Investing in private companies before an IPO comes with limited transparency. Unlike public companies, private firms aren’t required to disclose financials or risks unless investors secure information rights. These rights, typically outlined in an Investors’ Rights Agreement (IRA), grant access to critical data like financial statements, cap tables, and performance metrics.

Key Points:

- Why Information Rights Matter: Private companies lack mandatory disclosure rules. Without these rights, investors risk being uninformed about financial health or operational issues.

- What They Include: Access to financial reports (often annual, quarterly, or monthly), board materials, budgets, and key performance indicators (KPIs).

- Who Gets Them: Reserved for "Major Investors" meeting thresholds like $1M–$2M investments or 5%-10% equity ownership.

- Expiration: Rights terminate before an IPO or when SEC reporting begins.

- Challenges: Enforcement depends on investor-company relationships, and excessive demands can strain resources.

In short, information rights help investors monitor their investments effectively and make informed decisions, especially in private markets where transparency is limited.

Why Investors Require Information Rights in Pre-IPO Deals

Investors need information rights because private companies, unlike public ones, are not obligated to disclose financial details to shareholders who aren’t on the board. As PipelineRoad puts it:

In public markets, investors receive standardized disclosures through SEC filings. In private markets, there is no regulatory requirement for companies to share financial data with shareholders who do not sit on the board. Information rights fill that gap.

This lack of required transparency makes these contractual rights critical for investors to maintain oversight. Without them, shareholders might find themselves in the dark about whether a company is thriving or burning through cash at an alarming rate. Early-stage companies can experience significant financial shifts within just a quarter, so having regular updates – not just yearly summaries – helps investors spot problems early. This kind of insight is key not only for tracking growth but also for ensuring accurate portfolio valuations.

For venture capital and private equity funds, such rights are essential for calculating Net Asset Value (NAV) and providing accurate reports to Limited Partners. General Partners depend on up-to-date financial data, including quarterly reports and cap tables, to give stakeholders reliable valuations. Without this access, ensuring transparency and accountability becomes nearly impossible.

Additionally, these rights help reduce valuation uncertainties in private markets. Whether it’s for secondary transactions or deciding on pro-rata participation in future funding rounds, investors need timely performance metrics. Access to board-approved budgets and monthly management reports gives them a clearer picture of how the company is performing.

Typically, information rights are reserved for "Major Investors" – those who invest a minimum of $1 million to $2 million during the Series Seed stage or hold 5% to 10% of the preferred stock. As companies grow and raise more capital, these thresholds usually increase, ensuring only significant stakeholders receive these updates. This approach also helps companies manage their reporting obligations without overwhelming their resources.

sbb-itb-7e716c2

Core Information Rights in Pre-IPO Agreements

When experienced investors negotiate pre-IPO agreements, they focus on securing specific contractual rights that provide a clear view of a company’s performance and governance. These rights are typically outlined in an Investors’ Rights Agreement (IRA). Since private companies are not required to disclose detailed financial information, these agreements become critical for ensuring transparency. The complexity of these contracts highlights the importance of clearly defined rights, which often include access to financial statements, board-related materials, operational metrics, and more.

Financial Statement Access

Regular access to financial updates is essential for investors to evaluate a company’s financial health. Commonly, annual financial statements are provided within 90 to 120 days after the fiscal year ends, quarterly reports within 45 days after each quarter, and monthly income statements within 30 days if requested.

For early-stage companies, unaudited statements are the norm to reduce administrative strain. However, later-stage companies are usually required to provide audited reports certified by an independent accounting firm. Many agreements also include a flexible clause obligating the company to share additional financial data upon reasonable request, ensuring investors have the information they need.

Board Meeting Minutes and Observer Rights

Board observer rights allow investors to gain insight into a company’s strategy without taking on the fiduciary responsibilities of a director. Observers are typically granted access to board meetings and related materials, such as meeting notices, agendas, and minutes, under strict confidentiality requirements.

These rights are often reserved for lead investors or those who meet a minimum ownership threshold – commonly between $1 million and $2 million at the Series Seed stage. Observers may also receive annual budgets and business plans before the fiscal year begins, giving them a glimpse into management’s expectations and strategic direction.

Performance Metrics and KPIs

Beyond standard financial statements, sophisticated investors often request access to operational metrics and KPIs that provide a deeper understanding of the company’s performance. For example:

- A SaaS company might report monthly recurring revenue (MRR), customer acquisition cost (CAC), and churn rate.

- A consumer marketplace might focus on gross merchandise value (GMV), take rate, and user retention.

These metrics act as early indicators of the company’s financial health and help investors gauge whether growth projections are on track. As startup lawyer Ryan Roberts explains:

Information rights should give your investors confidence, not consume your calendar.

