Side pockets in pre-IPO funds are specialized accounts used to manage illiquid or hard-to-value assets, like private equity or growth-stage investments. These accounts separate such assets from the fund’s main portfolio, ensuring accurate valuation and preventing forced sales during redemptions. While side pockets help preserve the value of these investments, they also lock up investor capital until a liquidity event (e.g., IPO or acquisition) occurs, which can take years.

Key points for Limited Partners (LPs):

- Locked Capital: Funds placed in side pockets are inaccessible until the asset is sold or liquidated.

- Fair Allocation: Only investors at the time of the asset’s side-pocketing share its risks and returns.

- Fee Risks: Some funds charge fees on side-pocketed assets, even if they remain illiquid.

- Secondary Market Options: Platforms like BeyondOTC allow LPs to sell side-pocketed positions but often at a discount.

Before investing, it’s critical to review fund agreements for side pocket terms, fee structures, and valuation processes to avoid surprises. Side pockets are neither inherently good nor bad – they’re tools that require careful consideration to align with your liquidity needs and investment goals.

What Are Side Pockets and How Do They Work?

Definition and Purpose of Side Pockets

A side pocket is a segregated account within a fund, specifically designed to handle assets like private equity positions, venture capital commitments, and growth equity stakes that are illiquid, hard to value, or come with particular risks. By moving an asset into a side pocket, fund managers separate it from the main fund’s regular NAV (Net Asset Value) calculation. This approach helps avoid mispricing and protects both incoming and outgoing investors from being unfairly impacted by the valuation challenges of these assets.

Side pockets also address a timing issue. While many funds allow quarterly redemptions, assets like pre-IPO investments often take years to mature. By isolating these holdings, managers can hold onto them until a liquidity event – such as an IPO or acquisition – occurs, rather than being forced to sell at a loss to meet redemption requests.

"Side pockets offer a targeted method of isolating specific assets without impeding liquidity across the wider portfolio." – Maples Group

How Side Pockets Operate in Pre-IPO Funds

When a General Partner (GP) decides to place an asset into a side pocket, current investors receive a pro-rata share in the separate account based on their ownership percentage at the time. Their capital account in the main fund is adjusted accordingly. New investors who join the fund after the side pocket is created do not have any exposure to those specific assets – they are only linked to the liquid portion of the fund.

Once an asset is moved into a side pocket, investors are tied to it until the asset is either liquidated or reaches a stable valuation. This process can take several years. Even if an investor redeems their stake in the liquid portion of the fund, they remain locked into the side pocket until the GP resolves the asset through a sale, IPO, or write-off.

In 2025, 81% of funds with side pocket provisions required mandatory participation, while only 24% of funds with this authority placed limits on the percentage of assets that could be side-pocketed. This highlights fund managers’ preference for having flexibility in managing these accounts. Because of this discretion, it’s essential for Limited Partners (LPs) to carefully examine side pocket terms in fund agreements before committing their capital.

This structure has a direct impact on LP liquidity, which will be discussed in the next section.

sbb-itb-7e716c2

How Side Pockets Affect LP Liquidity

Locked Capital and Delayed Distributions

Side pockets, by design, can significantly impact Limited Partner (LP) liquidity by locking capital and altering the timing of distributions.

When a General Partner (GP) assigns an asset to a side pocket, your capital tied to that asset becomes inaccessible until it is either liquidated or reassigned. This process can drag on for years. Even after redeeming your liquid stake in the fund, your interest in the side pocket remains locked until the underlying asset is resolved.

This situation creates what’s known as a "residual side pocket interest." Paul Daniels from Stone Coast Fund Services explains this challenge clearly:

"Investors may retain a residual side pocket interest long after ‘exiting’ the fund, a fact that may be poorly understood until it is unfolding in reality".

Distributions from side pockets are not scheduled regularly. Instead, they depend entirely on liquidity events tied to the segregated assets. For example, if a pre-IPO company delays its public offering or sells at a lower valuation than anticipated, the timeline for distributions may stretch further. Meanwhile, management fees can chip away at your ownership interest. If you’ve already redeemed your liquid balance, the fund might log your share of ongoing expenses as payables, which would be due when the illiquid asset is eventually realized.

While this delay limits immediate access to funds, it serves a broader purpose in preserving the value of the underlying asset.

