When investing in pre-IPO companies, you have two primary options: forward contracts and direct equity. Each has distinct advantages, risks, and costs, making your choice dependent on your financial goals, risk tolerance, and investment size.

Key Takeaways:

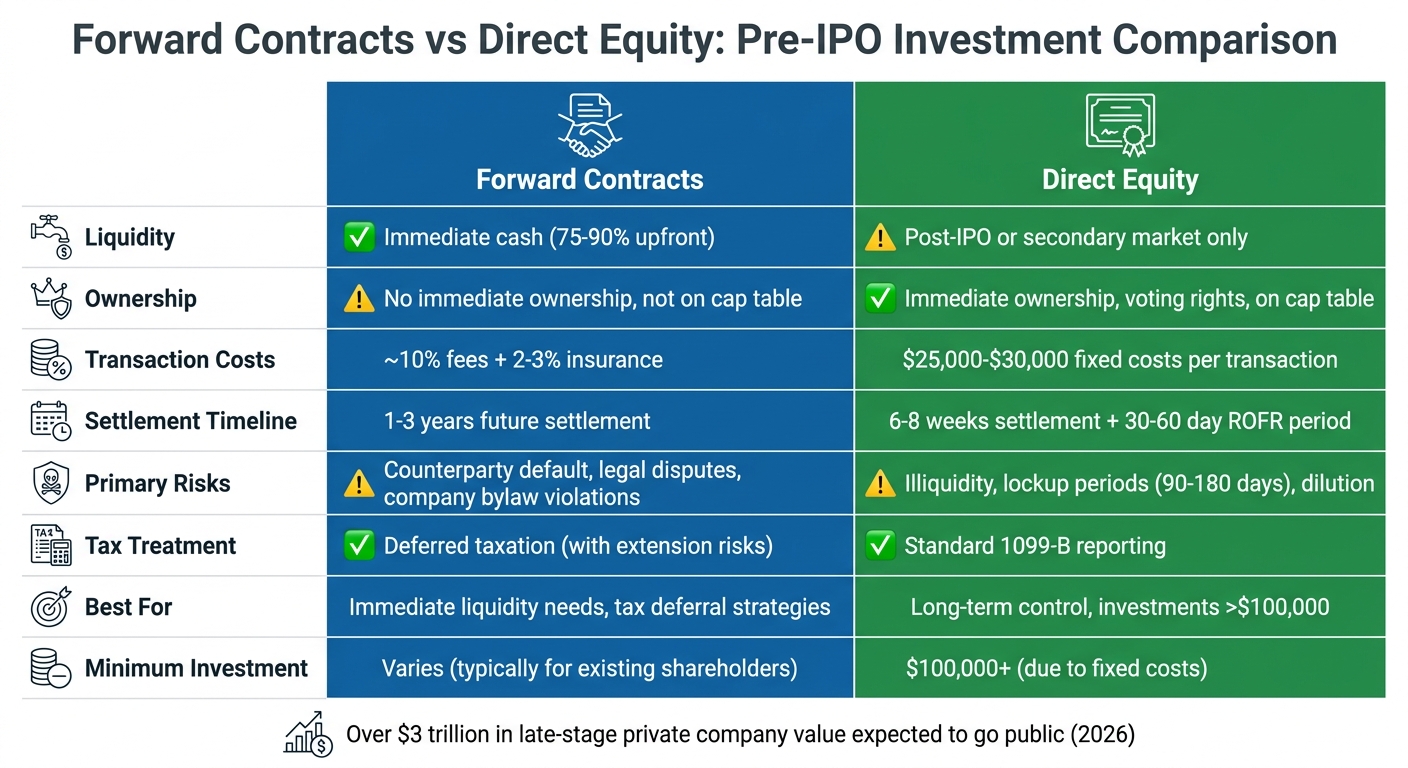

- Direct Equity: You purchase shares directly, gaining ownership, voting rights, and control over your exit after an IPO. Best for large investments (over $100,000) due to high transaction costs ($25,000–$30,000). However, it involves long settlement times (6–8 weeks) and risks like dilution and lockup periods.