To strike a balance between transparency and efficiency, companies should establish a reliable reporting framework that includes essentials like cash on hand, burn rate, runway, and revenue. Additionally, investors often require mechanisms to verify these reports, such as inspection rights and access to the cap table.

Inspection Rights and Cap Table Access

Inspection rights give major investors the ability to verify reported information by visiting company premises, reviewing books and records, and discussing financial matters with company officers during normal business hours. These provisions often include safeguards to prevent the disclosure of sensitive information to competitors or anything that could jeopardize attorney-client privilege.

Equally important is consistent access to the capitalization table (cap table), which allows investors to track their exact equity ownership and monitor potential dilution. The cap table must provide enough detail for investors to calculate their equity percentage accurately.

How to Negotiate and Secure Information Rights

To secure robust information rights, it’s essential to approach negotiations strategically. One effective approach is qualifying as a "Major Investor", which often grants full access to reporting. With Series A pre-money valuations in 2026 ranging between $35 million and $45 million, investors should be ready to commit significant capital to meet these thresholds.

Information rights are often tied to pro-rata rights, as investors argue that access to performance data is critical for evaluating follow-on investment opportunities. In late-stage deals, tiered access structures are another strategy: larger investors might receive monthly reports, while smaller stakeholders are limited to quarterly updates.

Term Sheet Inclusion and Sample Clauses

The groundwork for information rights is laid out in the term sheet and formalized through the Investors’ Rights Agreement (IRA). Using the National Venture Capital Association (NVCA) model IRA as a reference point offers a reliable, market-standard framework. A typical reporting package should include financial statement timelines, as discussed earlier in this article.

In addition to standard financials, it’s wise to include a "catch-all" clause requiring the company to provide "additional information relating to the financial condition, business, prospects, or corporate affairs as reasonably requested". To address founder concerns, clearly define what is "reasonable" and implement strong confidentiality measures. For later-stage deals, investors should also require that financial statements be certified by the CFO to ensure accuracy. When negotiating special privileges like observer rights, a side letter can be a useful tool to secure these benefits without triggering similar requests from other investors.

Working with Advisors and Agencies

Engaging experienced legal counsel and advisors is crucial for navigating the complexities of information rights. As the MoFo ScaleUp Team notes, advisors can "assist in identifying market standards according to a company’s stage of development, limit any unnecessary costs in complying with these obligations, and ensure that appropriate confidentiality protections are in place". Their expertise can also help avoid the so-called "CFO-by-investor" trap, where ad-hoc analytics requests overwhelm company resources and strain relationships.

BeyondOTC, for example, provides access to pre-IPO opportunities while guiding investors through the intricacies of information rights for each deal. Leveraging established networks and stage-specific insights, advisors can negotiate realistic reporting schedules and confidentiality safeguards, especially when sensitive trade secrets or customer data are involved. They also help define "Major Investor" thresholds in a way that protects investor rights, even in the face of future dilution. While information rights are rarely litigated, they are typically enforced through board discussions and leverage in future financing rounds. Securing these rights is essential, but investors must also remain mindful of their limitations, which will be explored in the following section.