Protecting Asset Value During Illiquidity

One of the key benefits of side pockets is their ability to protect the value of illiquid assets. By isolating these assets, fund managers avoid being forced into selling them at distressed prices just to meet redemption requests. This approach helps maintain the asset’s value and ensures fairness for all LPs.

Without side pockets, the dynamics could shift unfairly. Early redeemers might withdraw more than their fair share of the liquid assets, leaving remaining investors with an outsized portion of illiquid holdings. As Paul Daniels points out:

"Without side‑pocketing investments, redeeming investors could receive more than their fair share, or remaining investors could be left holding a disproportionate amount of illiquid risk".

Side pockets, therefore, act as a safeguard, balancing the interests of all investors while protecting the value of illiquid assets during uncertain periods.

What Are Side Pockets In Hedge Funds?

Risks and Benefits of Side Pockets for LPs

Side Pockets in Pre-IPO Funds: Benefits vs Risks for Limited Partners

Benefits of Side Pockets for LPs

Side pockets, while addressing liquidity challenges, offer several advantages for limited partners (LPs).

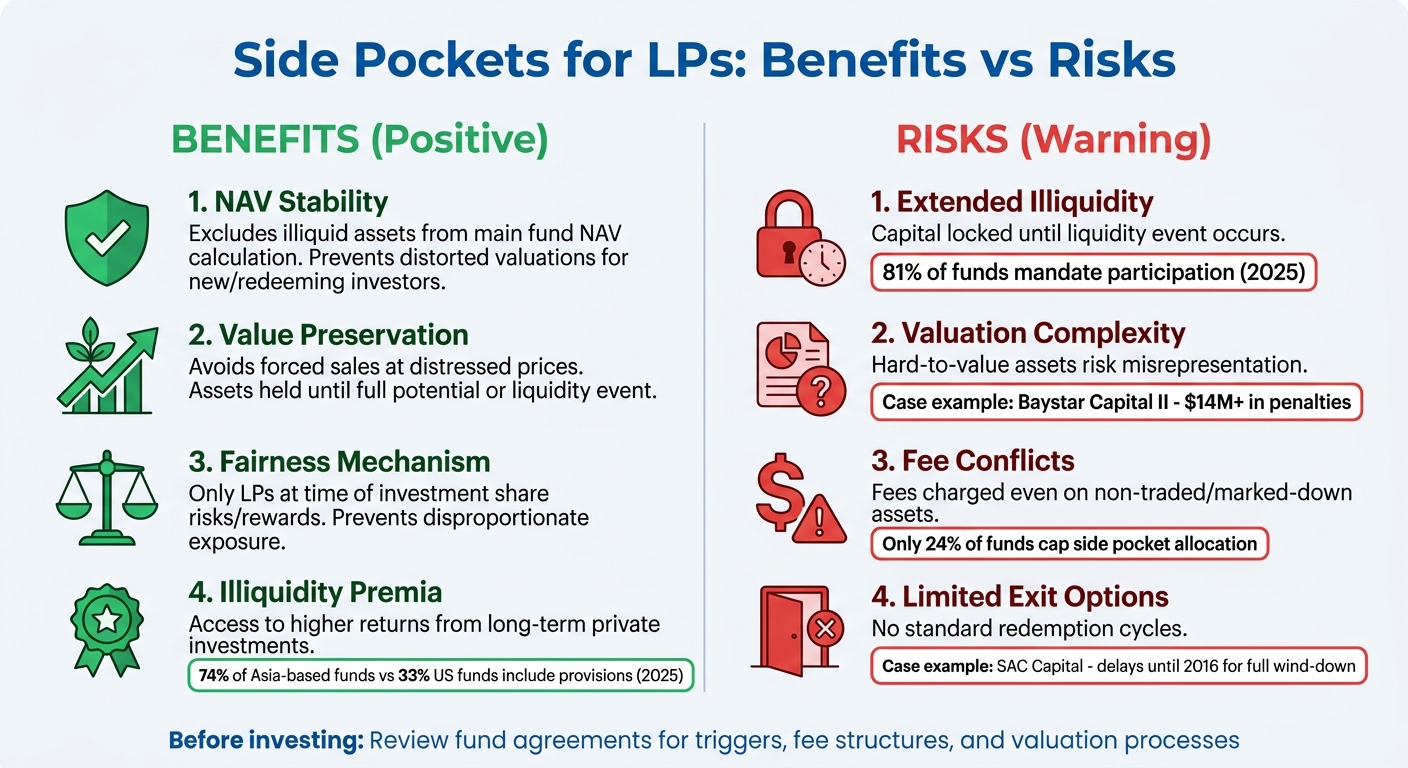

One major benefit is NAV Stability. By excluding illiquid or hard-to-value assets from the main fund’s net asset value (NAV) calculation, side pockets help maintain a more accurate valuation. This ensures that new or redeeming investors aren’t unfairly impacted by distorted NAV figures.

