Tender offers and open market Pre-IPO sales are two ways private company shareholders can sell their shares before an IPO. Both methods provide liquidity but differ in process, pricing, and regulation. Here’s what you need to know:

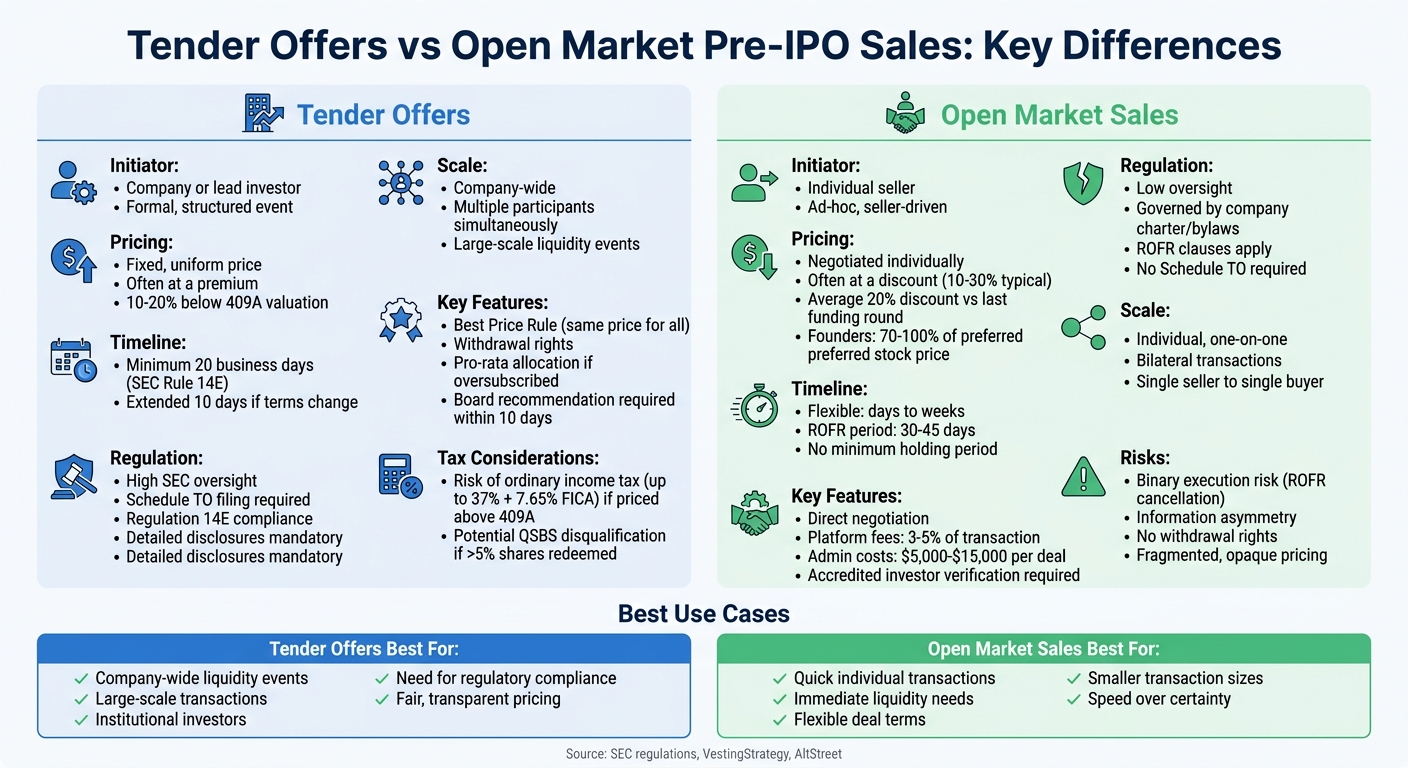

- Tender Offers: Organized by the company, these are structured events where buyers purchase shares from multiple shareholders at a fixed price. They follow strict SEC rules, require a minimum 20-day timeline, and offer consistent pricing for all participants.

- Open Market Sales: These are private, one-on-one transactions between a seller and a buyer, often negotiated through third-party platforms. They are faster but come with fewer regulatory safeguards and often involve discounts.