Risks and Limitations of Information Rights

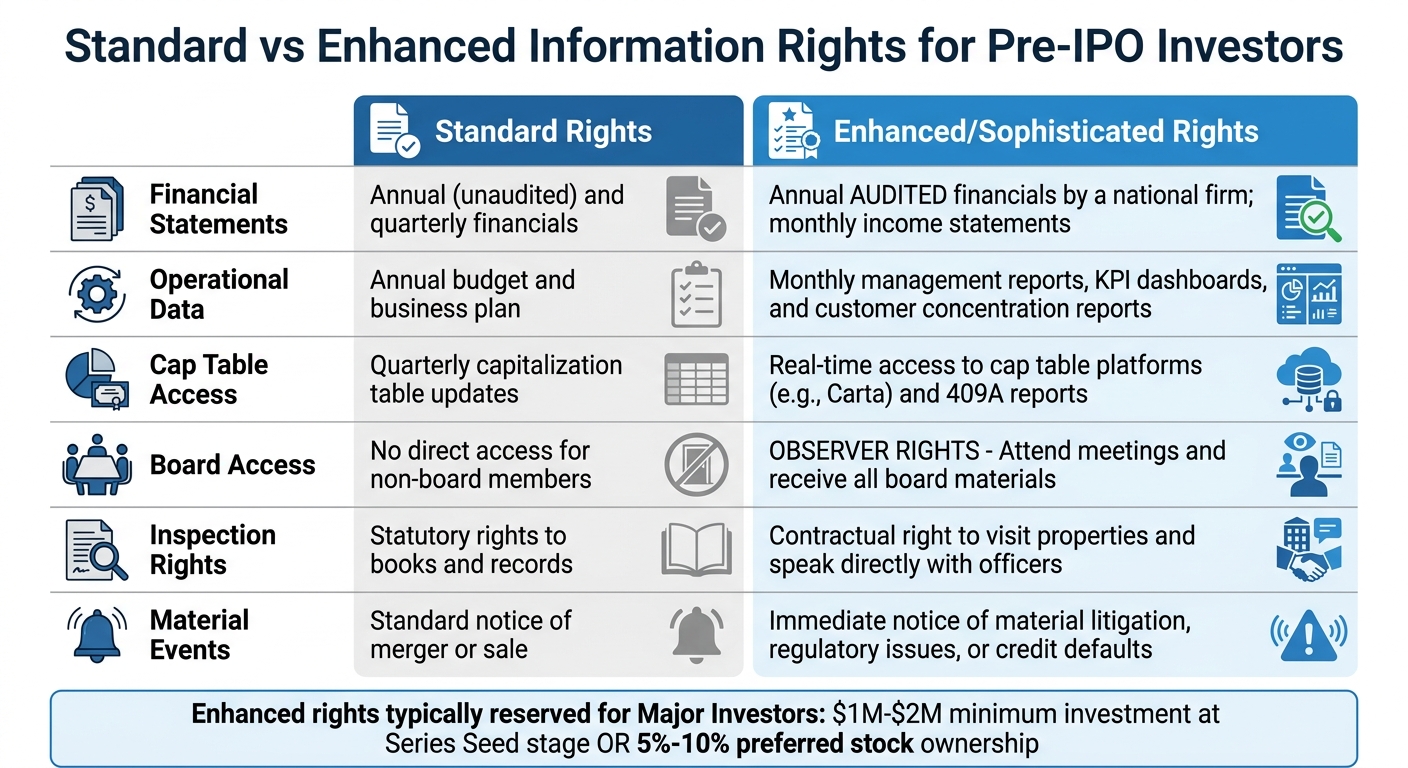

Standard vs Enhanced Information Rights for Pre-IPO Investors

While strong information rights can give investors valuable insights, it’s important to understand their boundaries, especially in pre-IPO deals. One key limitation is automatic termination: these rights automatically end just before a company’s IPO or when it becomes subject to SEC reporting requirements. This happens regardless of how much you’ve invested or how solid your contract might be.

Another major challenge is enforcement. These rights are rarely enforced through legal action; instead, they rely on the dynamics between investors and the company’s leadership. If a company delays reports or provides incomplete data, your main leverage is during future funding rounds, not in court. This makes your relationship with the management team just as important as the legal terms of your agreement. Beyond enforcement issues, regulatory rules also impose limits on these rights.

Regulatory constraints can restrict information rights in certain situations. For example, foreign investors with observer rights may trigger a Committee on Foreign Investment in the United States (CFIUS) review, as these rights could conflict with the "passive investment" status needed for some regulatory exemptions. Companies may also withhold information to protect attorney-client privilege, safeguard trade secrets, or avoid conflicts of interest. As the MoFo ScaleUp Team explains:

The company has the right to withhold any information… to protect the company’s attorney-client privilege with its counsel and to prevent disclosure of trade secrets.

There’s also the issue of administrative burden. Granting too many information rights can overwhelm a company’s management, creating what’s sometimes called a "CFO-by-investor" trap. This happens when the finance team spends so much time meeting investors’ demands that it distracts from running the business. This "reporting creep" can strain relationships and even lower the quality of the information provided, as rushed reports often lack depth or accuracy.

Standard vs. Enhanced Rights Comparison

Understanding the difference between basic and more advanced information rights can help you negotiate smarter and set realistic expectations for what you’ll receive:

| Feature | Standard Rights | Enhanced/Sophisticated Rights |

|---|---|---|

| Financial Statements | Annual (unaudited) and quarterly financials | Annual audited financials by a national firm; monthly income statements |

| Operational Data | Annual budget and business plan | Monthly management reports, KPI dashboards, and customer concentration reports |

| Cap Table Access | Quarterly capitalization table updates | Real-time access to cap table platforms (e.g., Carta) and 409A reports |

| Board Access | No direct access for non-board members | Observer Rights: Attend meetings and receive all board materials |

| Inspection Rights | Statutory rights to books and records | Contractual right to visit properties and speak directly with officers |

| Material Events | Standard notice of merger or sale | Immediate notice of material litigation, regulatory issues, or credit defaults |

Enhanced rights are typically reserved for major investors, often with thresholds between $1 million and $2 million at the Series Seed stage. Ownership requirements usually range from 5% to 10% of preferred stock. If you don’t meet these thresholds, you’ll likely have access only to standard rights – and even those might be limited if the company is dealing with administrative challenges.

