can directly affect your potential returns. Let’s break down some of the most common red flags to watch out for.

Multiple or Conflicting Cap Table Versions

If a company presents more than one version of its cap table, it’s a big warning sign. This isn’t just an administrative hiccup – it reflects poor judgment and lack of discipline from the founders. These inconsistencies make it hard to accurately predict your potential returns. Often, the problem comes from using manual spreadsheets, which lack version history and are prone to errors that usually surface weeks into due diligence.

Conflicting cap tables can also hide convertible instruments like SAFEs, notes, or unallocated option pools, which may dilute your ownership unexpectedly when they convert.

To safeguard your investment, insist on reconciling the cap table with the formal corporate stock ledger (the legal record of issued shares). Cross-check it against signed Stock Purchase Agreements, Articles of Incorporation, and board-approved option grant schedules. Always model a "fully diluted" version of the cap table, which accounts for all SAFEs, notes, and warrants as if they’ve already converted.

Another area to scrutinize is undocumented equity promises.

Undocumented Equity Promises and Phantom Grants

Verbal agreements for equity or informal promises can lead to serious problems. Without proper approval from the board or stockholders, these grants might be legally invalid and could trigger tax penalties under IRS Section 409A – for both the recipient and the company.

Here’s an example: A founder verbally promised an early sales hire "about 0.5%" equity. Years later, the employee claimed the promise was for 1%. With no written agreement, the dispute ended up costing the company $15,000 to resolve.

"Verbal equity agreements are unenforceable, unmemorable, and create disputes. By year three, when someone remembers an old promise differently than you do, you have a problem." – Lech Kaniuk, Angel Investor

These undocumented promises can lead to "cap table shock", where investors find their ownership percentages are lower than expected once informal agreements are accounted for – often right before a liquidity event.

To avoid surprises, conduct a legal audit of all previous grants. Create a master list of everyone with an equity claim – founders, employees, and advisors – and verify that each claim has proper documentation. Request copies of board resolutions, stock certificates, and purchase agreements. Any gap between the cap table and legal documents is a major red flag.

Next, let’s look at valuation and option pricing issues.

Outdated Valuations and Option Pricing Problems

Using old valuations or incorrect option pricing can create tax problems and misrepresent ownership percentages. Under IRS Section 409A, companies must get an independent valuation to determine the Fair Market Value (FMV) of their stock before issuing options. If the strike price is set too low, employees could face immediate tax liabilities, and the company might incur penalties.

Outdated valuations also distort the cap table. If a company hasn’t updated its 409A valuation in over a year, the option strike prices might not reflect current market conditions, leading to unexpected dilution when options are exercised.

To protect yourself, confirm that all option grants include 83(b) election filings (submitted to the IRS within 30 days of the grant). Ask for the company’s most recent 409A valuation report and verify it’s no more than 12 months old. Make sure the option strike prices on the cap table match the FMV stated in the report.

Be wary of tactics like the "pool shuffle", where investors require a new option pool to be created on a pre-money basis. This can dilute founders more than expected if only the current cap table is considered. Always ask how the option pool was sized and when it was last updated.

Valuation errors can impact your returns, but so can poor equity management and excessive dilution.

Excessive Dilution and Poor Equity Management

If founders’ equity has been excessively diluted, it’s a clear red flag. This often points to poor decision-making or desperate financing terms. As Jeff Barnes, CEO of Angel Investors Network, puts it:

"If the founding team has been diluted below 30-40% by the seed stage, something has gone wrong – either too much capital was raised at unfavorable terms, or too much equity was given away."

Healthy founder ownership levels typically range from 60–80% at pre-seed, 50–65% at seed, and 35–50% at Series A. Anything below these levels might indicate the founders lack the incentives to push through the tough early stages.

Another issue is "advisor bloat." Giving away more than 1% equity to multiple advisors can clutter the cap table and cause headaches during fundraising or exits. Active advisors usually receive 0.15–0.5% equity.

For secondary market buyers, there’s also the risk of a "dilution bomb." Unlike public shareholders, who see quarterly dilution disclosures, secondary investors may only learn about years of stock-based compensation (SBC) when the company files its S-1 for an IPO. This can lead to sudden, unexpected dilution.

| Aspect | Public Shareholder | Secondary Market (Pre-IPO) Shareholder |

|---|---|---|

| Transparency | High: Dilution reported quarterly | Very low: Limited visibility |

| Dilution Event | Gradual and priced in over time | Sudden "bomb" at S-1 filing |

| Liquidity | High: Can sell instantly | Low: Locked in until IPO or exit |

To assess dilution risks, calculate ownership based on the fully diluted share count, including all options, warrants, and convertible instruments. Also, review the option pool size – it should align with an 18–24 month hiring plan, not an arbitrary percentage. At the seed stage, a typical employee option pool is 10–15% of fully diluted shares.

Finally, let’s address missing legal documents.

Missing Legal Documents and Record Discrepancies

If the cap table doesn’t match the supporting legal documents, it creates serious risks. The cap table should be the definitive record of ownership, but it’s only reliable if backed by proper documentation.