Another advantage is Value Preservation. Segregating illiquid pre-IPO holdings allows fund managers to avoid selling these assets at distressed prices to meet redemption demands. Instead, these assets can be held until they achieve their full potential or a liquidity event occurs.

The Fairness Mechanism is also critical. Side pockets ensure that only the LPs involved at the time of the investment share in its risks and rewards. This approach prevents new investors from inheriting the burden of older, illiquid assets and protects remaining LPs from being disproportionately exposed.

Additionally, side pockets offer access to Illiquidity Premia, creating opportunities for higher returns from long-term private market investments. By isolating these assets, funds can target high-growth pre-IPO companies without the need for large cash reserves, which could otherwise weigh down overall performance. Notably, in 2025, approximately 74% of Asia-based open-ended fund launches included side pocket provisions from the start, compared to just 33% in the US.

Despite these benefits, LPs must carefully evaluate the risks associated with side pockets.

Risks of Side Pockets for LPs

While offering advantages, side pockets come with notable risks that LPs should not overlook.

One primary risk is Extended Illiquidity. Once capital is allocated to side-pocketed assets, it remains locked until a liquidity event occurs. In 2025, 81% of funds mandated participation in side pockets, further limiting investors’ ability to access their capital, even after redeeming their main fund stakes.

Valuation Complexity is another concern. Side-pocketed assets are often challenging to value accurately, increasing the risk of misrepresentation. There’s also the potential for inflated valuations, which could artificially support fee levels. Former SEC official Robert Kaplan emphasized this risk:

"Side pockets are not supposed to be a dumping ground for hedge fund managers to conceal overvalued assets".

The Baystar Capital II Case from 2011 highlights this issue. Fund manager Lawrence Goldfarb concealed over $12 million in proceeds from a side-pocketed investment, ultimately paying over $14 million in penalties to settle SEC charges.

Fee Conflicts also pose a challenge. Some managers charge fees on side-pocketed assets, even when these assets are non-traded or marked down. Adrian Whelan, Global Head of Regulatory Intelligence at BBH, explained the danger:

"One of the biggest risks inherent in side-pockets is the ‘moral hazard’ of using them inappropriately or where not really needed".

Alarmingly, only 24% of funds impose caps on the percentage allocated to side pockets.

Finally, Limited Exit Options make side-pocketed assets particularly restrictive. Unlike the main portfolio, these assets don’t adhere to standard redemption cycles, leaving investors waiting for liquidity events that can take years. For instance, SAC Capital Advisors faced significant delays, requiring until 2016 to fully wind down due to challenges in valuing and liquidating side-pocketed assets.

How to Evaluate Side Pockets in Your Portfolio

What LPs Should Consider

Before committing to a fund with side pocket provisions, it’s crucial to carefully review the fund documents and understand the key aspects.

Start by examining the designation triggers. The fund agreement should clearly define when an asset can be moved into a side pocket. Avoid contracts that leave this decision entirely up to the fund manager’s discretion. Look for specific criteria that outline what qualifies as an illiquid or hard-to-value asset.

Pay close attention to the fee structures. Determine whether management fees apply to side-pocketed assets. Ideally, fees should be paused, or performance fees should only be charged when the asset is sold. As Robert Kaplan, Co-Chief of the SEC’s Enforcement Division’s Asset Management Unit, pointed out:

"Hedge fund managers need to honor their obligations to investors, and investors should pay close attention to the discretion that managers wield over side pocketed investments."

Next, evaluate the GP’s track record and strategy. Are side pockets used as a planned, strategic tool or as a reaction to market conditions? For instance, in 2025, 74% of Asia-based open-ended fund launches included side pocket provisions from the start, compared to just 33% in the U.S., suggesting a more deliberate approach in Asia.