- Forward Contracts: These derivative agreements offer liquidity upfront (75–90% of share value) without immediate ownership. They bypass company restrictions like Rights of First Refusal (ROFR) but carry counterparty risk and high fees (10%+).

Quick Overview:

- Liquidity: Forward contracts provide immediate cash but depend on future settlement. Direct equity involves waiting for IPO or secondary market opportunities.

- Ownership: Direct equity gives you voting rights and a spot on the cap table. Forward contracts don’t transfer ownership until settlement.

- Costs: Forward contracts have higher fees, while direct equity suits larger investments due to fixed costs.

- Risks: Forward contracts face counterparty defaults; direct equity risks include illiquidity and valuation uncertainty.

Quick Comparison:

| Feature | Forward Contracts | Direct Equity |

|---|---|---|

| Liquidity | Immediate cash (75–90% upfront) | Post-IPO or secondary market only |

| Ownership | No immediate ownership | Immediate ownership, voting rights |

| Costs | ~10% fees | $25,000–$30,000 per transaction |

| Risks | Counterparty defaults, legal issues | Illiquidity, lockup periods |

| Best For | Immediate liquidity, tax deferrals | Long-term control, large investments |

Both strategies can be combined for diversification. For example, use forward contracts for liquidity and direct equity for high-conviction, long-term investments. With over $3 trillion in late-stage private company value expected to go public, understanding these options is essential for pre-IPO success.

Forward Contracts vs Direct Equity in Pre-IPO Investments Comparison

How Forward Contracts Work in Pre-IPO Transactions

Grasping the mechanics of forward contracts is crucial for understanding their role in pre-IPO strategies.

Forward Contract Structure and Settlement

A Variable Prepaid Forward (VPF) contract is a popular structure in pre-IPO transactions. In this setup, the seller typically receives 75%–90% of the stock’s current value upfront. Settlement happens one to three years later, with the seller delivering a variable number of shares based on the stock price at that time.

This structure uses a collar strategy, which combines a long put option (providing downside protection) with a short call option (limiting upside potential), alongside a secured loan. The exact number of shares delivered depends on the stock’s price movements. If the price drops below a set "floor", the seller must deliver all pledged shares. On the other hand, if the price exceeds a "cap", the seller retains some shares.

"The options hedge provides downside protection, allowing the VPF provider – such as a bank – to issue a larger loan against the concentrated stock pledged as collateral." – Liberman and Sosner, The Journal of Wealth Management

Settlement can occur in two ways:

- Physical settlement: The seller delivers the agreed-upon shares.

- Cash settlement: The seller repays the loan and settles the net value of the options.

For example, a VPF with a floor set at 100% of the stock’s value and a cap at 120% might allow the seller to receive 90% of the stock’s value upfront. A broader range, such as an 80% floor and 140% cap, might yield closer to 78%. This flexibility allows sellers to access immediate liquidity while structuring the deal to align with their financial goals.

Benefits of Using Forward Contracts

Forward contracts offer several advantages, starting with immediate liquidity while deferring taxable events. This deferral can be especially useful if the seller anticipates being in a lower tax bracket in the future.

"A variable prepaid forward contract enables shareholders to obtain cash by selling shares while delaying the payment of capital gains taxes." – Investopedia

Another key benefit is the ability to navigate company-imposed restrictions. Since the legal title of the shares doesn’t transfer at the time of the initial transaction, forward contracts can sidestep barriers like Rights of First Refusal (ROFR) or the need for board approval. However, some companies, such as Anduril Industries, explicitly prohibit forward contracts in their bylaws.

Risks and Drawbacks of Forward Contracts

While forward contracts provide liquidity and flexibility, they come with notable risks.

Counterparty risk is a major concern. If the stock price rises significantly, the seller might breach the contract, leading to potential legal disputes. Buyers often face lengthy litigation, which may result in settling for only a portion of the agreed shares.

High transaction costs are another drawback. Broker fees for these contracts average around 10%, which is double the cost of standard secondary market transactions. Additionally, buyer insurance can add another 2–3% to the overall cost.