Quick Comparison

| Feature | Tender Offer | Open Market Sale |

|---|---|---|

| Initiator | Company or lead investor | Individual seller |

| Pricing | Fixed, often at a premium | Negotiated, often at a discount |

| Timeline | Minimum 20 business days | Flexible; days to weeks |

| Regulation | High (SEC oversight, Schedule TO) | Low (company rules, ROFR clauses) |

| Scale | Large, company-wide | Individual, one-on-one |

Tender offers work best for large-scale liquidity events, while open market sales are ideal for quick, individual transactions. Your choice depends on your goals, timeline, and tax considerations.

Tender Offers vs Open Market Pre-IPO Sales Comparison Chart

How Tender Offers Work

The Tender Offer Process

A tender offer typically unfolds in seven steps. It begins with the bidder – either the company itself or an external investor, such as a venture capital firm – proposing to buy a specific number of shares at a set price. This price is usually higher than the current market value, making the offer more appealing to shareholders.

Once the offer is initiated, the company’s Board reviews the terms, and legal counsel prepares the necessary documentation. If the transaction involves more than 5% ownership, filings with the SEC are required.

The offer stays open for at least 20 business days, giving shareholders time to evaluate their options. During this period, shareholders can decide to tender (sell) their shares or withdraw them if they change their minds before the offer closes. If more shares are tendered than the bidder initially planned to buy – referred to as oversubscription – the shares are usually accepted on a pro-rata basis. After the offer period ends, the bidder finalizes the allocation and processes payments within three business days. If the bidder decides to adjust the price or the number of shares they aim to purchase, the offer must be extended by at least 10 business days.

These steps are designed with safeguards to ensure the tender offer process remains fair and transparent.

Main Features of Tender Offers

Tender offers include several features aimed at protecting shareholders. For instance, proration ensures that shareholders sell a proportional amount of their shares when the number of shares tendered exceeds the bidder’s target, maintaining an orderly process. Withdrawal rights allow shareholders to reclaim their tendered shares at any point before the offer concludes, adding flexibility.

The company must disclose its recommendation regarding the offer within 10 business days of its launch. Specific eligibility criteria, such as vesting requirements or a minimum holding period for exercised options, may also be applied. The Best Price Rule guarantees that every shareholder receives the same price for their shares, eliminating the possibility of preferential treatment or side deals. Additionally, under Section 14(e) of the Securities Exchange Act, bidders are prohibited from making any material misstatements or omissions.

Christopher McKinnon from MoFo highlights the importance of these rules:

"The tender offer rules are generally designed to ensure timely, accurate, and adequate disclosures so that shareholders can make an informed decision".

For companies in the crypto space, pricing above the 409A fair market value can have tax implications. The excess may be treated as ordinary income by the IRS, leading to a tax rate of up to 37% plus 7.65% FICA, which eliminates the benefits of capital gains treatment. Additionally, if a company-led redemption exceeds 5% of total shares, it can disqualify Qualified Small Business Stock (QSBS) benefits for all shareholders, even those who don’t participate.

sbb-itb-7e716c2

How Open Market Pre-IPO Sales Work

The Open Market Sales Process

Open market pre-IPO sales take place through direct transactions between sellers and buyers, without the company’s involvement in coordinating the deal. Unlike tender offers, these sales happen informally when a shareholder finds a buyer through private networks or over-the-counter (OTC) platforms.

The process begins when a seller identifies a buyer and negotiates the terms, including the price. Once both parties agree, the seller submits a transfer notice to the company, triggering the Right of First Refusal (ROFR). Many private companies have ROFR clauses, which allow the company or its existing investors 30–45 days to match the offer and purchase the shares instead. This introduces what is often referred to as "risk of cancellation" or binary execution risk. Essentially, the buyer may invest time and money into due diligence and commit funds, only for the company to block the deal by exercising its ROFR.

AltStreet explains this dynamic well:

"Unlike the New York Stock Exchange where price discovery occurs through transparent, regulated order books, the private secondary market operates as a fragmented, opaque network of bilateral negotiations".

If the company approves the transfer, the next step is signing a stock purchase agreement. However, these transactions come with administrative costs, typically ranging from $5,000 to $15,000 per deal, which makes them more practical for larger transactions. Once the company gives the green light, the process generally wraps up within a few days to a few weeks.