Information Rights in Crypto Pre-IPO Investments with BeyondOTC

Cryptocurrency pre-IPO investments often come with a lack of standardized regulatory disclosures. Since Web3 startups and DeFi protocols typically bypass GAAP accounting standards, contractual information rights become critical. These rights provide insight into key areas like burn rates, protocol health, and insolvency risks, addressing the need for more transparency in this space.

To tackle these challenges, BeyondOTC offers customized solutions for crypto pre-IPO investments. The platform bridges the transparency gap by providing secure deal rooms that house essential fundraising details, cap table data, and due diligence support. BeyondOTC has already facilitated investments totaling over $5 billion in TVL and has guided more than $2 billion in fundraising advisory services.

What sets BeyondOTC apart is its focus on crypto-specific metrics. The platform provides real-time access to data like TVL opportunities, smart contract risk assessments, and APY optimization insights – key factors for assessing growth potential and liquidity risks. Their automated performance trackers allow continuous monitoring of protocol performance in the fast-moving crypto world. To date, BeyondOTC has contributed over $40 million to DeFi TVL and supports more than 1,000 active deals across 50+ countries.

When negotiating information rights, investors can benefit from BeyondOTC’s fundraising advisory services. These services ensure that crypto-specific clauses – such as TVL reporting and access to smart contract audits – are clearly outlined in term sheets. This strategy enhances the broader negotiation approaches discussed earlier, giving investors the detailed, actionable data they need to make informed decisions in the complex world of crypto pre-IPO investments.

Conclusion

Information rights play a critical role for sophisticated investors navigating the complexities of pre-IPO deals. These provisions turn private investments – often shrouded in uncertainty – into more transparent opportunities by providing access to essential details like financial statements, cap tables, board materials, and performance metrics. Without such rights, investors risk losing visibility into key issues, such as whether a company is burning through cash faster than expected or teetering on the edge of insolvency. This transparency not only supports follow-on investment decisions but also reinforces the strategic advantages outlined earlier.

Negotiating these rights requires careful attention to detail. Investors should aim for Major Investor thresholds – commonly set between $1 million and $2 million – to secure enhanced access. As startup attorney Ryan Roberts succinctly explains:

Information rights are the venture capital compromise between two truths: investors are writing big checks into a company they don’t control, and you’re trying to run a company without a committee.

Whether dealing with traditional tech firms or crypto ventures, the importance of robust information rights remains the same. As noted earlier, these rights are particularly vital in the crypto space, where they help uncover risks unique to digital assets. Platforms like BeyondOTC assist investors in navigating crypto pre-IPO deals by integrating crypto-specific provisions into term sheets.

These rights, which provide oversight and protect capital up until an IPO, automatically expire once the company complies with SEC reporting requirements. Until that point, they remain a cornerstone for making informed decisions, whether you’re evaluating a traditional tech startup or a DeFi protocol. Securing strong information rights isn’t just a smart move – it’s the bedrock of sound pre-IPO investment strategy.

FAQs

What’s the minimum check size to get information rights?

The minimum check size required to secure information rights isn’t set in stone – it depends on the terms negotiated between the company and its investors. Typically, these rights are reserved for those making meaningful financial contributions, such as in venture capital or private equity transactions. In general, larger investments tend to provide investors with more leverage to obtain these rights.

How can I enforce info rights if the company stops reporting?

When a company ceases reporting, your investor rights agreement is your go-to resource. These agreements typically detail the company’s obligations to share financial and operational updates. If the company isn’t meeting these terms, you may have legal options, such as filing a breach of contract claim or seeking specific performance to enforce compliance.

Start by carefully reviewing the agreement to understand your enforcement options. It might include steps like sending formal notices or imposing penalties to address the issue.

Which KPIs should I request for my specific business model?

When evaluating your company’s performance and growth, it’s crucial to zero in on the key performance indicators (KPIs) that align with your goals. Some widely-used metrics include:

- Revenue, gross profit, and EBITDA: These provide a snapshot of your financial health.

- Customer acquisition cost (CAC), lifetime value (LTV), and churn rate: These highlight how effectively you’re engaging and retaining customers.

Your KPIs should align with your business model. For instance:

- SaaS companies often track monthly recurring revenue (MRR), LTV, and churn rate since subscription-based models thrive on customer retention and predictable income.

- E-commerce businesses focus on metrics like conversion rates, average order value (AOV), and repeat purchase rate, as these directly impact sales and customer loyalty.

Tailoring your KPIs ensures you’re measuring what truly drives success for your specific business.