Discrepancies between the cap table and legal records can invalidate shares or lead to ownership disputes.

"When you start hitting 15, 20 or more entities in your cap table, that’s when it starts getting messy and can be a red flag to some investors." – Jonny Seaman, Investor Partnerships Manager, SeedLegals

Request a full legal audit to cross-check the cap table against executed documents. Every entry should have a paper trail: board minutes approving the grant, signed agreements, and proof of payment (if applicable). Missing vesting schedules are especially problematic – they leave "dead equity" on the cap table even if key employees leave.

Resolving these gaps can be costly and time-consuming. A professional cap table audit usually costs $2,500–$5,000 and takes 4–8 weeks. Fixing a single equity dispute caused by missing documentation can run upwards of $15,000 in legal fees.

How to Verify Cap Tables Properly

Once you’ve identified potential issues, the next step is to thoroughly verify the cap table. A detailed review can help you avoid expensive surprises later. Here’s how to handle this process step by step.

Reconciling Records and Reviewing Documents

Start by gathering all the documentation related to equity in one place. This includes key documents like articles of incorporation, shareholder agreements, stock option plans, board resolutions, and transaction records. Every entry in the cap table should be backed by a signed document approved by the board and shareholders.

Next, confirm the fully diluted share count. This means accounting for all options, warrants, and convertible instruments, while also identifying any equity held by inactive advisors or former co-founders that no longer contributes to the company. This ensures you have a clear view of your ownership percentage after factoring in all dilution events.

It’s also crucial to check that the company’s 409A valuation has been updated within the past year. This ensures that option strike prices align with current market values. For early-stage companies, a 409A valuation typically costs between $2,000 and $5,000.

| Document Type | What to Verify |

|---|---|

| Articles of Incorporation | Rights, preferences, and privileges of each share class |

| Stock Purchase Agreements | Terms of all previous funding rounds |

| Option Plan Documents | Current grant schedules and total authorized shares |

| Convertible Instruments | Valuation caps, discount rates, and interest for SAFEs/Notes |

| Vesting Schedules | Cliff dates and acceleration provisions for key personnel |

| 409A Valuation | Most recent independent appraisal of common stock fair market value |

Once you’ve reconciled these documents, it’s time to bring in experts for a deeper review.

Working with Legal and Financial Advisors

After verifying your records, collaborate with legal and financial advisors to uncover any overlooked discrepancies. While cap table management software can help streamline this process, complex cases often require human expertise. Advisors are especially useful when dealing with international holdings or intricate equity structures. They can also clarify issues like undocumented grants or non-contributing equity identified during your review.

A full cap table audit generally takes 4–8 weeks and costs between $2,000 and $5,000. This investment can save you time and money by speeding up fundraising by 4 to 6 weeks and cutting legal fees during due diligence by over $10,000.

"A clean cap table accelerates fundraising by 4-6 weeks and reduces legal fees during due diligence by €10,000+." – Lech Kaniuk, Angel Investor and Founder

Legal counsel can also "certify" your cap table, providing a formal statement of accuracy that reassures institutional investors. They can reconcile the cap table with the formal stock ledger (a legal requirement for Delaware C-Corporations) and model complex scenarios to show how SAFEs or convertible notes might dilute ownership during a priced round.

If your company has more than 50 shareholders or complex international holdings, consider hiring a cap table specialist immediately. Addressing problems early can prevent costs from escalating significantly over time.

Using Cap Table Management Software

Cap table management software offers automated tools for calculations, scenario modeling, and compliance tracking – capabilities that go beyond what spreadsheets can handle. This software works alongside manual reviews to provide real-time validation and continuous monitoring.

The software should automate record validation by cross-checking equity entries against legal documents and flagging any inconsistencies. It should also support scenario modeling, allowing you to run "what-if" projections for future funding rounds, create waterfall charts for exit payouts, and evaluate the impact of SAFE or convertible note conversions.

Other important features include audit trails that preserve historical records, integration with legal and financial systems, and automated tracking of 409A valuations. Additionally, the platform should allow investors to securely access and monitor their holdings in real time.

Popular platforms for managing cap tables before an IPO include Carta (starting at about $2,400 per year for Series A+ companies) and Pulley (starting at about $500 per year for seed-stage startups). While these tools require an upfront investment, they can save over $10,000 in legal fees during due diligence and speed up fundraising by 4 to 6 weeks.

"A company managing its equity on a spreadsheet in 2026 is not taking governance seriously." – Jeff Barnes, CEO, Angel Investors Network

How to Fix Common Cap Table Problems

Once you spot red flags in your cap table, it’s crucial to address them quickly to protect your investment. With a structured approach and proper record-keeping, most issues can be resolved effectively.

Setting Up Standard Vesting Schedules

Inconsistent or missing vesting schedules can shake investor confidence and lead to "dead equity." To avoid this, establish clear vesting schedules. A common structure is a 4-year vesting schedule with a 1-year cliff for founders and early hires. For active advisors, a 2-year vesting schedule with a 1-year cliff is more appropriate.