Main Features of Open Market Sales

Open market pre-IPO sales stand out due to features that set them apart from tender offers. One of the most notable differences is pricing flexibility. Prices in these deals are individually negotiated and often trade at an average 20% discount compared to the valuation from the last preferred funding round. For founders selling common shares, the payout typically ranges from 70% to 100% of the preferred stock price from the most recent financing round.

Timing is another key distinction. These transactions are entirely seller-driven and ad-hoc, unlike tender offers, which follow a structured timeline of at least 20 business days. Open market sales can happen whenever a shareholder needs liquidity and finds a willing buyer. However, this flexibility comes with challenges, as there’s no centralized order book to publish bid-ask spreads. This can result in substantial price differences for the same type of securities across various transactions.

Regulation is also notably lighter for open market sales. These transactions are governed more by the company’s internal rules – like its charter and bylaws – rather than strict SEC tender offer regulations, as long as they don’t meet the legal definition of a tender offer. Platforms that facilitate these deals typically charge 3% to 5% of the transaction value, and buyers are required to confirm their status as accredited investors before participating.

The growing popularity of these transactions reflects the increasing activity in the secondary market. This flexible and less regulated approach offers a practical option for shareholders seeking fast liquidity, especially in fast-evolving industries like crypto.

How to Sell Pre-IPO Stock Options Before Your Company Goes Public

Comparing Tender Offers and Open Market Sales

In the world of crypto OTC trading and Pre-IPO deals, the operational differences between tender offers and open market sales play a big role in shaping liquidity and ensuring compliance.

Process and Who Initiates

Tender offers are initiated by the company, while open market sales are driven by individual sellers. In a tender offer, the company’s board approves a formal bid to buy shares from multiple shareholders simultaneously. These offers often come with specific eligibility criteria, like requiring employees to have a certain tenure – say, four years or more. On the other hand, open market sales are more straightforward: a shareholder finds a buyer and negotiates directly.

VC Beast sums it up well:

Tender offers are the right tool for company-wide liquidity events at scale. Secondary sales work for individual transactions.

While both methods require company approval, tender offers are proactive, planned events led by leadership. Open market sales, however, start when a shareholder submits a transfer notice, which activates the company’s Right of First Refusal (ROFR).

These differences also impact pricing strategies and the time it takes to complete transactions.

Pricing and Timing

The pricing approach varies significantly between the two methods. Tender offers use a single price for all participants, often set higher than market value to encourage shareholders to sell. This price is typically tied to the latest funding round or the company’s 409A valuation. In contrast, open market sales involve negotiated pricing between the buyer and seller, usually at a 10% to 30% discount due to the risks and illiquidity involved.

There’s also a big difference in timelines. SEC Rule 14e-1 requires tender offers to stay open for at least 20 business days, giving shareholders ample time to decide. Open market sales, however, can wrap up much faster – sometimes within just a few days or weeks. This speed can be a lifeline for shareholders needing quick liquidity, but it often comes with compromises in terms of price and certainty.

Compliance and Oversight

Regulatory requirements mark another major distinction. Tender offers are subject to strict SEC oversight, governed by Regulation 14E and Section 14(e) of the Securities Exchange Act. If the offer involves more than 5% of the company’s shares, a Schedule TO must be filed with the SEC. These rules ensure protections like withdrawal rights for shareholders and enforce the "Best Price Rule", guaranteeing everyone gets the same offer.

Open market sales, in contrast, face much lighter regulation. They’re primarily governed by the company’s internal rules – its charter, bylaws, and agreements between the parties involved. There’s no Schedule TO, no 20-day requirement, and fewer disclosure obligations. However, sellers still need to navigate company-specific hurdles like ROFR clauses and board approvals. While this lighter regulatory touch makes open market sales quicker, it also provides fewer safeguards for investors.

Here’s a quick comparison of the two methods:

| Feature | Tender Offer | Open Market Sale |

|---|---|---|

| Initiator | Company or lead investor | Individual seller |

| Pricing | Single uniform price; often a premium | Negotiated; often a 10–30% discount |

| Timeline | Minimum 20 business days | Flexible; days to weeks |

| SEC Oversight | High (Reg 14E, Schedule TO) | Low (company charter, ROFR) |

| Scale | Company-wide; many participants | Bilateral; typically one-to-one |

| Withdrawal Rights | Mandated by SEC | Generally none once agreed |

Benefits and Risks of Each Method

For crypto investors, the choice between tender offers and open market sales can significantly impact liquidity, tax outcomes, and overall investment returns. Each method comes with its own set of advantages and challenges that investors need to weigh carefully.