Tax implications also pose challenges. For instance, in Estate of McKelvey v. Commissioner, the Second Circuit Court of Appeals ruled that extending Andrew McKelvey’s forward contracts for Monster.com stock in 2008 terminated the original agreements, triggering immediate taxation. This case highlights the risks of extending a VPF. Instead, a more prudent approach may be to "roll" the contract – cash-settling the original agreement and entering into a new one.

Company enforcement can further complicate matters. For example, AirBnB historically banned forward purchase contracts in its bylaws. This created uncertainty for those involved in shadow-market agreements when liquidity events occurred. Violating a company’s bylaws by entering into a forward contract could lead to share clawbacks or legal action.

sbb-itb-7e716c2

How Direct Equity Works in Pre-IPO Deals

Direct equity investments stand apart from forward contracts by offering immediate ownership. When you invest in direct equity, your name is added directly to the company’s cap table, giving you actual ownership and a voice in the company’s decisions.

The Direct Equity Investment Process

To get started, you’ll need to verify your accreditation status. This requires demonstrating an annual income of at least $200,000 ($300,000 for joint filers) or a net worth exceeding $1 million, excluding your primary residence. By early 2026, about 18.5% of U.S. households met these qualifications.

Once accredited, you can explore investment opportunities through platforms like Hiive, Forge, or EquityZen, or work with brokers and angel syndicates. Due diligence is a critical step here. You’ll need to review the company’s cap table, evaluate its financial health, and assess the "409A delta" – the difference between the prices of VC-preferred shares and common shares, which can vary from 20% to 80%.

Next, you’ll navigate the Right of First Refusal (ROFR) process. Most private shares come with a 30–60-day ROFR period, during which the company or existing investors can match your offer. Even if ROFR is waived, the company’s board often has the final say on whether to approve you as a shareholder.

The settlement process typically takes 6–8 weeks. During this time, funds are held in escrow while legal documentation and cap table updates are completed. Keep in mind, this process comes with costs – legal, due diligence, and transfer fees can add up to $25,000–$30,000 per transaction. Because of these expenses, direct equity investments are best suited for amounts exceeding $100,000.

Benefits of Direct Equity Investments

While the process may seem complex, direct equity offers several compelling advantages. For starters, it provides voting rights, allowing you to weigh in on major corporate decisions and access company communications. You also control when to exit your investment after an IPO, without relying on a fund manager. Investors holding at least 25% of shares can even block significant changes, such as amendments to the company’s articles of association.

Another key benefit is the ability to negotiate registration rights. These agreements can require the company to assist in reselling your shares after it goes public. You might secure demand rights (forcing the company to register your shares) or piggyback rights (allowing you to join the company’s registration efforts).

The financial rewards can also be substantial. For example, when Visa went public in 2008, its shares jumped 28% on the first day of trading. Similarly, Palantir‘s shares, which traded between $4.50 and $6.50 on secondary markets, opened at $7.50 during its 2020 IPO and climbed to $25 within six months.

Risks and Challenges of Direct Equity

Despite its advantages, direct equity comes with risks, starting with illiquidity. The average age of companies at IPO has grown to 13 years as of 2025, up from 10 years in 2018. Late-stage private companies preparing for IPOs represent over $3 trillion in market capitalization as of early 2026, but there’s no certainty when – or if – any specific company will go public.

Post-IPO, investors often face lockup periods of 90 to 180 days, during which selling shares is prohibited. This can lead to a tax mismatch, where you owe taxes on paper gains but lack the liquidity to pay them.

Another challenge is valuation opacity. Limited disclosure requirements mean investors often rely on pitch decks or "Tape D" marks to gauge value. High-profile companies like SpaceX (valued at over $350 billion in 2026) and Stripe ($95 billion) tightly control their cap tables, approving or rejecting secondary buyers to manage regulatory concerns.

Finally, the liquidation waterfall can diminish returns. Direct equity investors usually acquire common stock, which ranks below preferred stock in payout priority. Venture capitalists holding preferred shares are paid first, and their liquidation preferences can absorb much of the proceeds. To avoid surprises, it’s essential to model various exit scenarios to understand potential returns for common shareholders.