Here’s how the 4-year schedule works: no shares vest until the first anniversary, at which point 25% of the shares vest. After that, the remaining shares vest monthly over the next three years. For advisors actively contributing to the company, equity should typically range between 0.15% and 0.5%.

"The vesting schedule is the founder’s ‘skin in the game’ signal. Investors want to see that founders are committed to a multi-year process." – Lech Kaniuk, Founder of iTaxi

If vesting wasn’t set up at the start, you can fix this by retrofitting vesting agreements through restricted stock agreements, crediting founders for time already served. For example, in 2012, iTaxi discovered during due diligence that its four co-founders had different vesting schedules. To address this, the company standardized all founders to a 4-year schedule with a 1-year cliff, starting from the founding date. This move reassured investors and resolved concerns.

Don’t forget to file an 83(b) election within 30 days of granting restricted stock. This prevents unexpected tax liabilities.

Once vesting schedules are in place, the next step is to clean up your cap table.

Cleaning Up Cap Tables and Auditing Documents

A messy cap table can lead to confusion and missed opportunities. Follow these five steps to clean things up:

- Audit: Collect all equity-related documents to establish an accurate baseline.

- Resolve: Formalize any verbal or undocumented equity arrangements with board-approved, signed agreements.

- Consolidate: Remove equity for inactive advisors and adjust your option pool to match a hiring plan for the next 18–24 months.

- Standardize: Ensure all vesting schedules and SAFE terms are consistent across the board.

- Certify: Have your corporate attorney review and certify the updated cap table.

A professional audit of your cap table usually takes 4 to 8 weeks and costs between $2,000 and $5,000. Start this process at least 90 days before a fundraising round to ensure discrepancies are resolved before due diligence begins.

By maintaining a clear process, you’ll avoid scrambling to fix issues later.

Keeping Cap Tables Accurate Through Regular Reviews

Prevent future cap table problems by conducting regular reviews. Assign a single person – such as your CFO, fractional CFO, or head of legal – to manage and update the cap table immediately after any equity event.

Reconcile the cap table with legal documents on a quarterly basis. During active fundraising periods, review it even more frequently. Studies show that about 40% of companies audited by financial advisors have unsigned option agreements.

"Cap table hygiene is a month-1 activity, not a month-24 activity." – Lech Kaniuk, Founder and Angel Investor

Before your first priced funding round, consider upgrading from spreadsheets to professional cap table management software. Tools like Carta (starting at $3,000 per year) or Pulley (starting at $1,000 per year) can help. These platforms ensure data accuracy, automate calculations, and link transactions to their supporting documents.

Regular audits and the right tools keep your cap table clean, eliminate "dead equity", and reduce the risk of costly mistakes like forced repricing or losing investor trust.

Conclusion

After examining the major warning signs and solutions, one thing becomes clear: cap table diligence is absolutely essential.

A cap table is much more than just a spreadsheet – it’s a reflection of a company’s financial foundation. Disorganized records, missing documentation, or problems like dead equity and anti-dilution clauses don’t just highlight administrative slip-ups. They also reveal poor decision-making by founders and a lack of transparency, both of which can jeopardize pre-IPO investments.

"If you cannot read a cap table and understand its implications, you are investing blind." – Jeff Barnes, CEO, Angel Investors Network

Thorough diligence helps uncover issues like hidden dilution from uncapped SAFEs, ensures equity is properly approved by the board, and confirms timely tax filings. Expert advisors play a crucial role in avoiding costly mistakes by modeling exit waterfalls, clarifying the differences between participating and non-participating preferred shares, and spotting blocking rights that could delay an IPO. These strategies, discussed earlier, emphasize why rigorous cap table checks are so critical. Tools like Carta and Pulley, combined with regular audits, can keep records accurate and ready for scrutiny, making last-minute chaos before major transactions a thing of the past.

As one expert put it:

"A poorly managed capitalization table isn’t just an administrative oversight – it’s a liability that can derail negotiations, inflate legal costs, and in worst-case scenarios, kill deals entirely." – Ishwar Gogineni, Product Lead, Commenda

FAQs

What is a fully diluted cap table?

A fully diluted cap table includes all outstanding shares as well as any shares that might be issued through options, warrants, convertible securities, or other rights. It reflects the company’s total potential ownership if every one of these securities were exercised or converted.

How can SAFEs or notes dilute me later?

When you issue SAFEs (Simple Agreements for Future Equity) or convertible notes, you’re essentially agreeing to issue shares in the future. This can dilute your ownership. The tricky part? If you have multiple SAFEs or notes converting during a funding round, their varying valuation caps or terms can lead to more dilution than you might expect. This means founders could see their overall stake shrink more than anticipated.

What documents should match the cap table?

The cap table needs to match critical ownership records to ensure everything checks out during due diligence. These records include equity documents, stock ownership details, and data on options or warrants. Keeping these documents aligned helps ensure clarity and prevents any inconsistencies.