Tender Offers: Benefits and Risks

Tender offers follow a structured process where all participants are offered the same price, alongside detailed company disclosures to help them make informed decisions. For companies, this method simplifies cap table management, provides liquidity to multiple shareholders at once, and allows third-party investors to acquire substantial equity stakes without waiting for a new funding round.

But tender offers aren’t without their downsides. For instance, a $1M gain could lead to a tax bill of approximately $447K if the offer price exceeds the 409A valuation, as the excess may be taxed as ordinary income. According to VestingStrategy:

"Company-led tenders priced above 409A valuation can trigger IRS scrutiny. The excess may be treated as compensation across all participants – potentially doubling effective tax rates."

Another risk is the potential loss of Qualified Small Business Stock (QSBS) tax benefits. If more than 5% of a company’s shares are redeemed in the process, all shareholders could lose these benefits. Additionally, oversubscription can lead to proration, meaning participants might not be able to sell or buy the full number of shares they intended.

A real-world example is the Snowflake tender offer from February 2020. Employees sold shares at $38.77 each, only to see the stock skyrocket to $253 on IPO day. This highlights the risk of underpricing in tender offers.

Open Market Sales: Benefits and Risks

Open market sales, on the other hand, are completed quickly – often within days or weeks – and allow for deal terms to be customized, making them a good choice for investors seeking fast liquidity.

However, these transactions come with their own challenges. Unlike tender offers, they typically lack detailed disclosure documents, which can lead to uneven access to information. To offset this risk and account for the illiquid nature of the shares, buyers often demand a discount of 10% to 30%. Furthermore, company-specific restrictions like Right of First Refusal (ROFR) clauses can block or delay these transactions, adding another layer of complexity.

Here’s a quick comparison of the two methods:

| Feature | Tender Offer | Open Market Sale |

|---|---|---|

| Key Benefits | Uniform pricing; detailed disclosures; regulatory oversight | Speed; flexibility; customizable terms |

| Key Risks | Tax recharacterization; potential QSBS disqualification; proration | Information gaps; required discount; ROFR delays |

| Best For | Achieving company-wide liquidity at scale | Individual transactions requiring fast execution |

Choosing the right approach requires a clear understanding of these trade-offs, especially in the fast-moving world of crypto investments. Each method serves different needs, and the decision will depend on your specific goals and circumstances.

Using These Methods in Cryptocurrency OTC Trading

The principles behind tender offers and open market sales apply seamlessly to the cryptocurrency world, where pre-IPO token sales and OTC (over-the-counter) transactions operate under similar frameworks. With blockchain companies staying private for longer periods, these strategies have become crucial for early investors, employees, and institutional players who want to enter or exit positions before a public listing. Just like in traditional equity markets, these methods help ensure liquidity and compliance with regulations in pre-IPO crypto transactions. Below is a closer look at how each approach is tailored to fit the crypto landscape.

Using Tender Offer Structures for Crypto

In cryptocurrency, a tender offer is a structured event where a buyer – often a venture capital firm or the project itself – offers to purchase tokens or shares from multiple holders at a fixed price. This method provides a way to achieve liquidity on a larger scale while maintaining compliance with regulations and ensuring fair pricing.

To align with regulatory requirements, these transactions must follow SEC Rule 14E. This rule stipulates that the offer must remain open for at least 20 business days, giving participants enough time to review disclosures and consult advisors.

For company-led transactions, pricing plays a critical role. Transactions must be priced at or below the 409A fair market value to avoid issues with the IRS. If the price exceeds this threshold, the IRS may reclassify the excess amount as compensation, which could lead to tax complications. As VestingStrategy explains:

"Company-led tenders should price at or below 409A FMV to secure capital gains treatment. Exceeding it by even a small margin can trigger compensation recharacterization for all participants."

BeyondOTC plays a key role in these liquidity events, handling the necessary documentation, ensuring compliance, and connecting crypto projects with institutional buyers.