"Successful investors plan for failure. Understanding why transactions fail and how to assess completion probability is as important as understanding how they succeed." – AltStreet

Before committing capital, research the company’s ROFR history. Some firms actively block secondary transfers to consolidate ownership, which could prevent your deal from closing even after weeks of effort and significant due diligence costs.

Forward Contracts vs. Direct Equity: Side-by-Side Comparison

When deciding between forward contracts and direct equity, it’s essential to weigh factors like liquidity, control, and potential returns. Each option caters to different investment goals, and understanding their nuances can help you make informed decisions and sidestep costly errors.

Liquidity and Exit Strategies

Direct equity gives you the freedom to decide when to sell your shares after an IPO, as long as any lock-up periods have expired. This independence means you’re not relying on a fund manager to make that call for you. However, direct equity transactions come with hurdles: they typically require a 6–8 week settlement period and a 30–60 day Right of First Refusal (ROFR) window. During this time, transfers can be blocked if the company exercises its ROFR, the board rejects the transfer, or the valuation fluctuates before approval. Many deals fall through during this phase.

Forward contracts avoid the ROFR process initially, but they come with their own risks. Ownership only transfers upon delivery, which creates a problem if the stock’s value increases significantly – sellers might refuse to deliver, potentially leading to legal disputes.

For smaller investments handled through Special Purpose Vehicles (SPVs), you’re essentially a passive investor. The SPV manager controls the exit timing, leaving you with little say in the process.

Control and Ownership Rights

Ownership plays a key role in differentiating these two structures. With direct equity, you immediately become part of the company, earning a spot on the cap table. This comes with voting rights and access to company updates, allowing you to participate in major decisions and stay informed about the company’s strategy.

In contrast, forward contracts leave legal ownership with the seller until delivery. This means you don’t gain voting rights, access to company communications, or a direct relationship with the company. Essentially, you’re invisible to the issuer, and complications like the seller’s divorce or death can derail the transaction entirely.

"The best way to know for certain if the secondary transaction you are entertaining is a forward contract is to ask point-blank how the shares were acquired. If the shares were purchased outright… You’ll be put on the cap table — or at least be part of a special-purpose vehicle that’s put on the cap table — which makes the whole transaction transparent to all parties."

- Bill Clark, CEO and Founder, MicroVentures

Some platforms may use terms like "participation interests" or "alternative derivative instruments" to describe forward contracts. Always confirm if your investment will place you on the cap table before committing.

Return Potential and Risk Comparison

Direct equity avoids intermediary fees but requires a larger upfront investment. On the flip side, forward contracts carry counterparty risk – if the seller refuses to deliver, you may face litigation. Direct equity also has higher closing costs, often reaching $25,000–$30,000 for legal counsel, due diligence, and transfer fees. This makes it a better fit for investments over $100,000.

SPVs can lower operational risks by offering professional vetting and reduced minimums, but management fees and carried interest can significantly cut into your net returns.

"Forward contracts fall into that category because they add unnecessary risk to an already inherently risky transaction."

- Bill Clark, CEO and Founder, MicroVentures

To increase your chances of success, research the company’s ROFR history. Companies with established secondary programs are generally less likely to block transactions. These factors can help you determine which option aligns better with your investment goals and risk tolerance.

When to Use Forward Contracts vs. Direct Equity

Deciding between forward contracts and direct equity depends on factors like your investment size, timeline, and goals. Each option has its own strengths and limitations, and knowing when to choose one over the other can save you from unnecessary expenses and complications.

Best Use Cases for Forward Contracts

Forward contracts – particularly Variable Prepaid Forward Contracts – are ideal if you already own shares in a pre-IPO company and need immediate liquidity while deferring taxes. These contracts typically provide an upfront cash payment ranging from 75% to 90% of your shares’ current value.

"Variable Prepaid Forward Contract: Cash Now, Taxes Later" – Longbridge

This structure is especially useful for accessing liquidity without affecting the company’s cap table.

Best Use Cases for Direct Equity

Direct equity works best for larger investments, typically $100,000 or more, where you want more control over your stake. Fixed costs, which range from $25,000 to $30,000, often make direct equity practical only for significant commitments. This option is particularly appealing to family offices or high-net-worth individuals who value voting rights, direct communication with the company, and control over their exit strategy after the IPO.