Independent valuations are another must. Ensure that the fund employs third-party valuation standards, such as ASC 820 or IFRS. This is critical to avoid inflated valuations, which can lead to excessive fees or delays in redemptions. A notable example is the SEC’s 2010 case against Paul T. Mannion, Jr. and Andrew S. Reckles of the Palisades Master Fund, LP, where they were charged for overvaluing side-pocketed investments.

Finally, understand the participation rules. Participation in side pockets is typically mandatory. Once your capital is allocated to a side pocket, it remains locked until a liquidity event occurs, even if you’ve redeemed your main fund stake.

Using OTC Secondary Markets for Liquidity

Once you’ve assessed the fund’s side pocket provisions, consider alternative ways to access liquidity. Side-pocketed assets often remain illiquid for extended periods, but secondary markets can offer a solution.

Platforms like BeyondOTC specialize in connecting LPs with buyers interested in illiquid holdings, including side-pocketed assets. These over-the-counter (OTC) marketplaces allow transactions at negotiated prices. In 2024, the secondary market hit a record $162 billion in deals, with LP-led transactions making up $87 billion of that total.

However, pricing in secondary markets often involves trade-offs. High-demand funds may trade close to their net asset value (NAV), but less-liquid or underperforming strategies can see discounts of 20% or more below NAV. Early in 2025, some hedge fund positions traded at discounts of 15–20% due to portfolio rebalancing pressures.

Secondary markets also provide opportunities to diversify. Ben Pace, Partner & Chief Economist at Cerity Partners, highlighted this point:

"Participants in the pre-IPO space are strongly encouraged to diversify appropriately across single opportunities and within industry and sector exposures."

Nasdaq Private Market‘s activity in 2025 is a good example of this growing trend. The platform completed approximately $15 billion in tender offers, offering liquidity to employee shareholders and investors ahead of IPOs. This reflects the expanding infrastructure for unlocking liquidity in otherwise locked-up assets.

Conclusion

Side pockets have become a practical tool for managing pre-IPO and other illiquid assets within investment funds. By separating these hard-to-value holdings from the main portfolio, they ensure more accurate net asset value (NAV) calculations and shield remaining investors from the risks of forced sales at unfavorable prices.

In 2025, data showed that Asia-based funds were more likely to use side pockets than their U.S. counterparts, often with mandatory investor participation and minimal asset limits. This regional trend highlights the strategic role side pockets play in managing illiquid assets, emphasizing the need for thorough due diligence.

This approach ties into broader considerations like liquidity timelines and secondary market exit strategies. When assessing funds with side pocket provisions, focus on key factors: clear triggers for their use, fee structures that protect investor value, and reliable, independent valuation processes. While secondary markets can offer exit opportunities for side-pocketed assets, these positions often trade at a discount to their NAV. Incorporating these elements into your overall liquidity plan is essential for balancing short-term and long-term capital access.

Side pockets are neither inherently good nor bad – they’re tools that demand careful evaluation. Scrutinize fund documents, understand the governance framework, and prepare for the possibility that some of your investment might be tied up longer than expected. With the global hedge fund industry managing over $5 trillion in assets, side pockets will remain a key mechanism for balancing liquid fund structures with the challenges of holding illiquid pre-IPO investments.

FAQs

How can I tell if a fund’s side pocket rules are too broad?

Fund managers might have too much leeway if a fund’s side pocket rules are overly broad. This could lead to problems like unfair asset valuation or limitations on redemptions. Pay attention to whether the rules lack clear and specific criteria for how assets are designated and valued. Without this clarity, there’s a risk of misuse and reduced transparency. Well-defined rules are crucial to prevent these issues.

What fees can I still owe after I redeem the liquid part of a fund?

Even after withdrawing the liquid portion of a fund, you might still be responsible for paying fees related to managing the fund’s illiquid assets or side pockets. These fees could include valuation fees, administrative fees, or performance fees, depending on the specific fee structure of the fund and how the side-pocketed assets are managed.

When does it make sense to sell a side-pocket interest on BeyondOTC?

Selling a side-pocket interest can be a smart move when assets that were once difficult to value or sell become easier to cash out. It’s particularly useful if you’re looking for liquidity and don’t want to wait for the fund to handle the asset liquidation. This approach gives you more flexibility to manage your cash flow while staying aligned with your broader investment objectives.