Using Open Market Sales for Crypto Pre-IPO Deals

Open market sales in the crypto world involve direct transactions between individual buyers and sellers. This approach offers more flexibility and faster execution compared to tender offers, with deals often closing within days or weeks.

However, sellers need to navigate potential restrictions before proceeding. For instance, Right of First Refusal (ROFR) clauses in token purchase agreements can delay or even block sales. These clauses require sellers to first offer their tokens to the company or existing investors before selling to external parties. Reviewing the terms of these agreements is essential before initiating a sale.

To address these challenges, BeyondOTC connects buyers and sellers in the crypto market, ensuring KYC/AML compliance and facilitating direct negotiations. While open market sales may lack the detailed disclosures of tender offers, BeyondOTC helps bridge information gaps, enabling parties to negotiate terms that reflect the illiquid nature of pre-IPO crypto assets.

Choosing the Right Approach for Pre-IPO Crypto Investments

Summary of Key Differences

When it comes to pre-IPO crypto investments, tender offers and open market sales each bring distinct advantages and challenges. Tender offers are structured events initiated by the company, featuring a single price for all participants, set timelines, and formal disclosures. These offers are built for large-scale liquidity and must remain open for at least 20 business days, as required by SEC Rule 14E. On the other hand, open market sales are privately negotiated transactions between individual parties. They’re faster and more flexible, often wrapping up in days or weeks, but they come with higher execution risks due to Right of First Refusal (ROFR) provisions.

Pricing is another area where these methods diverge. Tender offers usually set a fixed price, often 10% to 20% below the latest 409A valuation for common shares. In contrast, open market sales involve negotiations, leading to varied pricing. For crypto, the discounts in over-the-counter (OTC) markets can be steep – up to 70% for tokens outside the top 100.

Understanding these differences is crucial in aligning your strategy with your investment goals. Whether you opt for the structured nature of a tender offer or the flexibility of an open market sale, these details will guide your decision-making process.

How to Select the Right Method

Choosing between these methods depends on factors like transaction size, speed, and regulatory considerations. If your goal is to buy or sell a significant block of tokens with company cooperation, tender offers provide the structured framework necessary for institutional-level transactions. High-profile companies like SpaceX, Stripe, Databricks, and OpenAI have used tender offers to facilitate billions in liquidity between 2024 and 2025. For instance, SpaceX conducted a $1.25 billion tender offer in 2024.

For smaller, quicker deals, open market sales are often the better choice. However, it’s essential to review the company’s history with secondary trade approvals to avoid complications with ROFR restrictions. Companies nearing an IPO are generally more open to waiving ROFR. Additionally, if you’re considering a company-led tender, check the current 409A valuation. Paying above this valuation could lead to ordinary income tax rates – potentially up to 37% plus FICA – rather than the more favorable capital gains treatment.

BeyondOTC simplifies these processes by managing compliance, connecting buyers and sellers, and ensuring all documentation is in order. Whether you lean toward the structured approach of a tender offer or the agility of an open market sale, BeyondOTC provides the tools and guidance to align your decisions with your timeline and regulatory needs.

FAQs

How do I know if a deal is legally a tender offer?

A tender offer refers to a formal, company-organized process where a buyer proposes to purchase shares from existing shareholders at a predetermined price. This process is defined by specific terms, deadlines, and eligibility requirements, often subject to regulatory scrutiny. Essential aspects include clearly outlined offer conditions and strict compliance with legal obligations.

What taxes can change if the price is above the 409A value?

If the price goes beyond the 409A valuation, any proceeds exceeding the 409A fair market value (FMV) might be classified as ordinary income. This could result in taxes as high as 37%, plus FICA. In contrast, amounts below the 409A FMV are generally eligible for capital gains treatment, which often comes with lower tax rates.

How can ROFR stop an open market pre-IPO sale?

The Right of First Refusal (ROFR) can restrict an open market pre-IPO sale by requiring shareholders to first offer their shares to the company or existing shareholders under identical terms. This gives the ROFR holder the opportunity to either match the offer or decline it, potentially blocking or delaying sales to third parties. By doing so, it helps preserve control over ownership and can impact the timing or conditions of pre-IPO liquidity events.