Another advantage of direct equity is simpler tax reporting, as it uses a standard 1099-B form. This is less complex compared to SPVs, which require K-1 schedules. To minimize risks during the 30–60 day Right of First Refusal (ROFR) period, focus on companies with well-established secondary trading patterns.

Combining Both Approaches for Diversification

You don’t have to pick just one strategy – combining forward contracts, SPVs, and direct equity can help balance risk and reward. Many savvy investors use SPVs to diversify across multiple late-stage companies, such as SpaceX, OpenAI, or Stripe, with minimum investments as low as $10,000 to $25,000. This approach spreads risk across several "hectocorns" (private companies valued at over $100 billion) and helps mitigate potential losses if a single company cancels or delays its IPO.

Meanwhile, direct equity can be reserved for high-conviction investments where you want a direct relationship with the company. This dual strategy allows you to maintain a core long-term position while hedging against market volatility. With over $3 trillion in late-stage private company value expected to go public by early 2026, building a diversified pre-IPO portfolio has never been more critical.

Conclusion and Key Takeaways

Deciding between forward contracts and direct equity in pre-IPO transactions hinges on factors like transparency, risk tolerance, and your broader investment objectives. Direct equity offers ownership with clearer legal rights and, in some cases, voting privileges. In contrast, forward contracts are private agreements that come with considerable counterparty risk – sellers might default if share prices surge, or delivery could be hindered by company bylaws or unexpected events.

The regulatory environment is evolving, and forward contracts are facing increased scrutiny. The SEC has initiated investigations into their use in private equity due to concerns about misrepresentation and the absence of robust safeguards. Bill Clark, CEO and Founder of MicroVentures, explained:

"Forward contracts… add unnecessary risk to an already inherently risky transaction".

Be cautious if a platform uses ambiguous terms like "participation agreements" or "alternative derivative instruments", as these often signal the use of forward contracts rather than direct equity purchases. These regulatory developments highlight the need for thorough due diligence.

Direct equity and SPVs (Special Purpose Vehicles) offer more transparent alternatives for accessing pre-IPO opportunities. Direct equity is typically suited for investments of $100,000 or more, where legal and administrative costs (ranging from $25,000 to $30,000) make sense. SPVs, on the other hand, allow investors to participate with lower minimums – usually between $10,000 and $25,000 – while also helping companies manage their cap tables effectively. With over $3 trillion in late-stage private company value projected to go public by early 2026, understanding these structures is more important than ever.

Whether you lean toward forward contracts, direct equity, or a mix of both, the key to navigating the pre-IPO investing landscape lies in prioritizing transparency and conducting rigorous due diligence.

FAQs

How can I tell if a deal is a forward contract or real shares?

To figure out whether a deal involves a forward contract or real shares, take a close look at the agreement and delivery terms.

- Forward contracts involve paying now to lock in the right to receive shares at a future date. However, there’s no immediate transfer of ownership when the deal is made.

- Real shares, on the other hand, usually mean ownership is transferred right away or on a clearly defined schedule.

By carefully reviewing the contract, you can determine if it represents a derivative (like a forward contract) or a straightforward equity purchase.

What happens if the company bans the structure I used?

If a company prohibits the use of certain structures, like forward contracts or direct equity investments, it could limit your liquidity options. This might delay your ability to exit before an IPO or acquisition. Additionally, if these structures were part of previous agreements, it could lead to legal or contractual complications, forcing you to adjust your strategy to align with the new restrictions.

How do I estimate my payout as a common shareholder?

To figure out your potential payout in a pre-IPO transaction, start by calculating the fair market value of your shares. This involves evaluating the company’s valuation and factoring in common secondary market discounts, which typically range between 25% and 45%. Once you have this adjusted value, multiply it by the number of shares you own.

Keep in mind that several factors can influence your final payout. These include discounts related to marketability and liquidity, as well as possible tax implications – such as whether your earnings will be taxed as capital gains or ordinary income. These considerations can significantly affect your net proceeds.